US equity futures are off a touch as the US/IranIran failed to consummate a deal, which is boosting Energy commodities and bond yields. Still, stocks have withstood the resulting increase in oil prices and higher bond yields as the market remains focused on the memory/semi stock bubble. As of 8:00am ET, S&P and Nasdaq 100 futures are down fractionally as Trump and Iran rejected each other’s latest peace proposals to end the 10-week conflict as the two sides struggle to maintain a fragile ceasefire. In premarket trading, semis are bid again after surging to a record high on Friday, Mag7 are mostly lower as early action points to Defensive positioning with Energy plays acting as a long hedge. European stocks are lower, reversing earlier gains in Asia, there driven by the AI Theme / Memory as Korean indices added 4-5%, and were briefly halted at the +5% trigger. Bond yields higher across the world on fears of an oil-driven inflation shock and expectations of central banks tightening monetary policy. The 10-year Treasury rate rose four basis points to 4.39%. The dollar edged 0.1% higher, while gold dipped below $4,700 an ounce. In commodities, the Energy complex is leading but WTI remains below $100/bbl, and off session highs, silver is outpacing gold as base metals are bid, and Ags are mixed. Today’s macro data focus is on existing home sales (10am ET) before kicking off a data-heavy week highlights by CPI, PPI, and Retail Sales. Fed speaker slate empty for the session.

In premarket trading, Mag 7 stocks are mostly lower:Apple +0.2%, Meta -0.6%, Microsoft -0.8%, Amazon -0.6%, Nvidia -0.5%, Alphabet -0.9%, Tesla -0.6%

- Semiconductor stocks are rising, set to extend gains, after many chip stocks closed at record highs on Friday. The latest surge is boosted by continued investor enthusiasm over AI infrastructure build-outs. Among notable movers: Intel (INTC +6%), Micron (MU +5%)

- Babcock & Wilcox (BW) rises 12% after the power equipment company reported revenue that grew 44% year-over-year in the first quarter, as well as adjusted Ebitda that nearly quadrupled.

- Beazer Homes USA Inc. (BZH) rises 22% as people familiar with the matter say Dream Finders Homes Inc. is close to announcing a $704 million offer to acquire the rival homebuilder.

- Certara (CERT) slips 5% after the biotech company cut its adjusted earnings forecast for the full year. The firm also posted adjusted profit for the first quarter that fell short of Wall Street’s expectations.

- Liquidia (LQDA) rises 7% after the drugmaker posted revenue for the first quarter that beat the average analyst estimate.

- Lumentum (LITE) rises 4% after Nasdaq announced that the stock will join the Nasdaq 100 Index, replacing CoStar Group. prior to the market open on May 18.

- Moderna (MRNA) rises 8% in the wake of Friday’s 12% rally after the company said last week it’s researching vaccines to protect against hantaviruses.

- Monday.com (MNDY) soars 25% after the software company raised its full-year forecast for both revenue and adjusted operating profits. It also reported first-quarter results that beat expectations.

- Mosaic (MOS) falls 3% after forecasting phosphates sales volumes for the second quarter that missed the average analyst estimate.

- Target Hospitality (TH) gains 11% after the provider of modular housing boosted its year sales forecast.

Global equities are trading at record highs following a narrow tech-led rally that’s been driven by strong earnings and resurgent optimism around artificial intelligence, even as the war continues. This week, investors will be watching Trump’s visit to China’s Xi Jinping to see whether they can influence the situation surrounding the conflict.

The high in stock markets “does make sense,” Grace Peters, global head of investment strategy at JPMorgan Private Bank, told Bloomberg TV. “The underlying driver is more capex being spent. That’s not just associated with the AI buildout, but governments directing capital and companies following suit.”

The modest moves in futures signal traders are pausing for breath after 6 straight weeks higher, as they break down the latest Iran war news before a spate of key economic readings. With most of the earnings season in the rear-view mirror, much of the focus this week is on the CPI print Tuesday, Wednesday’s PPI numbers and retail sales on Thursday. Bloomberg Economics expects April CPI to moderate from March’s strong pace to a monthly increase of 0.6% - still pretty hot. Core CPI should also be elevated, but not because of the Iran war or tariffs. In fact, many tariff-related goods have seen deflation. Rather, core strength will be driven by a rectification of the artificial understatement in shelter CPI from the government shutdown last October.

“The market melt-up driven by robust earnings, AI enthusiasm and hopes for a short-lived energy shock faces a tougher test in the week ahead,” according to Laura Cooper, head of macro credit at Nuveen. “Hotter US inflation could push yields higher, while weaker retail sales may begin to reveal the impact of higher gas prices on consumers,” she added.

