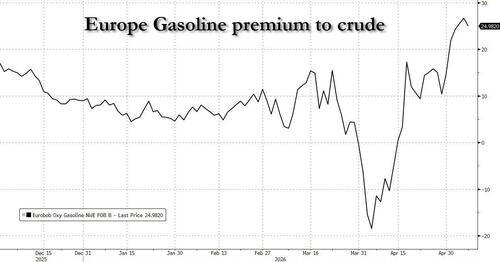

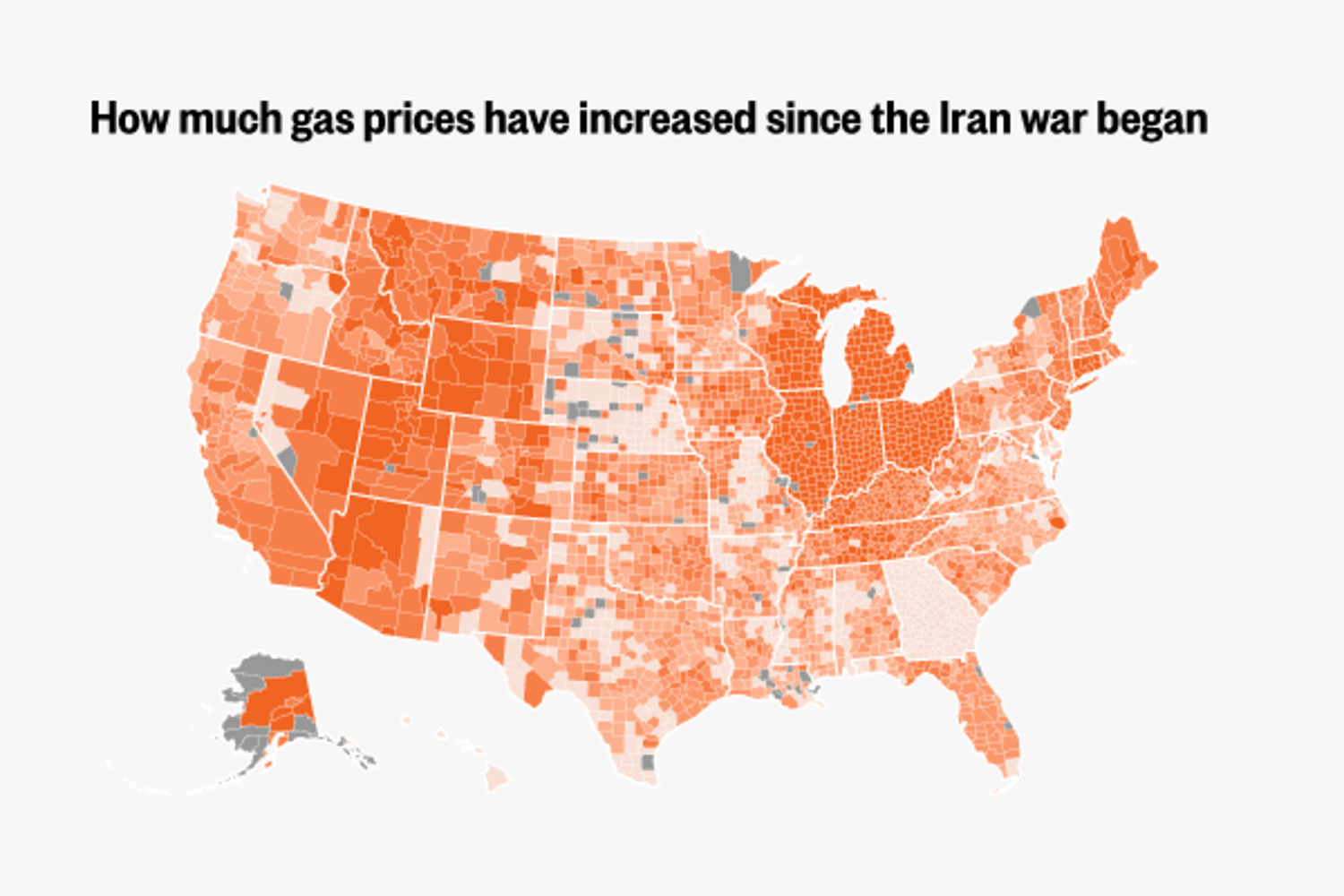

Yesterday when discussing China's unexpected flip-flopping on its decision to order local banks to ignore the latest US sanctions on Chinese, followed days later by a demand that they pause loans to sanctions refiners, we highlighted something remarkable: in the aftermath of the Strait of Hormuz blockade, which throttled the transit of ~10% of global oil and sent physical prices soaring to record highs (especially for Dubai crude), resulting in a windfall for European refiners thanks to soaring gasoline premiums...

