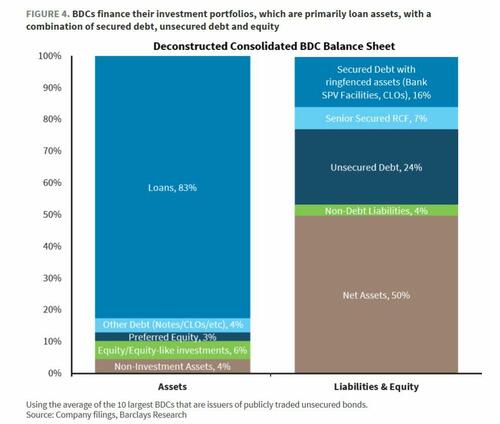

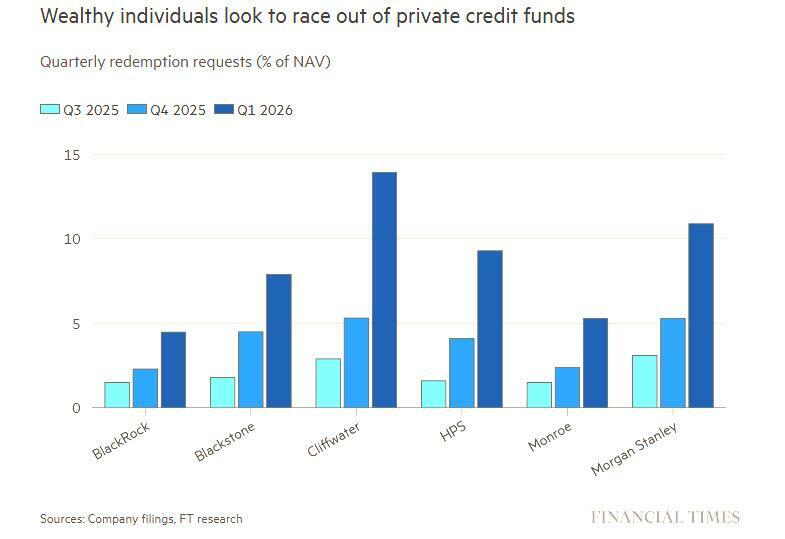

Amid the ongoing fracturing of the private credit industry, which after enjoying years of stable, levered growth (and when it ran out of institutional greater fools, it aimed lower, toward HNWs and retail) finally hit a brick wall thanks to the Claude-inspired SaaSpocalypse, which has led to a historic surge in redemption requests across the biggest (and certainly smallest) names in the industry, last week we said that debt funds managed by powerhouse firms including Blackstone, BlackRock, Cliffwater, Morgan Stanley and Monroe Capital have agreed to honor only 70% of the $10.1bn of redemption requests they have faced, according to FT calculations, as fund after fund is gating investors.

We also said that the number of both redemptions and gates is expected to spike over the coming weeks, as funds managed by Ares Management, Apollo Global, Blue Owl, Oaktree and Goldman Sachs tally up how many of their investors are heading for the exits, as discussed here.

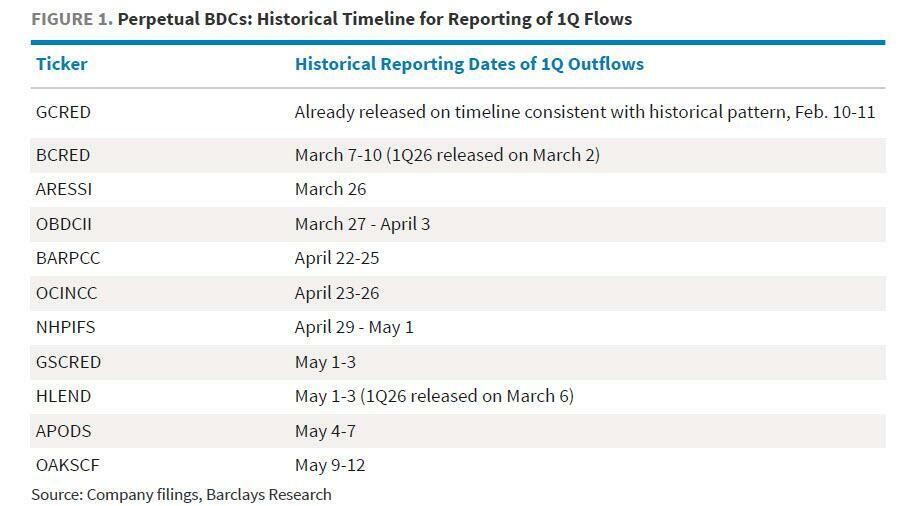

According to the above table, Apollo's private credit fund, APODS, was supposed to report its Q1 outflow in early May. However, the surge in redemptions was so big the private equity giant decided not to wait that long, and according to Bloomberg, Apollo Global Management has joined a growing number of its peers in gating redemptions from one of its largest non-traded private credit funds for retail investors, becoming the latest alternative asset manager to be flooded by a surge in such requests.