The oil market is in “a race against time” as the factors that combined to curb price rises from the Iran war stand to come under strain if the Strait of Hormuz stays closed into June, according to Morgan Stanley. Still, Bloomberg lists four "shock absorbers" that can help prevent crude reaching $200 per barrel.

Turning to the only driver for stocks, AI is increasingly “eating the global earnings cycle,” notes Bloomberg Intelligence analyst Izabella Wieckowska. A narrow group of AI-linked companies is doing much of the heavy lifting for global profit growth while large parts of the broader market struggle to keep pace. Meanwhile, BI’s scenario shows a 32% surge in 2026 AI-driven demand for electrical infrastructure to reach $117 billion by 2030, a compound annual growth rate of 18%. The narrowing trend within the stock market is likely to sustain moving forward, according to Citi strategists, who have upgraded US stocks to an overweight. The first-quarter earnings season shows an ongoing shift in corporate spending priorities to capex from buybacks, according to Goldman Sachs strategists.

Meanwhile, a multi-asset Pictet fund has sharply raised its equity exposure, shifting as much as 30% of its cash-equivalent holdings into AI heavyweights across Asia and the US. With the Kospi index surging to new highs on Monday, equity-derivatives strategists are increasingly recommending trades to bet on more gains in tech-heavy South Korea and Taiwan markets. Strategists at Societe Generale note the 12‑month variance spread between the Kospi 200 and S&P 500 has reached extreme levels.

In private credit, a recent wave of investor redemption requests across the $1.8 trillion market for private credit prompted Blackstone to enlist senior executives in putting up capital to bolster its flagship fund.

Taking a look at the waning earnings season, of the 446 S&P 500 companies to have reported so far, 83% have beaten analysts’ estimates, while 11% have missed. Barrick Mining and Constellation Energy are among companies expected to report results before the market open. Barrick Mining’s gold output could fall for the fifth straight quarter to 680,000 ounces, according to data compiled by Bloomberg. Bloomberg Intelligence projects this quarter will be its weakest gold production level in 2026, as the company resets its operating model. Simon Property and Him & Hers Health follow later in the day.

European stocks fall as an impasse in the Middle East conflict lifted oil prices and bond yields. The Stoxx 600 is down 0.2% to 611.12; Telecoms and banks outperform, consumer and retail sectors lag. Here are some of the biggest movers on Monday:

- Novo Nordisk shares gain as much as 5.5% to DKK306.15 after Citi analysts note the “impressive” Wegovy pill launch and increase their price target on the stock.

- Verisure gains as much as 3.6% after Bank of America upgraded its rating on the home-security firm to buy from neutral. BofA says the valuation “looks compelling” after recent share declines, praising the company’s premium subscription-based business model in structurally underpenetrated markets.

- Compass shares rise as much as 5.4% as the contract catering group delivers interim results described by analysts as “solid,” “sound” and “encouraging.”

- Genmab climbs as much as 2.7% after Jefferies analysts say share-price weakness after the 1Q results seems “overdone.”

- DiaSorin shares rise as much as 9.2%, the most in almost three years, after the health care company reported earnings ahead of expectations in the first quarter and reiterated its guidance for the full year. Analysts said the intact guidance is a positive surprise, with all eyes now turning to the upcoming capital markets day on May 20.

- Asos shares rise as much as 14% after the online clothing retailer agreed to sell its Lichfield fulfillment center to Marks & Spencer Group, which will lead to a significant one-off pretax profit. JPMorgan said the positive reaction is because investors were not anticipating material proceeds from the sale. It lifted its price target on the stock.

- Renault shares fall as much as 4% while Stellantis drops as much as 1.5% as Bank of America downgrades the carmakers due to competition from Chinese electric vehicles.

- European Defense shares fall on speculation that a weekend ceasefire in Ukraine, and reported remarks by Russian President Putin, could indicate that the war may be nearing its conclusion.

- Hannover Re shared drop as much as 3.4% as the German reinsurer reported a miss in P&C Re revenues despite strong April renewals.

- Victrex shares fall as much as 7% on the thermoplastic company’s first-half loss following an impairment against its manufacturing facility in China. The company’s full-year earnings guidance also fell short of consensus, according to analysts.

Earlier in the session, stocks in Asia rose, with South Korea leading a rally in tech shares as focus shifts back to artificial intelligence demand. The MSCI Asia Pacific Index gained 0.6%, with Korean memory chipmakers SK Hynix and Samsung among the biggest boosts. South Korea’s benchmark Kospi jumped 4.3% to a record. Investors are factoring in strong earnings for the region’s hardware makers on the AI buildout, with recent results from major tech firms indicating continued big spending. That’s helping propel continued gains in tech-heavy Asian markets, offsetting lingering concerns over the war in the Middle East. Stocks also gained Monday in Taiwan, mainland China and the Philippines, while equities fell in Australia and Indonesia. Shares also slipped in India, after Prime Minister Modi urged citizens to conserve fuel and curb costly oil imports.