... the reaction in China was a mirror image, as already razor-thin independent refiner (teapot) margins plunged to record negative.

The reason for the margin collapse was China’s domestic fuel policy: it has long been Beijing's policy to soften price hikes to help shield consumers and avoid social unrest; which while beneficial to end consumers is catastrophic to refiners and processors who are prohibited from passing on rising costs. In other words, Chna’s "energy security" was the dominant theme, and if it meant an entire industry has to suffer huge losses if it continues to purchase oil and process it into various product grades.

Ordered to process as much available inventory as possible, that's what the refiners have done, and refining rates in Shandong province, China's hub for smaller refineries known as teapots, ramped up over April to the highest level in almost two years, as processing margins cratered to record negative levels meaning refiners are losing record amounts on every barrel they process.

“I would not be surprised if the teapots are prioritizing politics over economics with an eye to their long-term survival,” said Erica Downs, a senior research scholar at Columbia University’s Center on Global Energy Policy. “They may be calculating that if they do their part to help China weather the energy crisis, then maybe they will build up some goodwill in Beijing.”

While Downs is right, and teapots are prioritizing politics, they are also certainly keeping an eye on economics to the extent they can avoid Beijing's wrath, and predictably the logical consequence of this centrally-planned policy to force "independent" refiners (who are not really independent if they have to do whatever Beijing instructs them) to make fuel at record losses to ensure energy security, is for them to slash purchases of Iranian crude.

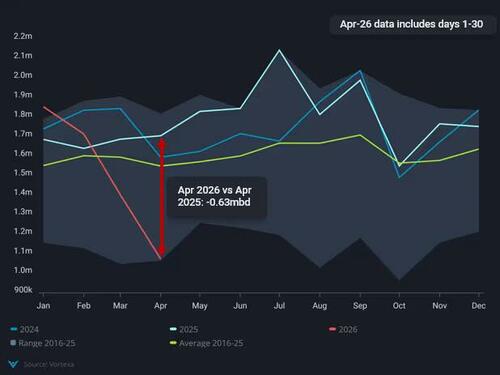

Sure enough, Chinese crude oil imports have plunged: according to Vortexa, China's April imports plunged to a multi-year low of just 8.2 million barrels a day, down by about a quarter from a prewar level of around 11.7 million. The 3.5-million barrels a day swing almost matches the total consumption of Japan and is double the amount supplied by the United Arab Emirates pipeline that circumvents Hormuz.

As Bloomberg's Javier Blas writes overnight, "simply put, it’s huge, perhaps the second- or third-largest factor rebalancing the oil market today, behind only Saudi Arabia’s own pipeline bypassing the strait and the use of the strategic petroleum reserves of the US and Japan."

The import drop might make sense if Chinese commercial inventories were falling sharply, or if Beijing had tapped its strategic petroleum reserves. But neither appears to be happening. Instead, commercial stockpiles have continued to increase in recent weeks, according to satellite data (of course, China is well known to manipulate all data and with the bulk of its 1.4 billion in strategic oil reserves located underground, it is impossible to trace flows definitively)

Meanwhile, as imports have collapsed, inventories at sea have piled up: Kpler reports that there are now about 16 million barrels on ships anchored in the Yellow Sea off the Chinese coast, almost 40% higher than the level prior to a US blockade of Iran’s ports in mid-April as oil that was ordered previously remains unused.

There has been another complication: after the Iran war broke out, Beijing banned exports of refined products, effectively allowing refineries to process less crude to meet domestic demand. But the policy has now been reversed, suggesting the country sees enough fuel availability.

In any case, in recent weeks, Blas writes that amid this collapse in Chinese imports, industry executives have noticed something odd: Chinese state-owned oil companies have been reselling some of their oil cargoes to European and Asian rivals. The behavior suggests surpluses, which is "odd" to say the least during a supply shortage. Where is this excess oil coming from (for the answer, see below).

