Futures are weaker heading into the weekend after US equities finished lower yesterday despite Netanyahu headlines leading to a late day bounceback into EOD. Geopolitical headlines remain the focus overnight with Brent rising as much as 90bps before reversing, as Iran pressed ahead with hitting energy assets & headlines that the US is considering plans to occupy Iran’s Kharg Island to press for the reopening of the Strait of Hormuz. As of 8:15am, S&P 500 futures fell 0.4% after finishing on Thursday under its 200-day moving average which could trigger even more forced selling; Nasdaq 100 futures declined 0.6%. US stocks are on course for a fourth week of losses, the longest losing streak in a year. Brent crude oil prices reversed earlier gains to decline 0.7% to around $108. The VIX rose to around 25. Elsewhere, it was a relatively quiet overnight with upward pressure on yields still the focus (USGG10YR +4bps @ 4.29%) amid concerns about hawkish central bank reaction functions. Metals are mostly lower: Aluminum -4.4%, Silver -1.0%. The US Dollar is up 0.2% as markets price in less than 5bp of Fed rate cuts this year, down from 60bp last month. There is no macro on today's calendar.

In premarket trading, Mag 7 stocks are all lower (Alphabet -0.7%, Amazon -0.6%, Tesla -0.4%, Nvidia -0.5%, Meta -0.4%, Microsoft -0.5%, Apple -0.4%)

- FedEx (FDX) climbs 7% after raising its full-year profit forecast, signaling that the courier’s plan to restructure its delivery network is gaining traction despite geopolitical conflict and economic volatility.

- Figs Inc. (FIGS) rises 6% after Oppenheimer upgraded the seller of medical scrubs to outperform, saying a sustained recovery is underway.

- Firefly Aerospace (FLY) gains 7% after the spacecraft maker reported revenue for the fourth quarter that beat the average analyst estimate

- Planet Labs (PL) gains 14% after the satellite imaging firm reported revenue for the fourth quarter that beat the average analyst estimate.

- Rhythm Pharmaceuticals (RYTM) rises 6% after the drugmaker said it received expanded indication approval from the FDA for its drug Imcivree (setmelanotide) to treat patients four years and older with acquired hypothalamic obesity.

- Super Micro Computer Inc. (SMCI) tumbles 26% after the US charged a co-founder with illegally diverting billions of dollars in Nvidia Corp.-powered servers to China.

- York Space Systems (YSS) rises 9% after the space and defense company gave revenue guidance in its first report as a public company that JPMorgan called “solid.” The firm also saw revenue grow and its losses narrow in the fourth quarter.

In other corporate news, at least a dozen large drugmakers are set to roll out copies of Novo Nordisk’s blockbuster weight-loss drugs in India, crashing prices as soon as the patent expires Friday. JPMorgan started a monitoring program to guard against overwork by its junior investment bankers, according to the Financial Times. Alibaba and Tencent lost $66 billion of market value in 24 hours after failing to lay out clear visions for how to profit off AI. Meanwhile, investors overwhelmed by Iran news are turning to AI tools - mining history for insights and context to assist work-flows and time management.

“Investors are stuck in geopolitical pinball right now,” said Max Gokhman, deputy CIO at Franklin Templeton Investment Solutions, as “literally and figuratively explosive developments are bouncing global market sentiment.” Confidence is being tested, and different schools of thought on the length of conflict are emerging.

An ugly, rollercoaster week is set to end with the Iran war - about to enter its third week - showing no signs of easing as Tehran keeps up attacks on Arab states in the Persian Gulf even after Israel signaled it would spare the country’s energy infrastructure. Axios reported the US is considering plans to take over Iran’s key oil-export site Kharg Island to add pressure on Tehran to reopen the Strait of Hormuz. Iran’s Revolutionary Guard insists it’s still building missiles and vowed the war will continue. Oil is headed for another weekly surge.

“I think that the market is right now coming to grips with the reality that higher energy prices are going to persist longer than expected,” said Mark Malek, chief investment officer at Siebert Financial. “It is clear that the Iran regime turned to the last page in its playbook: MAD, mutually assured destruction.”