In FX, the Bloomberg Dollar Spot Index traded 0.1% up on Monday; Bloomberg dollar gauge rose with Treasury yields as the US and Iran remain far apart on a framework to end the war, keeping oil prices elevated. The Canadian currency was among best performers in the Group of 10 against the greenback. EUR/USD traded down 0.1%. The European Central Bank will raise interest rates twice this year as the Iran war drives inflation higher, a Bloomberg survey showed. GBP/USD falls 0.2% to 1.3604. UK prime minister Keir Starmer said he would contest any leadership challenge, as he battled to save his premiership in a speech that appeared to do little to subdue the rebellions brewing within his party. US data Monday include April existing home sales

In rates, treasuries hold losses following gap lower at the Asia open and steady trading through London morning, leaving yields 3bp to 4bp cheaper across the curve. US 10-year near 4.39% is 3.7bp higher on the day with UK counterpart up about 6bp from Friday’s close; Treasury curve spreads are mostly flatter, 5s30s by 1bp. Oil prices are higher amid Middle East war impasse, and gilts underperform Treasuries and bunds with UK’s Starmer set to speak in a last-ditch effort to save his premiership. Treasury quarterly refunding auctions begin with 3-year note sale at 1pm New York time. Treasury’s $58 billion 3-year note auction precedes $42 billion 10-year and $25 billion 30-year new issues Tuesday and Wednesday. WI 3-year yield near 3.95% is 5.3bp cheaper than last month’s auction, which stopped through by 1.2bp, a strong result. IG dollar issuance slate includes four deals so far, and dealers anticipate a busy week totaling about $50 billion, much of it Monday ahead of CPI (Tuesday) and PPI (Wednesday) releases

Today's economic data slate includes April existing home sales at 10am. Fed speaker slate empty for the session.

Market Snapshot

- S&P 500 mini little changed

- Nasdaq 100 mini little changed

- Russell 2000 mini -0.1%

- Stoxx Europe 600 -0.2%

- DAX -0.2%

- CAC 40 -1%

- 10-year Treasury yield +3 basis points at 4.38%

- VIX +0.9 points at 18.12

- Bloomberg Dollar Index +0.1% at 1189.37

- euro -0.1% at $1.1771

- WTI crude +2.3% at $97.64/barrel

Top Overnight News

- The US and Iran wrangled over terms to end the war and reopen the Strait of Hormuz. Donald Trump called Tehran’s reply to his proposed peace plan “totally unacceptable.” BBG

- China confirms US President Trump's visit to China on May 13th-15th: Xinhua

- In an interview airing Sunday on 60 Minutes, Israel's Netanyahu says Iran war is "not over" until highly enriched uranium is removed. Benjamin Netanyahu told CBS he wants to end the US’s $3.8 billion a year in military aid to Israel over the next decade. CBS

- Trump will press Xi Jinping over China’s approach to Iran and hammer out details on a new board of trade when they meet later this week, senior US officials said. BBG

- China’s factory-gate inflation neared a four-year high in April, continuing a reversal from a long period of deflation as war in the Middle East keeps fueling higher energy costs. PPI (+2.8% vs. the Street +1.8% and up from +0.5% in Mar) and CPI (+1.2% vs. the Street +0.9% and up from +1% in Mar). WSJ

- US housing lenders and state agencies are raising concerns that the Trump administration could wind down a financing programme, The FY27 budget projects no new commitments for the programme: Semafor