The shift has not only capped benchmark oil prices, but also helped to trigger a collapse in the premia that traders pay above them to secure physical crude. The immediate outcome has been a very beneficial one: physical barrels that in early April went for $30 above benchmark prices are now changing hands at premiums as low as $1. Talk of discounts has even started to emerge.

Underscoring this point, North Sea oil traders don’t appear as desperate for crude for immediate delivery anymore, compared to the panic buying of late March and early April

While the collapse in refining margins is a clear clue to the plunging oil imports, other questions remain: chief among them how is China importing far less crude than before without running down stocks? In the past, the country clearly bought more oil than it needed, building a huge emergency stockpile. Today, China has nearly 1.4 billion barrels in its reserves according to media reports, well above the 400 million of the US and Japan’s 260 million. As we reported in late 2025, China probably bought one million barrels a day more than it needed last year. By simply stopping beefing up the reserve, China can cut imports a lot without affecting its underlying oil needs.

The shift can explain, perhaps, a third of the import cut. But the rest? Here’s where oil traders speculate with different theories. One argument says that Chinese economic activity is weaker than previously thought, and thus oil consumption growth is also lower. What’s the catalyst for that slowdown? Perhaps the impact of the war on several of China’s clients in the region, including the Philippines, Vietnam and Thailand (just don't look for validation in Chinese economic "data" - like everything else, it took is centrally planned and Beijing would never confirm its economy is being hit due to the Iran war as that would mean reduced political leverage).

Separately, the increase of electric vehicles, improved public transportation and the option of working from home have made Chinese households better able to cope with higher oil prices.

Unlike most other nations in the region, China hasn’t announced any emergency action to rein in demand, like adopting a four-day work week for government employees or promoting carpooling.

The IEA estimates that Chinese oil demand slipped into a modest year-on-year contraction in both March and April, down by about 110,000 barrels a day to about 17 million barrels. While the drop is impressive when compared with the exuberant growth of the country’s consumption in the past, it isn’t nearly enough to explain why imports have fallen so much.

It is certainly possible that Chinese oil demand has been contracting far more sharply than currently thought, The key, Blas reckons, is the inscrutable petrochemical industry - the sector that has contributed the majority of oil consumption growth over the last five years. In petrochemicals, China is unique. On top of its traditional industry that uses oil and natural gas as feedstock, it has parallel production that relies on coal.

Since the war started in late February, coal-to-chemicals profit margins have improved markedly. The industry had typically operated with plentiful spare capacity, so there’s room for a significant shift to coal from oil as a chemical feedstock. Hard data is scarce but, anecdotally, petrochemicals plants transforming coal into plastics like polyethylene, polypropylene and polyvinyl chloride have been running hard for the last 60 days, in turn reducing consumption of traditional feedstocks such as ethane and naphtha.

So perhaps China has managed to rely far more on coal-to-chemicals than previously thought. Another possible explanation is that it’s running down hard-to-track inventories of semi-finished plastics and other chemicals, making the recent drop in oil consumption in the petrochemical industry an unsustainable one-off unless there is a global recession which collapses end-demand for Chinese plastics exports.

And then there are the more banal explanations. Although oil traders try to estimate Chinese inventory data with the use of satellite data, it is in fact possible that observers are missing locations and stocks are, in fact, falling. About two months ago, we hinted that Chinese drain of its SPR could more than offset a full Hormuz blockade for a long time. As we said on March 18, "China can avoid any Gulf imports for months and drain its SPR instead."

One relevant question: what is China's pace of SPR drain if any. Recall for the past year Beijing was adding about 500-700K in daily SPR stockpiles; total is said to be ~1.4 billion barrels. China can avoid any Gulf imports for months and drain its SPR instead.

— zerohedge (@zerohedge) March 18, 2026

Sure enough, Blas writes that the oil market has been full of chatter about China quietly tapping its strategic reserves, starting by using underground caverns that no one can see using satellites. Maybe. Time lags may also be playing a role; Chinese domestic oil production has been increasing, too, perhaps helping to plug any gaps.

But, as Blas concludes, "make no mistake, China is rebalancing the oil market today." The bigger question is for tomorrow when the Strait is (eventually) unblocked: If China can reduce imports so drastically without having to take extreme measures, what does that say about the future of oil consumption there? Nothing positive for oil bulls, that's for sure.

.png?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}