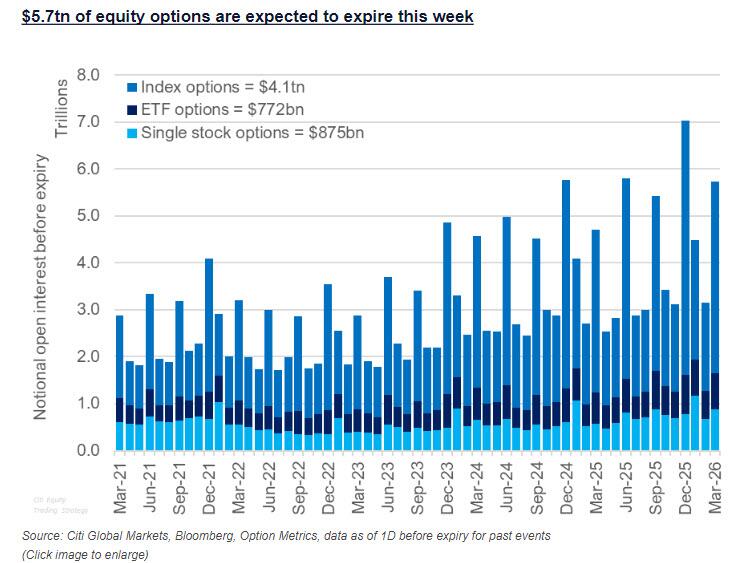

Meanwhile, traders braced for a historic amount of March options expiry. Roughly $5.7 trillion in notional options tied to individual US stocks, indexes and exchange-traded funds are set to expire on Friday in the quarterly event that traders have dubbed the “triple-witching”, the largest March expiry in 30 years and one the 4th largest ever. That includes $4.1 trillion in index contracts, $772 billion in exchange-traded funds and $875 billion in single-stock options. The event has a reputation for triggering abrupt price swings as large pools of derivatives exposure suddenly vanish. It also tends to reset dealer gamma sharply lower, unleashing an "unclenching" that lead to higher volatility in subsequent days. The scale of this week’s expiration is also notable relative to the broader market. At 8.4% of Russell 3000 Index market capitalization, it’s well above historical norms, amplifying the potential for positioning-driven flows.

Trading activity in options markets has surged in recent weeks, particularly in index and ETF contracts, both of which hit record notional volumes in March, about 9% above their year-to-date averages, according to Citi's Vishal Vivek. In contrast, single-stock options volumes are roughly 3% below the level, a move partly attributed to waning retail participation and worries around geopolitical risks.

Stocks including Regeneron Pharmaceuticals Inc., PDD Holdings Inc. and T. Rowe Price Group Inc. are among those seen as vulnerable to outsized moves during the session as they have large open interest in options that expire near the current prices, according to Citi.

“Given recent volatility, today could almost be described as unchanged but clearly the bias has been lower,” said Sameer Samana, head of global equities and real assets at Wells Fargo Investment Institute. “I think the true test of today will be what investors decide to do at the close, before the weekend.”

Crude oil prices continued to be traders’ main concern as it affects inflation and consumer sentiment. The latest oil future curves showed “markets are beginning to price a more persistent ‘higher for longer’ oil backdrop,” Barclays strategists including Emmanuel Cau said in a note. “This dynamic is reinforcing stagflation concerns.”

On Wednesday, Jerome Powell said the Fed will not lower interest rates until inflation cools, as it was too early to determine the impact of rising oil prices on the US economy. The central bank left rates steady for a second straight meeting.

“We think the Fed staying on hold remains the most appropriate positioning,” said Deborah Cunningham, chief investment officer for global liquidity markets at Federated Hermes. “The current conflict with Iran is nowhere near the magnitude of the disruptions seen during COVID, nor the 2008 global financial crisis, so there is no justification for cutting rates by hundreds of basis points.”