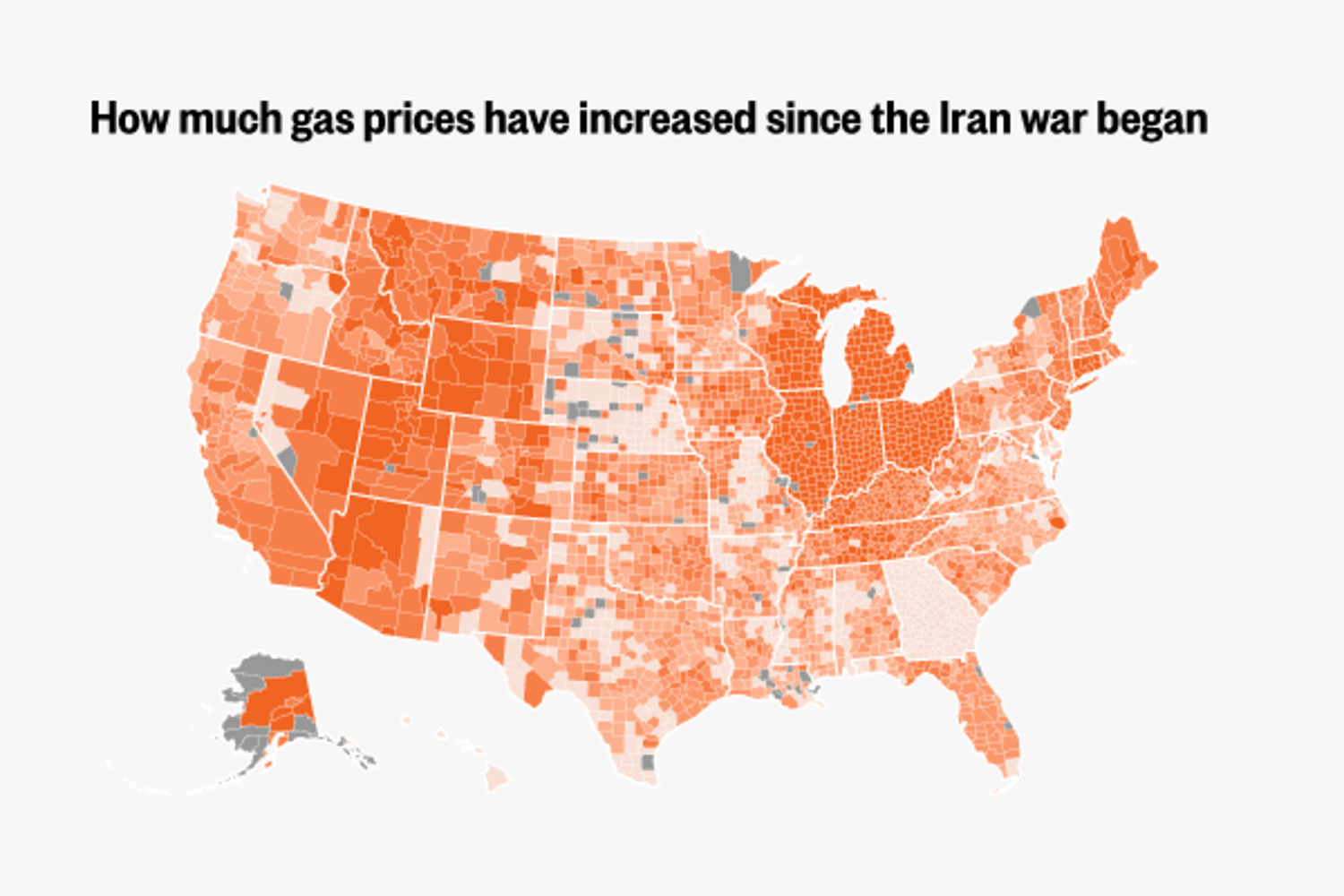

- US Energy Secretary Chris Wright told NBC that the White House is “open to all ideas,” when asked about suspending the federal gas tax. States in the Midwest have seen the steepest increases in gas prices, with a 72% jump in Ohio. BBG

- China's domestic car sales fell for a seventh straight month in April amid intense competition in the world's biggest auto market but exports stayed strong as automakers increasingly targeted overseas markets. Sales at home dropped 21.6% from a year earlier, but EV and plug-in hybrid vehicle exports shot up 111.8% from a year earlier, outpacing an 80.2% increase in overall car exports, as rising global fuel prices triggered by the U.S.-Israeli war on Iran bolstered EV demand in overseas markets. RTRS

- Prime Minister Narendra Modi has appealed to Indians to save fuel by working from home and using public transport, as the world’s third-largest oil importer tries to halt escalating economic disruption from higher energy prices. FT

- An American and a French passenger linked to the Hondius cruise ship outbreak have tested positive for the Andes strain of hantavirus, health authorities said. Seventeen US citizens are being repatriated from the vessel. BBG

- Goldman is pushing back the final two Fed rate cuts in our forecast by one quarter to December 2026 and March 2027. With energy cost passthrough likely to keep year-over-year core PCE inflation closer to 3% than 2% all year, we think that a combination of lower monthly inflation prints after the oil shock fades and further labor market softening will likely be needed for the FOMC to cut this year. The bank still expects that bar to be met but now expect it to take a bit longer.

Iran War

- US President Trump posted, “I have just read the response from Iran’s so-called “Representatives.” I don’t like it — TOTALLY UNACCEPTABLE!”

- Iran submitted its response to the latest proposal by the US to end the war, according to the Islamic Republic News Agency, while Tehran hasn’t provided any public indication yet on whether it will accept US President Trump’s proposal for Iran to permit passage through the Strait of Hormuz and for the US to end its blockade on Iranian ports in the next month. Iranian state media later reported that the US proposal amounted to Iran surrendering to Trump’s excessive demands, while Iran’s proposal stressed the need for the US to pay compensation for war damages and emphasised Iran’s sovereignty over the Strait of Hormuz.