The $25 billion business development company, Apollo Debt Solutions (APODS), capped withdrawals at 5% of outstanding shares Monday after clients sought to redeem 11.2%, according to a shareholder letter seen by Bloomberg, thus gating more than half of the redemption requests.

"Periods of complexity and uncertainty can create some of the most attractive investment opportunities, but only for those with the flexibility to act decisively,” the firm said, adding that “while the market has repriced risk, the fundamentals of the fund’s underlying borrowers remain strong."

The firm expects the granted redemptions to amount to roughly $730 million of gross outflows for the first quarter, offsetting the roughly $724 million of inflows for the period. Apollo Debt Solutions has been building its reserves in the past month, doubling the size of one credit line to $1 billion and signing a new $500 million facility.

What's worse is Apollo has effectively pre-gated next quarter's redemption requests, saying that it intends to stick to the same cap next quarter as it balances “the interests of shareholders seeking liquidity with those who choose to remain invested,” it said in the letter, noting that challenging times can benefit investors in the long run.

With redeeming investors receiving just 45% of their capital, Apollo Debt Solutions is returning less cash to clients than some of its peers that capped withdrawals. As we reported previously, while BlackRock also capped redemptions from its $26 billion non-traded BDC at a pre-set 5% earlier this month, investors had "only" requested 9.3% of their shares. Meanwhile, Morgan Stanley’s North Haven Private Income Fund’s pro-rated redemptions were granted at a similar rate to Apollo’s.

It seems that with every passing week, after Blue Owl started the private credit firesale a month ago, more investors are seeking to return their capital... and more are being gated.

As regular readers are aware, while private credit funds typically limit redemptions to 5% of outstanding shares, the recent bank run redemption scramble among retail investors has tested firms’ flexibility. Some firms such as Blackstone opted to exceed the cap - and fund the shortfall out of the partners' own pocket - in the hopes of quelling investor panic and stanching further outflows. That valiant effort failed after Blackstone's peers such as Blackrock, Cliffwater and Morgan Stanley gated their own investors.

Apollo, which has been pushing for more transparency in private markets, also said Monday that Apollo Debt Solutions had returned 1% over the past three months. At the same time, its net asset value dipped by 1.2% over the same period. Last night we reported that the largest private credit fund, Blackstone's BCRED, reported its first monthly decline since September 2022.

Meanwhile, in related news, late on Monday a private credit fund jointly run by Future Standard and KKR was the first to get junked, losing one of its investment-grade ratings, a rare occurrence in the $1.8 trillion private credit market, and one which will certainly result in higher borrowing costs for the $14 billion investment vehicle.

Moody’s Ratings lowered its assessment of FS KKR Capital Corp. to Ba1, or one level into junk, because of what it described as “continued asset quality challenges” that have hurt profitability and the value of the fund’s portfolio relative to peers, the credit grader said in a statement on Monday.

The fund’s non-accrual rate, which measures soured loans, rose to 5.5% of total investments as of the end of last year, one of the highest percentages among peers. It also expressed concern over other investments not classified as non-accrual that have have suffered significant markdowns, including a loan to software company Medallia.

The rating agency also called out FSK’s higher proportion of payment-in-kind income relative to peers, which it said is a sign of “weaker earnings quality.” PIK provisions allow borrowers to pay interest by accumulating additional debt instead of paying out cash.

That said, the ratings firm said the fund is “well positioned” from a liquidity perspective, with about $2.5 billion available after repaying a $1 billion note earlier this year.

“FSK remains well positioned despite the decision,” a spokesperson for the fund, referring to its stock-exchange ticker, said in an emailed statement. “It has a strong, well‑laddered liability structure with no 2026 unsecured maturities and limited near‑term maturities, enabling us to continue supporting our portfolio companies and navigate the current market environment.”

And now it's junk.

![The 20th Annual ‘Women Of Power’ Summit Finishes Strong With Powerhouse Programming [PICS]](https://blackenterprise-prod.b-cdn.net/wp-content/blogs.dir/1/files/2026/03/IMG_2881-1024x688.jpeg)

{kind=link}

{kind=link}