Stocks have unwound earlier gains too, with the Stoxx 600 now flat. The construction sector outperforms while energy stocks lag. Here are some of the biggest movers on Friday:

- CD Projekt’s share gain as much as 8.1%, the most since June, after it indicated it may release new gaming content to meet net income targets.

- Spire Healthcare shares jump as much as 11% after Sky News reported buyout firm Bridgepoint is drawing up proposals for a formal offer worth £1b for the UK operator of private hospitals.

- Elmos shares climb as much as 11% after Reuters reported the chip-equipment company is exploring a sale.

- Zabka shares rise as much as 2.7% after the convenience store chain said it saw a rebound in sales since mid-February.

- Inwit shares slide for a second day, as much as 9.7%, after the Italian tower company said Telecom Italia and Swisscom’s joint initiative to co-develop mobile towers will weigh on its growth.

- J D Wetherspoon shares drop as much as 11%, the most in a year, after the pub chain warned rising costs and pressure on consumer finances “may result in profits that are slightly below current market expectations” this year.

- Smiths Group shares fall as much as 5.5% to their lowest since July, after the UK manufacturing equipment group reported a somewhat light outlook.

- Fuchs shares fall as much as 4.7% to the lowest since November 2022 after the German manufacturer of automotive and industrial lubricants forecast profits for the year that missed the average analyst estimate.

Earlier, Asian stocks dropped as tech companies like Alibaba Group Holding and Taiwan Semiconductor retreated. The MSCI Asia Pacific ex-Japan Index swung between gains and losses before breaking lower as the session wore on, dropping as much as 0.6%. Markets in Japan, Indonesia, Malaysia and the Philippines were closed for a holiday. Tech giants Alibaba and Tencent lost $66 billion of market value in roughly 24 hours, after the market punished the twin leaders of China’s tech arena for failing to lay out clear visions for how to profit off artificial intelligence.

In FX, the Bloomberg Dollar Spot Index is rising though mixed against major currencies, with the yen lagging.

- USD/JPY rose 0.7% to 158.68, trimming weekly drop to 0.7%; Japanese markets were closed for a holiday on Friday. Tensions between the US and Japan over the Iran war remained evident as Trump hosted Prime Minister Sanae Takaichi, even as he said Tokyo was answering his call for support in the effort

- EUR/USD slipped 0.3% to 1.1555; European government bonds edged lower as money markets continued to price in a high chance of three rate hikes through 2026. During a summit in Brussels on Thursday, EU leaders expressed anxiety at the economic situation and called for a “moratorium” on strikes against energy facilities

- GBP/USD fell 0.2% to ~$1.34, while gilts extended Thursday’s drop triggered by a hawkish Bank of England stance; traders are betting on three hikes this year

In rates, yields rising across the curve in the US and Europe are being led by the short-end, with the UK underperforming for a second day, as bond markets extend their selloff as an initial paring in central bank rate hike bets in Europe reverses, as Brent crude edges toward new multiyear high close and Iran struck Arab states in the Persian Gulf. With US long-end yields only about 3bp higher, 2s10s and 5s30s spreads resume flattening, by 2bp and 3bp respectively. US 10-year is 4.5bp higher near 4.3% vs 9bp for UK counterpart, which reached 4.95%, highest level since 2008. A deeper selloff is gripping UK bonds as traders price in BOE rate hikes, while US short-term rate markets no longer see any chance of a Fed rate cut before next year. Fed-dated OIS contracts price in around 4bp of tightening for the April policy meeting; ECB swaps price in almost three 25bp rate hikes this year, while BOE swaps price in a combined 85bp of tightening by the December policy meeting.