- Iran reportedly was offering a shorter uranium enrichment suspension than the 20-year US proposal and rejected dismantling its nuclear facilities in any future talks with the US, according to WSJ.

- US lawmakers are considering a potential congressional authorisation for military action if the US-Iran ceasefire ends, according to Semafor.

- "Diplomacy and back channel talks and contacts between Iran and US to work out a draft agreement continues to be in the works -- Diplomacy is not dead", Journalist Mallick posted.

- US officials cited by Iran International said Iran's response to the US proposal has blocked the path to a diplomatic solution with Tehran; "The next steps by Trump after receiving Iran's negative response are still unclear".

- Iran’s Foreign Ministry spokesperson Baghaei said Iran’s proposal to the US “was not excessive,” and that the US continues to have “unreasonable demands.”. He further stated that "currently, we are focusing our discussions on ending the war and the uranium issue, which we will discuss later."

- Tehran reiterates "its main condition for the ceasefire is the cessation of conflicts on all fronts, from Gaza and Lebanon to Yemen", Mehr reported.

- Iranian source told Tasnim "We saw the reaction of the US president to the Iranian answer. It is of no importance. No one in Iran drafts proposals to please Trump. The negotiating team writes proposals only for the rights of the Iranian people...".

- Iranian media reported overnight that air defence systems in the southwest of the country shot down an enemy reconnaissance drone, Israeli N12 reported.

- Israeli PM Netanyahu said removal of Iranian nuclear material remains a war priority and that US President Trump told him 'I want to go in' regarding Iranian nuclear sites.

- Israeli PM Netanyahu is holding security consultations following Iran’s response to the US proposal.

- Two interceptors were launched from Kiryat Shmona area to southern Lebanon following the identification of a suspicious aerial target, according to N12.

- Hezbollah said it targeted Israeli force stationed inside a house in Baidar al-Faqaani in the town of Taybeh for the second time. Israeli media said officers in Northern Command reveal an increase in Hezbollah attacks without the public being informed about them.

- WSJ writes that as US President Trump prepares to meet with Chinese President Xi Jinping in Beijing this week, the ongoing US-Israel war against Iran and the closure of the Strait of Hormuz is expected to dominate discussions.

- UK and France will host a meeting on Tuesday with the presence of defence ministers of dozens of countries to discuss the situation in the Strait of Hormuz.

- Three tankers carrying 6mln barrels of oil exited the Strait of Hormuz, Sky News reported citing new data.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as the region reflected on last Friday's tech rally and NFP beat, as well as firmer-than-expected Chinese data, and geopolitical developments with US President Trump rejecting Iran's response to the peace proposal. ASX 200 was dragged lower by heavy losses in the health care sector as CSL shares slumped by around 19% after it flagged a USD 5bln impairment, while sentiment was also not helped by a report that Australia’s government is to scrap the 50% capital gains tax discount by July 2027. Nikkei 225 initially climbed to a fresh record high north of the 63,000 level but then wiped out its gains amid headwinds from higher oil prices and weak earnings outlooks for the likes of Nintendo and Honda. Hang Seng and Shanghai Comp were varied amid the mixed fortunes among the tech names in Hong Kong, and with the mainland boosted after Chinese trade and inflation data topped forecasts.

Top Asian News

- South Korea Finance Minister said economic growth is to exceed 2% this year.

European bourses (STOXX 600 -0.2%) trade mixed to start the week, despite the surge in energy prices. Over the weekend, US President Trump rejected Iran’s response to the peace plan and called it totally unacceptable. The FTSE 100 outperforms its peers while the CAC 40 lags. Sectors point to a mixed picture. Telecoms top the sector pile, followed by Banks amid the higher yield environment. Consumer Products & Services underperforms, with luxury names such as LVMH, Hermes and Kering falling by various degrees (0.8-2.5%).

Top European News

- UK PM Starmer said the local election results were "very tough" and reiterated he takes responsibility for election loss and will not step down. On the UK-EU relationship, he said Brexit has made the UK weaker and migration higher and vowed to rebuild the EU relationship.

- Talk of UK Cabinet resignations today. However, Mail on Sunday's Hodges expects such interventions to start later in the week, would be surprised to see any today.

- UK Manchester Mayor Burnham said to have identified a specific MP who is on board with a plan to stand down and let him run, POLITICO reported, citing sources.

- UK Labour Backbencher Catherine West told POLITICO she wants to “give a deadline” of Tuesday morning for the required 81 MPs to back her and force a leadership contest. West told POLITICO on Sunday that she still intends to watch Starmer this morning and make up her mind about whether to launch a leadership challenge. “If it’s an amazing speech, then I will think twice about asking the Parliamentary Labour Party for their support,” she told the Telegraph.

