Submitted by Criterion Research President, James Bevan,

The geopolitical calculus underpinning global LNG supply through the early 2030s has shifted materially. Iranian drone strikes on Qatari LNG trains, delays to key expansion projects, and the indefinite closure of the Strait of Hormuz have created a compounding threat to Qatar's LNG position that goes well beyond a construction delay. What had been framed as a two-horse race for global LNG market share now looks considerably more one-sided. The beneficiary is clear: U.S. Gulf Coast LNG.

At Criterion Research, our outlook is for US LNG exports to nearly double by 2030, with further upside in the coming decade.

Qatar's Gap Is Large and Getting Larger

While Qatar’s loss of 12.8 MTPA for 3 to 5 years due to Iranian strikes is a serious blow to Qatar’s 77 MTPA export capacity, it is not a global catastrophe on its own. What is worrying is that Iran has demonstrated the potential for further strikes, which means that even restored capacity cannot be treated as a stable floor. Even if onshore facilities are repaired and the Strait is nominally reopened, LNG tanker operators and their insurers are unlikely to resume normal transits until they have, over time, earned confidence that vessels are not exposed to strikes or mines. That confidence cannot be declared by a government. It has to be proven through sustained safety in a conflict environment with no clear resolution, a process that could take months or years, regardless of the physical state of Qatar's terminals. Molecules that cannot move to market are effectively stranded, and the Strait of Hormuz shipping constraint is the piece that is hardest to resolve through engineering or diplomacy alone.

Beyond current Qatari volumes being impacted, Qatar's three-phase North Field expansion program, encompassing NFE, NFS, and North Field West, was designed to lift total liquefaction capacity from 77 MTPA to 142 MTPA by 2030. Global LNG demand was counting on these volumes. All three phases now face indefinite delays, with no official revised timeline and no near-term path to resuming offshore construction. NFE’s first train had already slipped to a 3Q26 start before the suspension, and rumors say it was pushed to 2027 before strikes began.

Taken together, disruption to the existing base and delay of the full expansion program represent a potential swing of well over 100 MTPA relative to what the market had been counting on through the early 2030s. No other supply source can replace that on a compressed timeline.

The U.S. Fills the Void

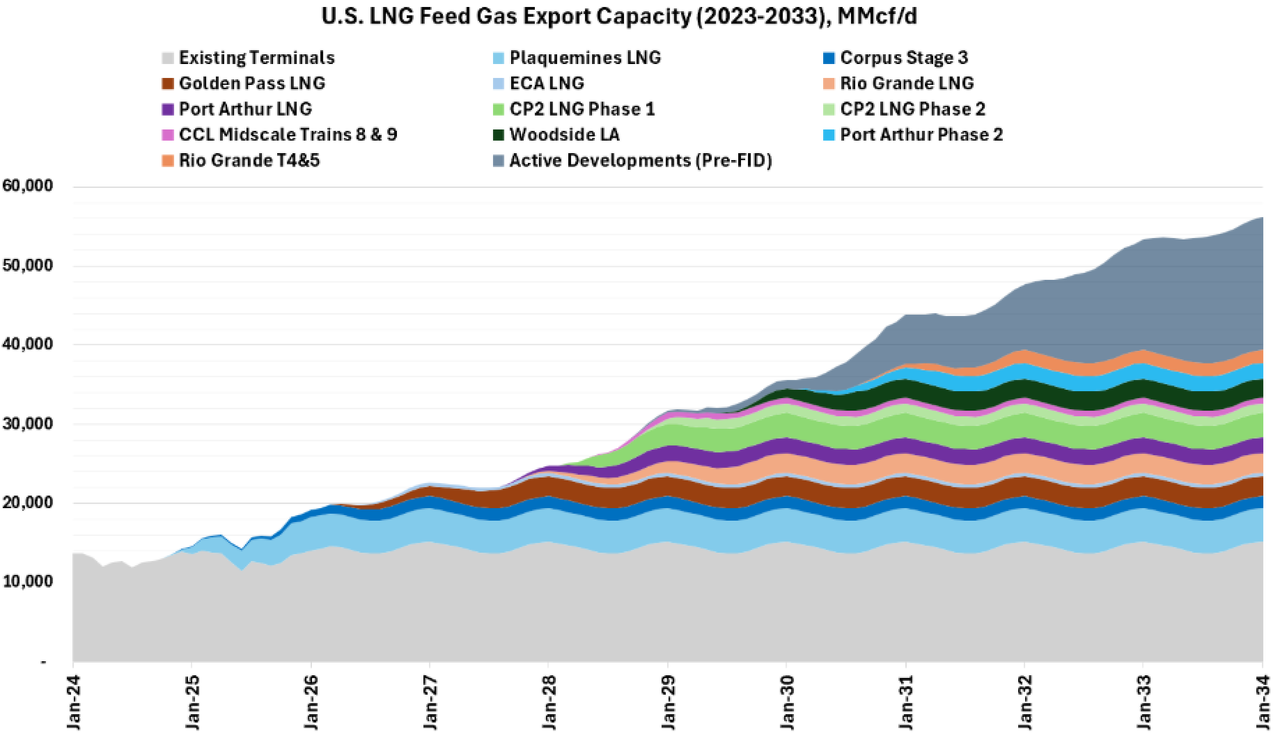

The U.S. project queue was already moving aggressively before Qatar's situation deteriorated. According to our data at Criterion Research, Golden Pass LNG is in active commissioning, CP2 Phase 1, Port Arthur, and Rio Grande LNG are all on track for first production in 2027, following, and CP2 Phase 2 reached FID. Post-FID US projects alone are expected to reach 39 Bcf/d by 2033. While the US cannot make up for the lost Qatari volumes before 2030, there is a strong pipeline of pre-FID projects for early 2030 and beyond that may now be pushed over the edge by new customer demand replacing Qatari volumes.

The Demand Caveat

The bull case is real but not unconditional. Whether demand materializes at the volumes required to absorb the full U.S. buildout depends heavily on price, and the infrastructure required to convert price-sensitive demand into actual imports remains well behind schedule. Across South Asia and Southeast Asia, the buildout of regasification terminals and downstream gas distribution that was supposed to undergird the bullish demand case for the 2030s has been repeatedly delayed by a combination of high prices, fiscal constraints, and the improving economics of competing renewable alternatives. The regas infrastructure that is not built in the late 2020s cannot absorb volumes in the early 2030s, and that pipeline of delayed or canceled projects represents a real ceiling on how quickly emerging-market demand can respond, even if prices fall to attractive levels. Paradoxically, a supply shock of this magnitude could push prices high enough to further delay that infrastructure buildout, suppressing the very demand growth that would otherwise absorb U.S. volumes. The structural demand from Europe and Northeast Asia, anchored by long-term contracts and supply security mandates, is likely to hold regardless. But the incremental emerging-market demand that was supposed to keep the market balanced through the mid-2030s now appears considerably more uncertain than the pre-conflict consensus assumed.

The Structural Conclusion

Seldom has a supply disruption of this magnitude aligned so cleanly with a competing exporter's buildout window. The U.S. has a well-financed project pipeline, while its most capable competitor is facing key expansion delays, operational damage, and a shipping constraint that may outlast both. LNG dominance for U.S. LNG looks increasingly certain. Whether that translates into strong project economics across the board depends on which demand pools ultimately clear, and at what price.

![The 20th Annual ‘Women Of Power’ Summit Finishes Strong With Powerhouse Programming [PICS]](https://blackenterprise-prod.b-cdn.net/wp-content/blogs.dir/1/files/2026/03/IMG_2881-1024x688.jpeg)

{kind=link}