In commodities, Brent crude futures have pared a gain of 2.4% to less than 0.2%, while US benchmark WTI crude is up 0.3%. Brent declined from its highest closing level since July 2022 to trade around $108 per barrel after Israel’s Prime Minister said the nation will no longer target energy infrastructure, and added that the war will end a lot faster than people think. Gold is fluctuating and now back below $4,700/oz. The precious metal is headed for the biggest weekly loss in six years, as war in the Middle East boosted energy and reduced expectations for rate cuts

There is no US economic data releases are scheduled, and Fed’s Bowman (8am) and Waller (8:30am) are slated to speak

Market Snapshot

- S&P 500 mini -0.4%

- Nasdaq 100 mini -0.5%

- Russell 2000 mini -0.5%

- Stoxx Europe 600 +0.2%

- DAX +0.4%

- CAC 40 +0.2%

- 10-year Treasury yield +4 basis points at 4.29%

- VIX +0.5 points at 24.55

- Bloomberg Dollar Index +0.2% at 1207.36

- euro -0.2% at $1.1567

- WTI crude little changed at $96.2/barrel

Top Overnight News

- The U.S. and its allies have intensified the battle to reopen the Strait of Hormuz, sending low-flying attack jets over the sea lanes to blast Iranian naval vessels and Apache helicopters to shoot down Iran’s deadly drones, American military officials said. WSJ

- Oil prices’ climb saw no letup as Iran pressed ahead with hitting energy assets. The country’s Revolutionary Guard insisted it is still building missiles and vowed the war will continue. Kuwait’s Mina Al-Ahmadi oil refinery shut down some units after a drone attack caused a fire. BBG

- Saudi Arabia’s oil officials are working frantically to project how high oil prices might go if the Iran war and its disruption of energy supplies doesn’t end soon—and they don’t like what they are seeing. The base case, several oil officials in the Gulf’s biggest producer said, is that prices could soar past $180 a barrel if the disruptions persist until late April. WSJ

- China is throttling exports of jet fuel, diesel and fertilisers, adding to fears in some of Asia’s biggest resource, manufacturing and agricultural nations that supplies could run short because of the war in the Middle East. FT

- Wall Street braced for $5.7 trillion in options set to expire in today’s triple-witching, which risks injecting yet more volatility into a market that’s seen weeks of turbulence. BBG

- In dollar terms, China’s GDP as a share of the global economy, peaked in 2021 at around 18.5%, when it grew to be around three quarters of the size of the U.S. economy. Many economists predicted China’s explosive growth would eventually make its economy bigger than that of the U.S. Instead China’s share of the pie has decreased, ending 2025 at around 16.5% of the global economy. It is now less than two-thirds the size of the U.S. economy, according to International Monetary Fund data. WSJ

- Australia’s 10-year bond yields rose to an almost 15-year high as mounting inflation concerns drove traders to ramp up bets on RBA rate hikes. BBG

- The ECB will need to consider hiking rates as soon as next month if price pressures build further due to the Iran war, Governing Council member Joachim Nagel said. Traders fully priced three rate hikes this year. BBG

- Trump is dialing back his mass deportation push, shifting focus toward targeting criminals on political and voter concerns. WSJ

- The Trump administration has delayed an executive order that could have required banks to collect and report more information on the immigration status of their customers, after Wall Street push-back: WaPo

- US President Trump said at dinner with Japanese PM Takaichi that the US is encouraged to see Japan buying US defence equipment.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly subdued but with downside limited as the region reacted to the recent oil swings, deluge of central bank meetings and mixed geopolitical headlines, while conditions were thinned - with the absence of Japanese participants due to the Vernal Equinox holiday. ASX 200 was dragged lower by weakness in the materials and commodity-related sectors, but with losses cushioned by strength in telecoms and defensives, while there were few fresh drivers overnight. Hang Seng and Shanghai Comp were following disappointing earnings results from the likes of Alibaba and CK Hutchison, with the former posting a 67% drop in Q3 net, which also weighed on other tech names. Furthermore, the PBoC's reiteration to continue implementing a moderately accommodative monetary policy and to use RRR and MLF to ensure sufficient stability did little to inspire, while China's Loan Prime Rate were unsurprisingly kept unchanged for the 10th consecutive month.

Top Asian News

- Chinese Commerce Ministry releases measures to boost travel services, CCTV reported; announces measures to expand inbound consumption.

- China's government is said to be urged to reform consumption tax in order to boost local income, according to China's Securities Journal.