FX

- Snapshot: G10s are mostly lower against the USD, with action dictated by the strength seen across the energy complex; the CHF and JPY lag whilst the Loonie holds afloat. The NOK is a touch stronger this morning, following an uptick in the region’s core inflation.

- DXY is slightly firmer this morning, and trades towards the lower end of a 97.96-98.15 range. The index has been lifted by renewed geopolitical risk, after President Trump called Iran’s latest peace offer as “totally unacceptable” – as such, the crude complex is bid this morning. Domestically, tier 1 data is lacking this morning, but attention will turn to US CPI on Tuesday. Fed speak today includes Kashkari and Hammack (both dissenters at the April confab). ING opines that continued geopolitical unrest this week could see the index traverse back above the 98.00 mark, and trade within a 98.00-98.50 range.

- JPY and CHF are underperforming this morning, driven lower by their net-importer of energy statuses. For the USD/JPY specifically, it trades back towards the 157.00 mark, within a 156.55-157.17 range; further upside could see the pair head back towards its 100-DMA at 157.38. Domestic updates have been lacking for the JPY, but focus will be on US Treasury Secretary Bessent’s meeting with Japanese officials early this week.

- GBP is currently incrementally lower. PM Starmer remains on the wires at the time of publication; comments thus far remains very much as expected, where he reiterated that he will not step down. Markets await commentary from Catherine West, who has threatened a leadership challenge against Starmer, if she was left unsatisfied by his remarks. MUFG writes, “we continue to believe that a shift to the left for the Labour party would trigger at least a temporary period of pound selling”. Cable currently trades just above the 1.3600 mark, within a 1.3557-1.3614 range.

- Antipodeans are currently diverging, with the Aussie holding afloat against the Dollar, whilst the Kiwi moves a touch lower. Overnight, both were pressured by the downbeat risk tone, but the Aussie has managed to clamber higher thereafter. Some of the strength may be facilitated by the outperformance in the Yuan, after Chinese trade and inflation data topped forecasts.

Fixed Income

- Fixed benchmarks are generally on the backfoot as energy benchmarks opened higher and extended at the start of the week as the negotiating process made no progress on the weekend, with the US and Iran essentially rejecting each other's positions. We now await any revised proposal(s) before looking to the meeting between Chinese President Xi and US President Trump, from Wednesday.

- USTs hit a 110-15 low, with downside of just under 10 ticks, early doors. Since, as the energy space wanes from highs, fixed income has lifted off worst. USTs are now lower by around five ticks and to a 110-23 peak. If the upside continues, we look to resistance at 110-28 and 111-03+ from Thursday and Friday, respectively.

- Gilts underperform vs peer, as markets await a potential leadership challenge against PM Starmer. He remains on the wires at the time of publication, where his comments thus far have largely been as expected; he reiterated that he does not intend to step down. Markets will await updates from Catherine West, who could launch a leadership challenge against the PM if she is not satisfied by his remarks. Gilts are off by around 45 ticks, within a 87.10 to 87.45 range.

- Bunds in-fitting with USTs. Lower by 35 ticks to a 125.35 base early doors. Since, as energy eases, Bunds have trimmed much of the initial pressure and hold off a 125.56 peak, lower by c. 10 ticks.

Commodities

- Geopolitics continues to be the underlying driving force of price action. In short, Iran submitted its response to the latest US proposal to end the war, with Trump calling it “TOTALLY UNACCEPTABLE”. Iranian state media said the US proposal amounted to Tehran surrendering to Trump’s excessive demands. Iran’s counter-position stressed US compensation for war damages, recognition of Iranian sovereignty over the Strait of Hormuz, sanctions relief and release of blocked assets. In terms of diplomacy, Pakistani journalist Mallick posted, "To my understanding, Contrary to publicly put out positions and statements, diplomacy and back channel talks and contacts between Iran and US to work out a draft agreement continues to be in the works -- Diplomacy is not dead”.

- WTI and Brent futures are firmer but off best levels following the initial pop higher on the rejection, with the prospect of ongoing efforts to negotiate taking some sting out of the punchy rhetoric from the US and Iran. WTI Jun hit a high of USD 100.37/bbl (vs low 96.92/bbl) before waning levels under USD 97.70/bbl at the time of writing, though still +2% intraday. Brent July has dipped back under USD 104/bbl from an earlier USD 105.99/bbl peak. Dutch TTF also rose in early trade before waning from a high near EUR 45.50/MWh to a low just under EUR 44.50/MWh.

- Spot gold is modestly softer as the firmer crude prices keep the USD underpinned, though the bullion resides in a narrow USD 4,648.09-4,705.56/oz range at the time of writing, remaining under its 100 DMA (USD 4,781/oz). Spot silver, however, is choppy on either side of the USD 80/oz mark after briefly topping Friday’s USD 81.57/oz peak, with the 100 DMA at USD 80.60/oz.

