Authored by Jeffrey Tucker via The Epoch Times,

Mortgage rates on a 30-year loan just hit 7 percent, intensifying problems on the demand side. Mortgages plus insurance—which turns a half-million dollar house into a $1.2 million house plus property taxes—became unaffordable for another class of buyers while already out of reach for most people.

On the supply side, millions of existing homeowners are locked into COVID-era mortgages of 3 percent or lower, which makes them negative in real terms. That’s a great deal unless you sell and then have to buy again. It would make no sense to sell in any case, but you are still stuck paying ever higher property taxes on ever higher valuations.

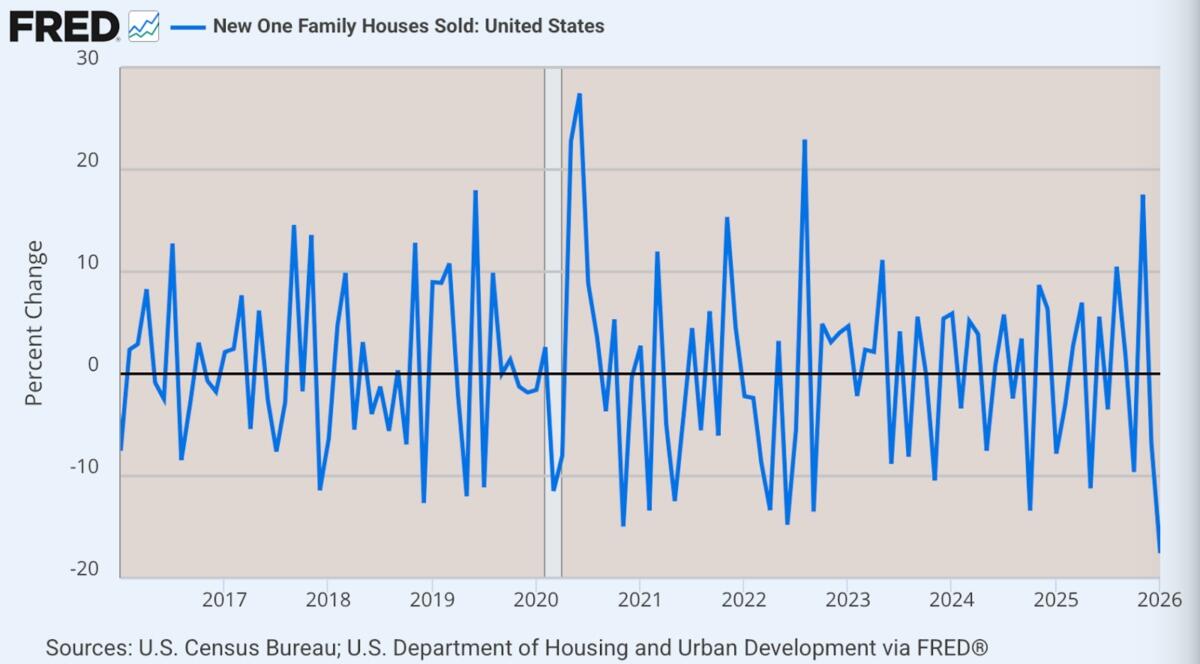

This has produced a problem that is evident in January’s new home sales numbers, which fell 18 percent, the largest drop in 13 years and a level comparable to the bust following the 2008 financial crisis that began with housing. What’s happening in real time is suggested by the anecdotes. People are neither selling nor buying—unless of course you have a full load of cash on hand.

The picture this creates is one of illusory wealth, on one hand, and frustrated renters on the other. The existing owners are paying ever higher property taxes on rising home valuations but their own joy comes from looking at their paper wealth rise on Zillow. It’s an unrealized gain, and realizing it is contingent on willing and lucrative buyers.

Otherwise, they are stuck. Closing a sale at the market price is wonderful but parlaying that into new living conditions would certainly land you in a smaller home or a different market entirely, requiring a geographic relocation. A fixer upper is not really viable either when it seems nearly impossible to find affordable and competent service providers these days plus the high cost of all resources.

This is again more collateral damage from lockdowns and zero interest rates. The people who used stimulus payments for home purchases thought they were getting a great deal. In some ways they were, but this is mitigated by rising property taxes and the feeling of being stuck in a homeowner situation from which there is no financially rational escape.

The buying peak of 2020 is matched by the selling trough of 2026 almost as mirror images.

The housing market is distinct for being spottily illiquid. This doesn’t happen in the market for eggs, jeans, or beef. A frozen market is about plentiful supply but few willing sellers or buyers. Posted prices become illusory because they are not manifested in actual trade. They are only estimates of trades, like a high-priced product on eBay that no one buys.

People are worried about a repeat of 2008 with a housing crash. That’s not out of the question, but the circumstances are different. If real buyers are scarce, and sellers are locked into their favorable contracts, the downward pressure on prices is thereby reduced. Rents are falling today but home prices, not so much. A locked market is different from a crashing one.

It’s hard to see the way out of this one absent a huge increase in supply and a drop in mortgage rates, neither of which seems likely any time soon. Indeed, Trump has reversed his campaign pledge of more housing stocks on grounds that he doesn’t want to reduce property values for existing homeowners, most of whom are the Boomer generation.

This topic is particularly sensitive in American culture. This is because the United States was the first country really to achieve the ideal of widespread and affordable homeownership for the middle class. This began after World War II with thanks in part to tax deductions for mortgage interest and other forms of subsidies. The goal was to construct the American dream. It worked.

The last five years have offered a fundamental challenge to that ideal, as young people are in no position to afford a house. The median age of first-time home buyers from 1950 to the 1990s was 24–28 years old. After 2008, that began to creep up. Today, the age of new home buyers is 40 years and older. Those numbers represent the shattering of an important part of the American dream.

The hope of the Trump administration was to find ways to revive the old dream through lower mortgage rates and other financial benefits to first-time buyers. But in fact, the problem is too entrenched and too deep to be fixed with small policy changes. Plus, since the war on Iran, bond markets have been profoundly disturbed. The yield curve is steepening in ways that have rattled market observers.

That is a conspicuous gap between a promised policy and actual results. It further illustrates just how little control government has over a price spread that is ruled by market forces rather than agency officials or elected leaders. Nor would buyer subsidies work: those are quickly factored into market demand and reflected in higher prices.

Average down payments have shifted upwards too. While the percentage down payment has often been lower today than it was in the 1960s, the real dollar amount has increased as much as four times. This is because homes are much more expensive in inflation-adjusted terms. Saving for a down payment now takes significantly longer relative to income for many households than it did in 1960.

Young people, even those fortunate enough to find high-paying jobs, are priced out of the market for as long as 15 years of their working lives. If they are fortunate to have access to family money, a cash purchase remains the best option by far, even with the deduction for rising interest rates.

This is a significant feature of the demoralization and anger that voters under the age of 35 feel today, along with growing job insecurity, rising medical insurance costs (sometimes even higher than rents), and persistent and rising inflation. I would strongly recommend that all talk of a Golden Age be put on hold until these serious problems begin to resolve themselves. That won’t be anytime soon.

{kind=link}

{kind=link}