European bourses kicked off cash trade on the front foot, rebounding from Thursday's losses. The IBEX 35 is currently bouncing the most, closely followed by the DAX 40. The FTSE 100 lags, weighed on by losses in oil majors and Smiths Group, as the Co. cuts its 2026 organic revenue growth to between 3-4% from 4-6%. Futures however dipped following reports the Trump Administration is reportedly considering plans to occupy or blockade Iran's Kharg Island to pressure Iran to reopen the Strait of Hormuz, according to Axios citing sources. Sectors point to a cyclical bias, with Construction and Materials and Banks sitting at the top of the pile. Energy and Media are the only sectors in the red.

Top European News

- UK Public Sector Net Borrowing Ex Banks (Feb) 14.3B vs. Exp. 8.5B (Prev. -30.4B).

- German PPI MoM (Feb) M/M -0.5% vs. Exp. 0.3% (Prev. -0.6%, Low. -0.1%, High. 0.7%).

- German PPI YoY (Feb) Y/Y -3.3% vs. Exp. -2.7% (Prev. -3%, Low. -3.1%, High. -2.1%).

FX

- DXY initial traded in a narrow range for most of the European morning before edging higher alongside crude following reports the Trump Administration is reportedly considering plans to occupy or blockade Iran's Kharg Island to pressure Iran to reopen the Strait of Hormuz, Axios reported citing sources. The index edged higher to a 99.60 peak from a 99.25 low, still a way off yesterday’s 100.23 peak.

- EUR/USD mildly pulled back overnight but trades relatively steady in a narrow range during the European morning. There have been several ECB speakers on the wires this morning, with Nagel suggesting that the ECB would need to hike in April if the price outlook sours, and will act with necessary resolve. The broad message by speakers suggested a meeting-by-meeting approach, echoing President Lagarde from her post-policy press conference. Pressure seen in recent trade on the aforementioned USD strength.

- GBP/USD trickled lower overnight after strengthening in the aftermath of the BoE decision. GBP clambered off its worst levels briefly at the start of the European session but is now trading at session lows as energy prices grind higher. Pressure seen in recent trade on the aforementioned USD strength.

- USD/JPY partially rebounds after slumping briefly below the 158.00 handle, while the mild recovery was facilitated by improved risk appetite, but with further momentum contained amid the absence of Japanese participants. JPY pressure was seen in recent trade on the aforementioned USD strength.

- Antipodeans initially tilted higher on a positive risk mood but has turned lower since as tone begins to sour, with added pressure following the Axios report on the Kharg islands.

FX

- ECB's Nagel said the ECB would need a hike in April if the price outlook sours, will act with necessary resolve.

- ECB's Makhlouf says the ECB is currently managing extreme uncertainty, adds that action will be taken if facts point to action. Every meeting is a live meeting.

- ECB's Rehn said no decision has been locked in ahead of time.

- ECB's Villeroy said rate hikes will be decided meeting by meeting and are totally determined to bring inflation back to 2%.

- ECB's Villeroy said ECB will remain vigilant and has the ability to act as needed.

- ECB's Muller said duration of high energy prices is key for ECB.

- ECB's Kazak said we know that inflation will go up and economy will slow, and will take stock in April.

- European Council appoints ECB's Vujcic as the central bank's Vice President to replace de Guindos as of June 1st.

- Barclays now forecasts ECB will raise rates by 25bps each in April and June vs. previous hold outlook.

- JP Morgan now expects ECB to hike interest rates in April and July, versus a previous forecast of holding rates unchanged throughout the year.

- Goldman Sachs now expects BoE to remain on hold throughout 2026 vs. prior forecast of quarterly cuts from July.

Fixed Income

- UST futures were initially on a firmer footing but are down some 3 ticks, largely moving in tandem with oil prices, with pressure seen across fixed income following reports that the Trump Administration is reportedly considering plans to occupy or blockade Iran's Kharg Island to pressure Iran to reopen the Strait of Hormuz. Earlier gains were limited after the recent choppy performance and curve flattening on hawkish central bank expectations in response to the Iran war.