- Base metals are mixed with sentiment cautiously positive in recent trade as energy prices came off best levels and provided a slight boost to the risk tone. 3M LME copper remains north of USD 13.5k/t in a USD 13,515.70-13,650.20/t range.

- Saudi crude oil supply to China is set to fall to a record low of about 10mln barrels in June, sources say.

- Japan's Industry Ministry said the first Central Asian crude tanker since Iran war has set sail for Japan.

Trade/Tariffs

- Indian official said Indian official said the US trade team will reach India soon for discussions; there is no plan to hike duties on gold and silver imports.

US Event Calendar

- 10:00 am: United States Apr Existing Home Sales, est. 4.05m, prior 3.98m

DB's Jim Reid concludes the overnight wrap

Good evening from Phoenix airport where I'm glad it’s a stopover to the West Coast and not the final destination as its seemingly 40 degrees plus out there! My Oura ring tells me I had 3hr 58 mins sleep on the plane. Hopefully a bit more will follow at the final destination before jet lag well and truly kicks in. I have 12 hours before I have to be presentable and coherent.

It has now been 73 days since the war in Iran began, with the past 32 marked by a stalemate characterised by a mix of truce and ongoing ceasefire. The absence of any meaningful kinetic activity for over a month suggests to me a firm US preference for reaching a deal. However, a counterpoint is that uncertainty over who holds negotiating authority in Iran may be complicating progress and delaying more difficult times ahead. It remains an unusual conflict with little action now for a month. In simple terms though, as long as the Strait of Hormuz stays closed, markets remain on a knife edge. Polymarket currently assigns a 50% probability to it fully reopening by 30 June.

The latest is that oil and yields are up again this morning as President Trump has posted that "I have just read the response from Iran's so called 'Representatives'" which he went on to call "TOTALLY UNACCEPTABLE". This was based on a WSJ report that suggested Iran was offering to transfer some of highly enriched uranium to another country but wouldn't dismantle its nuclear facilities. Iran's official news agency has disputed the report anyway. Brent is up +4.23% and 10yr US yields are up +3.5bps. However, US and European equity futures are largely flat and Asian equities are largely higher on the AI trade. The KOSPI is on fire again with the index up +4.0% as semiconductors surge again. The index has crossed +85% YTD.

This comes ahead of the planned mid-to end week meeting between US President Donald Trump and China’s President Xi Jinping in Beijing. It’ll be interesting to see whether this meeting does anything to shape negotiations in the war. Both leaders would clearly like to show their influence on the world stage. So certainly a big headline event.

Before that, the new week arrives with markets still processing last Friday’s US payrolls report, which came in broadly firm and reinforced the view that labour market conditions remain resilient. While not strong enough to decisively alter the policy outlook, the release did little to ease concerns that underlying inflation pressures could persist, especially given still-solid wage dynamics. Against this backdrop, outside of the Iran War developments which will of course take centre stage, the coming week will remain centred on the US, with a dense run of data and policy developments.

The focal point will be tomorrow’s April CPI report. Our economists expect headline inflation to rise by +0.58% month-on-month, moderating from March’s +0.9%, but still relatively firm. In contrast, the core measure is projected to accelerate to +0.39% MoM from +0.2%, suggesting underlying price pressures remain sticky even as energy-related effects fade. The YoY rates would move from 3.3% to 3.8% for the former and from 2.6% to 2.8% for the latter. See Matt Luzzetti's piece here on five doubts around the US disinflation story and his team's CPI preview piece here.

Producer price data follows on Wednesday and then the remainder of the week shifts towards activity indicators. Our economists expect retail sales to decline by -0.3% MoM after March’s strong +1.7% increase, pointing to some payback in consumer spending. Meanwhile, industrial production is forecast to rise modestly by +0.2% MoM following a -0.5% drop previously, suggesting a tentative stabilisation in manufacturing output.

Policy and politics will also be important. A Senate vote on Kevin Warsh’s nomination as Fed Chair is scheduled for today, just days before Jerome Powell’s term is set to expire at the end of the week. It's possible the vote could get pushed back a day or so due to other Senate business but by the end of the week you would expect Warsh to have taken Miran's seat on the board with Powell staying on the committee.

In Europe, inflation readings from Denmark and Norway today are followed with Germany’s ZEW survey tomorrow with sentiment darkening even with the nation's extraordinary fiscal package. Later in the week, the ECB’s economic bulletin may offer additional context on the central bank’s assessment of inflation and activity trends.

