Submitted by QTR's Fringe Finance

This morning I warned (again) this wasn’t a normal market in private credit. It was a liquidity event. And today it’s becoming something else too.

According to the Financial Times, the SEC is now questioning whether Egan-Jones, a small but deeply embedded credit rating agency in private credit, can “consistently produce credit ratings with integrity.” That’s not a routine inquiry. That’s the regulator openly wondering whether one of the key cogs in the machine was ever doing its job properly in the first place. Think S&P during The Big Short…

And the timing is almost too perfect.

Because just as gates go up, withdrawals get capped, and investors start asking for their money back, the conversation is shifting from “everything is fine” to “who signed off on this?”

That shift matters just as much as the redemptions.

For years, private credit sold stability. It worked because nobody had to test it. As long as money kept coming in and nobody needed to get out all at once, the system held together. You know, kinda like Madoff.

Now people are trying to get out, and suddenly the inputs behind those reassuring return streams — the marks, the models, the ratings — don’t look quite as solid. So naturally, we arrive at the part of the cycle where everyone starts looking around the room for someone else to blame.

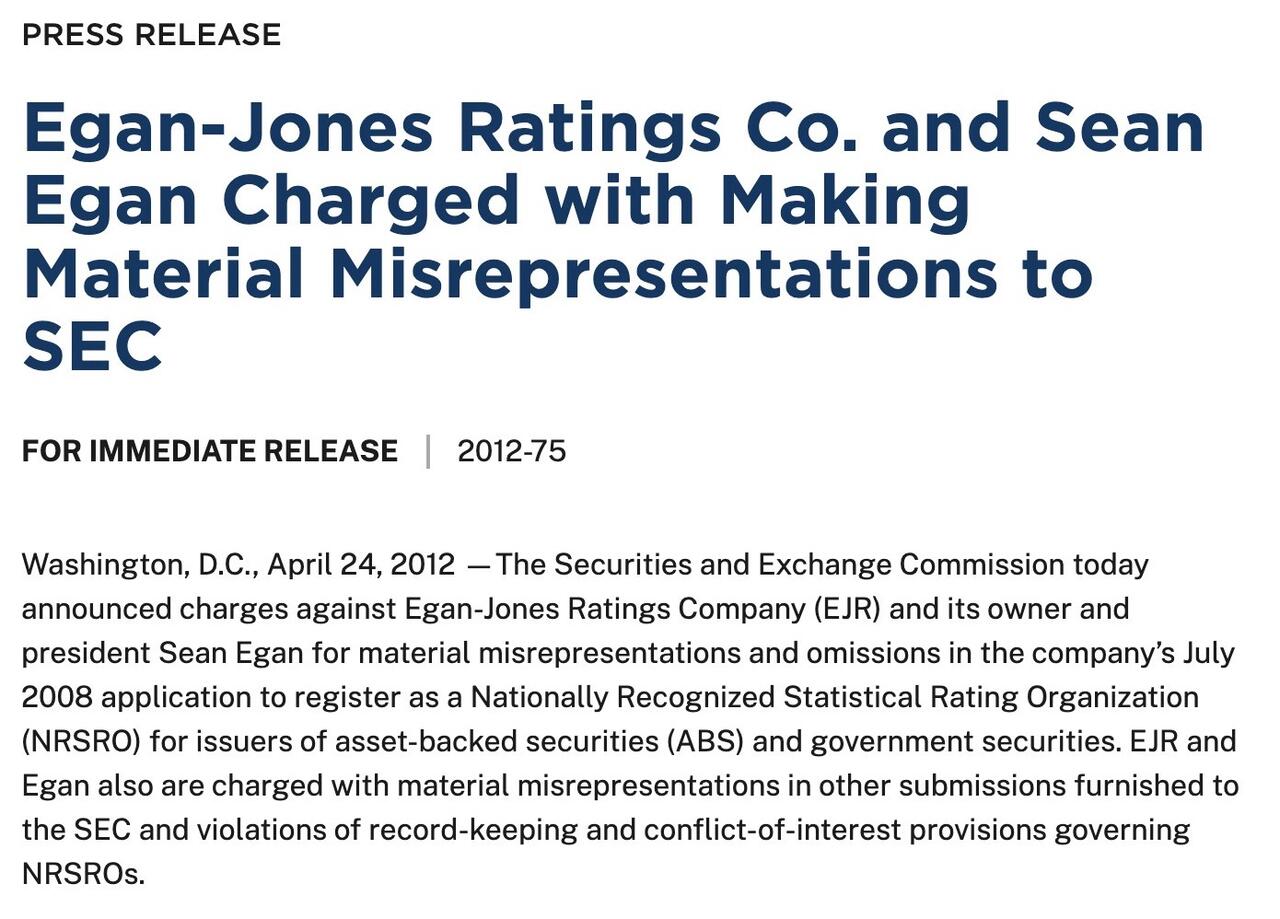

Egan-Jones is an easy place to start. For years, it has faced recurring regulatory scrutiny, primarily from the U.S. SEC, over conflicts of interest, disclosure practices, and internal controls tied to its business model. The most significant action came in 2012, when the SEC charged the firm with misrepresenting its expertise in rating asset-backed securities, resulting in fines and a temporary suspension from rating certain structured products. Ongoing concerns have centered on compliance systems, documentation, and transparency, highlighting tensions between its independent approach and NRSRO regulatory standards.

A small shop with a big footprint, issuing thousands of ratings on private loans that insurers rely on for capital treatment. If those ratings are even slightly generous, or just structurally flawed, then the implications stretch far beyond one firm. It raises the uncomfortable possibility that risk across the system wasn’t just misunderstood, but conveniently packaged to look safer than it was. Again, the analogues to the housing crisis are easy to identify.

And this idea takes hold, it doesn’t stay contained. Managers distance themselves. Investors get louder. Regulators, even reluctant ones, start asking questions they would have preferred not to ask.