- Bund futures trade lower amid the recent rise in crude prices. Upside has been contained following hawkish ECB reports yesterday, which noted officials see the need for possible rate hike talk to start in April, while ECB’s Nagel stated earlier the ECB would need to hike in April if the price outlook sours.

- Gilts underperform, with price action has been driven by the rebound in energy prices following the aforementioned Axios report, while markets are now fully pricing in 3 rate hikes by the BoE in 2026. As a reminder, the Bank kept rates unchanged with all 9 policymakers voting for a hold.

- China MOF sold 3-year bonds at 1.29% yield and 10-year bonds at 1.80% yield.

Trade/Tariffs

- Chinese media, SCMP, writes that the White Houses' Section 301 investigations may be less dramatic than war, but they risk retaliation and trade breakdowns.

- White House posted Fact Sheet on US-Japan alliance and stated it welcomes a second tranche of Japanese investments and that US and Japan reached a critical minerals action plan.

Commodities

- Crude futures initially traded with modest losses as the European session got underway but has steadily reversed higher following an Axios report stating that the Trump administration is considering plans to occupy or blockade Iran’s Kharg Island to pressure Iran to reopen the Strait of Hormuz. WTI regains the USD 96/bbl handle following the report, while Brent extends beyond USD 110/bbl. Comments from US Treasury Secretary Bessent late in Thursday’s session stated that the US could pursue another SPR release to keep prices down and may lift sanctions on Iranian oil but that has since been put in the rear view.

- Spot gold stabilises after its recent slide, although remaining on course for its worst weekly loss in six years following a deluge of hawkish-leaning central bank updates amid inflationary pressures driven by the war-related surge in oil prices. Spot gold resides in a USD 4,634-4,736/oz range.

- Copper futures have followed on from Thursday’s selloff as the dollar gains following the rebound in energy prices.

- SinoChem (600500 CH) reportedly cut throughput at its 300k BPD Quanzhou refinery to ~60%, sources say; also reduces operations at steam cracker to ~60%; seeking prompt delivery crude oil, including Russian oil under waver, to cover the supply gap.

- Russia is to limit major foreign container shipping companies from routes involving Russian ports unless they meet strict domestic control requirements.

- Spain is to reduce VAT on fuel from 21% to 10% to mitigate the impact of the Iran war, Ser Radio reported.

- Saudi officials see the base case for oil to rise to USD 180/bbl if the disruptions persist until late April, according to WSJ.

- EU member states to request EU Commission design national temporary and targeted measures to mitigate impacts on energy costs, according to a draft document.

- South32 (S32 AT) pauses production at the world's biggest manganese mine due to cyclone threat.

Geopolitics

- The Trump Administration is reportedly considering plans to occupy or blockade Iran's Kharg Island to pressure Iran to reopen the Strait of Hormuz, Axios reports citing sources.

- Iran announces the death of IRGC spokesperson Narini.

- Iranian Supreme Leader Khamenei said officials must compensate for the loss of the Iranian Minister of Security, Al Hadath reported.

- Iranian President said "the flames of war against us will affect many if the international community does not stand up to the aggression", Al Jazeera reported.

- Iran's Foreign Minister told his UK counterpart that providing military bases for the US will be considered as participation in aggression.

- Iran's IRGC spokesman, responding to Israeli PM, insists Tehran is still building missiles, AP reported.

- Iran's Revolutionary Guards report that missile manufacturing remains active amid conflict and stockpiles are sufficient.

- Iran is said to allow more Indian vessels to pass the Strait of Hormuz.

- IDF launches a wave of strikes on infrastructure targets across Iran.

- Explosion heard in Iranian city of Isfahan, according to Iran International.

- Saudi Arabia's eastern region saw further drone interceptions, with several threats destroyed.

- EU leaders call for de-escalation, civilian protection and full respect of international law by all parties, while they call for moratorium on strikes targeting energy and water infrastructure, also strongly condemned Iran's indiscriminate strikes.

