By Michael Every of Rabobank

Summit... then 'summit' worse?

“TOTALLY UNACCEPTABLE,” was President Trump’s response to Iran’s belated reply to his peace proposal, which they have rejected as a “surrender.” Tehran thinks the US must do so instead: rather than handing over enriched uranium, pledging to never build a nuke, reopening the Strait of Hormuz, and dropping ballistic missiles and support for regional terror proxies, Iran wants a permanent US retreat, reparations paid to it, and control of Hormuz.

More war, where the US takes control of the Strait and/or bombs the regime harder to encourage it to sign a deal, seems inevitable if one rules out a 1956-style retreat. Indeed, Israeli PM Netanyahu gave a TV interview to 60 Minutes where he stated the Iran war, while having achieved a lot, is “not over.” Markets are not going to enjoy the prospect of greater and longer disruption to global energy supplies.

However, new fighting may not be seen until the weekend. First, “because markets.” Second, as the US still doesn’t have everything in place it needs militarily to strike harder and for longer. Third, because over May 13-15, Trump will meet Xi in Beijing, where the focus will be on Iran as well as broader US-China relations.

As postulated since the early days of this war, its resolution may run through Beijing. China, like Russia, has influence on Iran via supplies of key military goods. In that regard, some see Trump going to China with Xi holding all the cards (because Iran holds a Strait.) Yet others think a sustained war that pushes global energy markets and the economy past a terrible tipping point might see Beijing offer to lean on Iran rather than supporting it like Russia vs Ukraine.

Naturally, that opens up chatter of a potential ‘Grand Bargain’ around the core interests of China, the US, and Russia (where President Putin presided over a deflated Victory Day parade and said the war with Ukraine may “be coming to an end.”) If you aren’t at this week’s table, you might be on it. In short, the focus should be on this summit and whether it leads to ‘summit’ better or worse for you.

Equally naturally, political dramas around the world mirror those in geopolitics.

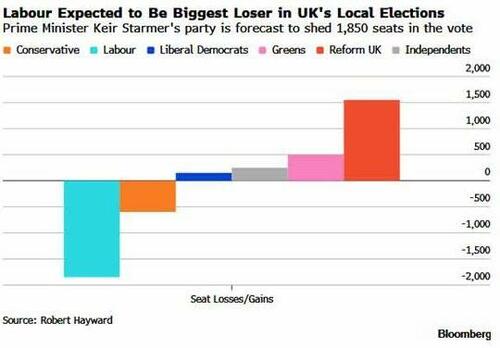

Following a local election drubbing and the collapse of two-party politics, the ruling UK Labour Party will see a stalking-horse leadership contest against deeply unpopular PM Starmer. His potential rivals Streeting (in the cabinet), Miliband (in the cabinet and a former unpopular Labour leader himself), Rayner (not in the cabinet due to a tax scandal), and Burns (not in Parliament due to Starmer’s team) must decide if they will make their moves. Starmer is determined to cling on and will give a major speech today seen as determinative for who joins the fray. Financial markets will be worried about populist left policy direction under new leadership, where Labour is losing voters just as fast at it is to the populist right.

In Australia, the by-election in Farrer saw a seat formerly held by the Liberal Party leader taken by the populist right One Nation and the door opened to it joining the Liberal-National opposition coalition, reshaping Australian politics. This is ahead of a Labor Party budget tomorrow already seeing a populist left shift via cash handouts (when inflation is nearly 5%), and taxation of residential property and other assets.

Denmark’s Liberal leader has taken over coalition talks after the Social Democrat premier failed to secure a parliamentary majority. There appear few stable political combos on offer, and questions swirl as to whether the inclusion of the far right will be necessary to achieve one.

Germany’s far right AfD is at 28% in national polls, the most popular party, and 41% in an eastern state where an election will be held in September: add the far left, and populism is >50% of the electorate. There appear few stable German political coalitions that exclude the AfD.

In all these cases, as in the US, the market-friendly center is failing to hold and extremes on the left and right, and via sectarianism, are benefitting most.

Meanwhile, a revolution may be taking place in the geoeconomic sphere. The CLARITY Act working its way through the US Congress as companion to the GENIUS Act that cements stablecoins into the financial system has disallowed USD stablecoins from paying interest; however, it allows the payment of scaled rewards and fees that are their functional equivalent when used in transactions. That might prove pivotal for these much-misunderstood new assets designed to steamroller the global Eurodollar financial architecture.

China is officially banning anything other than its official e-CNY, a CBDC, though Hong Kong is floated as a potential location that could perhaps issue Chinese versions of onshore mainland debt-backed stablecoins similar to those of the US. That could, in theory, propose an alternative payments infrastructure that isn’t hampered by China’s capital controls.

By contrast, the ECB has just stated stablecoins are not an efficient way to strengthen the international role of the euro vs. deeper capital market integration and a stronger safe asset base. That means its alternative to the USD is an EUR that looks more like it, which implies the matching ‘benefits’ of trade deficits, debt, and financialisation over net exports and the industrial production needed for remilitarisation – as the US tries to pivot hard the other way.

Indeed, the US is not only pushing for a $500bn increase in the Pentagon budget but seeing a shake-up of how it operates: bureaucrats will no longer negotiate defence contracts, with an elite private sector “Deal Team Six” to handle and approve negotiations; defence firms will have to build their own factories; those that fail to deliver goods will be held responsible and may be replaced with new contractors; and there will be no more ‘costs-plus’ overspending. “Despite paying companies to make weapons faster, scheduled delays were constant, and cost overruns were the norm, all while their CEOs got rich,” according to Secretary of War Hegseth.

“Because markets,” said shareholders. But perhaps no more. That’s summit else to chew on.

.png?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)