In the UK, attention will be split between politics and macro. The State Opening of Parliament and the King’s Speech on Wednesday will outline the government’s legislative agenda for the year ahead. With PM Starmer under tremendous pressure following the very poor (but broadly as expected) local election results on Thursday there is talk of a leadership challenge as soon as today. Backbench MP Catherine West has said she will stand, which would be a stalking horse nomination. However, many left-wing MPs (as she is) have urged her not to as their preferred candidate Andy Burnham is not currently an MP. They fear an election now might be a bit too early and may allow a more moderate candidate like Wes Streeting to prevail. So timing tactics could prolong Starmer’s reign. A reminder that in September last year, Mr Burnham said that the UK should no longer be “in hock to the bond markets”. This caused a spike in Gilt yields and although he subsequently downplayed the remarks, this is something to watch carefully as we navigate the politics of the next few days and weeks. On the data side, Q1 UK GDP on Thursday will offer up the latest state of play growth wise.

In Asia, Japan’s schedule includes household spending data tomorrow, alongside the Economy Watchers survey and bank lending figures on Wednesday. In addition, the Bank of Japan will publish its summary of opinions from the April meeting, which should provide greater insight into policymakers’ thinking and any emerging shifts in the policy stance.

There are multiple appearances from Fed, ECB, BoE and BoJ officials throughout the week, and on the corporate front, earnings continue at a steadier pace. In the US, Cisco and Applied Materials are among the key names, while internationally the focus includes major firms such as Tencent, Alibaba, Siemens and Bayer. See the day-by-day calendar at the end as usual for a fuller week ahead preview.

In terms of data in Asia, China's trade data released on Saturday showed exports surging +14.1% YoY (+8.4% expected) with imports up +25.3% (+20.0% expected). Inflation released this morning showed CPI climbing +1.2% YoY (+0.9% expected), the same number for core, with PPI up +2.8% (+1.8% expected). Commodity prices seem to have pushed inflation higher than expected.

Recapping last week now, markets advanced amidst hopes that the US and Iran would come to an agreement to end the war. The gains came despite both sides trading attacks on Thursday and Friday, as Trump reiterated that a ceasefire between the two sides remained intact. The initial catalyst of the market optimism occurred on Tuesday, when an Axios report announced that the US and Iran were close to agreeing on a framework that would end the war and ahead of more detailed nuclear negotiations. So that triggered a fall in oil prices, with Brent crude down (-6.43%) over the week (+1.16% on Friday) to $101.22/bbl, though 6-month Brent futures were stable (-0.11%) at $87.30/bbl after a +2.19% rally on Friday.

US equities surged to new highs, with the S&P 500 (+2.34%, +0.85% on Friday) posting a sixth consecutive weekly advance, whilst the Nasdaq (+4.30%, +1.51% on Friday), Mag-7 (+3.87%, +0.81% on Friday) and Philadelphia Semiconductor Stock Exchange (+10.57%, +4.97% on Friday) rose to new highs as well. In addition to the slide in oil, the rally was also driven by strong earnings in AI and solid US data. The highlight on the latter was the April jobs report on Friday, which showed payrolls rising by +115k (+65k expected), though this was combined with slightly slower average earnings growth (+3.6% yoy vs +3.8% exp). We did see some less positive survey data, including U Mich consumer confidence data for May (48.2 vs 49.5 est) on Friday and the NY Fed’s latest 1yr inflation expectations (3.64% vs 3.5% exp). Put together, this left Treasuries little changed over the week, with 10yr yields down -0.9bps to 4.36% (-2.5bps Friday), while 2yr yields were up +1.0bps to 3.89% (-2.2bps Friday).

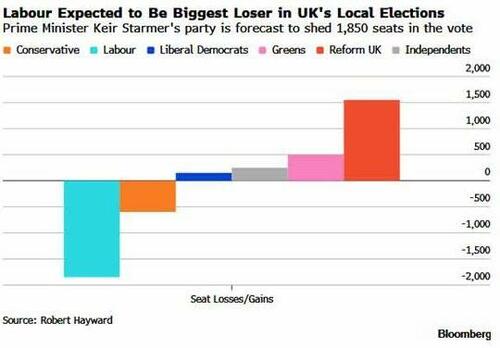

In Europe, a key story were the UK local elections, which showed the governing Labour Party suffering heavy losses, whilst Nigel Farage’s Reform UK party saw major gains. However, these results were largely expected and 10yr gilt yields outperformed on Friday (-3.6bps) and were down -5.2bps over the week.

Elsewhere in Europe, yields on 10yr bunds (-3.1ps, +0.3bps Friday), OATs (-7.1bps, -0.4bps Friday) and BTPs (-13.1bps, -1.2bps Friday) also declined amid lower oil prices. European equities mostly advanced, although their gains were pared back amidst the ongoing Iran uncertainty going into the weekend, with the STOXX 600 (+0.10%, -0.69% Friday) and DAX (+0.19%, -1.32% on Friday) marginally higher, though the FTSE 100 (-1.26%, -0.43% Friday) lost ground.

.png?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

{kind=link}