- German Chancellor Merz said EU leaders have asked the European Commission to examine other possible ways of paying out loans to Ukraine.

US Event Calendar

- 8:00 am: United States Fed’s Bowman Speaks on Fox Business

- 8:30 am: United States Fed’s Waller Speaks on CNBC

DB's Jim Reid concludes the overnight wrap

Today will be the 15th trading day of the conflict so far and as I showed in yesterday's CoTD (link here), that is on average when we bottom out in US equities after a geopolitical shock. However it would be hard to trade on the back of averages at the moment with so much uncertainty so headlines will be more important than history here but if you're looking for optimism the normal geopolitical playbook would at least give you hope. So far we haven't deviated from it.

The news flow hasn't slowed down though, and there's been so much going on over the last 24 hours, even more over the last 36, that it's hard to know where to start. The main saving grace after another challenging session was that the price of Brent was well off the $119.13/barrel highs (+10.9% at that point) we reached around 9:30am London time yesterday, a couple hours after European gas futures opened up nearly +35%. They eventually closed +1.18% higher at $108.65/bbl and +13.15% at €61.85/MWh respectively, in turn their highest levels since July 2022 and January 2023. As I type this morning, Brent is at $107.31/bbl, coming off the highs as Israel and the US signaled a desire to avoid further strikes against energy infrastructure that had stoked the market turmoil late on Wednesday and early yesterday. That helped the S&P 500 (-0.27%) recover most of its initial losses, even as the STOXX 600 (-2.39%) earlier posted its worst close of 2026 so far.

Elsewhere, markets also had plenty of other events to react to, with the ECB, BoE, and other central banks across Europe holding policy rates steady in reaction to the ongoing conflict. However, some hawkish interpretations of those on hold decisions, especially that of the BoE, coupled with the energy concerns led to a big global bond sell-off at the front-end. This was most pronounced in Europe, with 2yr gilt yields registering their largest rise (+31bps) since 2022, with about half coming after the BoE meeting. 2yr bund yields rose by +14.5bps to 2.59%, their highest since July 2024. And in the US, 2yr Treasury yields spiked by as much as 15bps though they largely reversed this rise by the close (+1.6bps to 3.79%). At this point, the Fed is the only G10 central bank that is still (albeit very marginally) pricing easing later this year and at one point yesterday, markets no longer priced in cuts for the next few quarters for the first time in the Fed’s post-2024 easing cycle.

Before we delve into yesterday’s central bank decisions, the most recent developments on the Middle East has been an easing of fears that Wednesday's energy infrastructure attacks would spiral into something worse. That comes as Israel’s Prime Minister Netanyahu said yesterday evening that Israel would no longer target Iran’s energy infrastructure, with Donald Trump also saying that he had told Netanyahu not to attack Iran’s energy fields. Earlier yesterday, Iran’s Foreign Minister Abbas Araghchi posted on X that Iran would show “ZERO restraint if our infrastructure are struck again”, while mentioning the phrase “requested de-escalation”. All that left a sense that we could see a truce when it comes to strikes against energy facilities, even as there’s still little visibility on reopening the Strait of Hormuz or ending the overall war. Indeed, with the Pentagon reportedly asking the White House for a $200bn funding request to Congress, it may be readying for a more protracted conflict.

Some of the peak energy stress earlier yesterday had come as Qatar’s energy officials said that Iran’s attack damaged 2 out of its 14 LNG trains, which represent ~17% of Qatar’s LNG exports and that the damage will take “between three to five years to repair”. While this is likely to lead to lingering stress in the gas market, the easing of the oil market stress through the course of yesterday has brought Brent back to $107.31/bbl this morning. And WTI is down to $94.16/bbl, with the relatively more protected energy position of the US becoming more visible in market pricing.

The S&P 500 erased most of its -1% opening decline but still closed -0.27% lower. However, S&P 500 futures trading are edging +0.10% higher this morning, with those on the STOXX 50 up by a larger +0.64% after yesterday’s slump. Meanwhile, the combination of moderating geopolitical fears and relatively lower US yields saw the dollar index (-0.85%) post its worst day since August yesterday, while gold (-3.50% to $4,650/oz) fell to its lowest level in two months amid the global repricing in front-end rates.