Which makes this even more interesting, because this SEC has hardly been spoiling for a fight. In fact, just yesterday news broke that the acting head of enforcement, effectively the agency’s top cop, is stepping down after reportedly pushing for more aggressive action than leadership wanted.

So if this group is starting to publicly question the integrity of ratings in private credit, it’s probably not because they woke up feeling ambitious. It’s because the pressure is getting hard to ignore.

That’s how these things usually go. Not with a bang, but with a slow, reluctant acknowledgment that something underneath the surface isn’t right. Kicking the can down the road continues literally as long as it’s humanly possible.

And now private credit is still a liquidity event, but it’s evolving into a credibility event at the same time. As the blame starts getting handed out, don’t be surprised if a few more “previously respected” pillars of the private credit boom suddenly look a lot less sturdy. The blame game is just getting started and there could be plenty more of it to go around in coming weeks.

Tracking the private credit meltdown:

- March 24, 2026 - SEC questions Egan-Jones' ratings in private credit

- March 24, 2026 - Ares restricts withdrawals on its Strategic Income Fund after redemption requests hit 11.6%

- March 23, 2026 - Apollo caps withdrawals on its $25 billion Apollo Debt Solutions vehicle after redemptions hit 11%

- March 19, 2026 - Stone Ridge’s Alternative Lending Risk Premium Fund gates redemptions after overwhelming redemption requests

- March 16, 2026 - Apollo co-president says that “all” marks in parts of the private markets industry are “wrong”

- March 11, 2026 - Morgan Stanley and Cliffwater cap redemptions in $8 billion, and $33 billion funds, respectively

- March 6, 2026 - BlackRock begins limiting withdrawals from its $26 billion HPS Corporate Lending Fund

- March 3, 2026 - Blackstone faces “record” redemptions from its flagship private credit vehicle, investors sought to redeem 7.9% of fund’s $82B in assets

- February 19, 2026 - Blue Owl restricts redemptions from its retail private credit fund

- January 26, 2026 - Blackrock takes 19% markdowns on TCP Capital Corp.

- December 17, 2025 - Blue Owl walks away from $10 billion data center deal for Oracle

- October 15, 2025 - QTR warns private credit is one of 10 areas of the market that I would avoid heading into 2026

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

{kind=link}

{kind=link}