Turning to those central bank meetings, the ECB left their deposit rate on hold at 2%, with President Lagarde exuding calmness in the press conference as she argued that the bank is “well positioned and well equipped” to deal with the energy shock. Lagarde’s comments suggested that the ECB would rather wait for evidence on second-round effects before deciding on any policy change. However, her comment that “we are starting from a good base” pointed to risks now being tilted towards hikes and she did not rule out more imminent action. Our European economists now expect 50bps of risk management hikes to 2.50% in the coming months, penciling June and September as the most likely timing. See their full reaction here. Following the meeting, Bloomberg reported that the ECB would be ready to raise rates as early as April if the Iran war pushed inflation too far above target, though a later hike could be more likely. With this backdrop, market pricing of an April hike rose from 36% to 63% on the day, with about 66bps of ECB hikes priced by year-end.

But it was the BoE that delivered the clearest hawkish surprise versus expectations, even as it held the Bank Rate steady at 3.75%. For the first time since September 2021 the decision was a 9-0 vote, confounding expectations that a couple members would still favour a cut. And the MPC stated that it would “stand ready to act” to contain inflation at the 2% target, removing the earlier easing bias. So while Governor Bailey cautioned later in the day against jumping to “strong conclusions”, investors dialled up expectations of BoE rate hikes in 2026 to +70bps (+49bps on the day), with a 53% chance of a hike priced in for April. Our UK economist has changed his call to no longer expect any rate cuts this year, with the prospect of rate hikes also possible should limited fiscal support to curb inflation materialise, and if the Iran conflict lasts into April and beyond. You can see his full take here.

The hawkish BoE decision, the timing of which coincided with the bond market open in the US, triggered a sharp front-end selloff as discussed at the top. The moves were more modest further out the curve, though 10yr bonds also sold off across the continent, with gilt (+10.8bps), bund (+1.7bps), BTP (+5.0bps) and OAT (+3.6bps) yields all moving higher. The underperformance in BTPs came after Italy announced yesterday that it would make a temporary 20-day tax cut on fuel, becoming the first large European country to use fiscal measures to alleviate surging energy costs. Meanwhile, the energy fears saw many European equity indices fall by more than 2% yesterday, including the STOXX 600 (-2.39%), FTSE 100 (-2.35%), DAX (-2.82%) and CAC 40 (-2.03%), although part of that was due to Europe catching up to Wednesday’s overnight news of Iran’s attack against Qatar’s LNG facility.

In terms of the other central bank decisions, the Riksbank left its policy rate at 1.75%, with the governor saying that it is expected to remain at this level for some time, though alternative scenarios showed a wide range of uncertainty on the rate path ahead. Finally, the SNB left policy rates at zero while incorporating their new, higher willingness to lean against Swiss Franc strength into their policy statement. See more from our FX strategists here.

Asian equity markets are fairly quiet this morning which can only be a positive thing at the moment. Japan is closed for a holiday with the Hang Seng (-0.63%) and the S&P/ASX 200 (-0.82%) lower but with the KOSPI (+0.52%) higher again on the back of tech stocks, and is now up over 5% this week.

In monetary policy action, China’s central bank kept its loan prime rates unchanged for a tenth straight month, with the one-year LPR held at 3.00% and the five-year rate, which influences mortgage pricing, at 3.50%, in line with market expectations.

To the day ahead now, we’ll get the UK’s February public finances, Germany Feb PPI, Italy January trade balance, current account balance, ECB January current account, Eurozone January trade balance, Canada January retail sales. The ECB’s Nagel will also speak today.

![The 20th Annual ‘Women Of Power’ Summit Finishes Strong With Powerhouse Programming [PICS]](https://blackenterprise-prod.b-cdn.net/wp-content/blogs.dir/1/files/2026/03/IMG_2881-1024x688.jpeg)

{kind=link}

{kind=link}