US equity futures are higher led by tech as the selloff in bonds eased and traders awaited earnings from Nvidia after the close. As of 7:30am ET, S&P futures are up 0.3% while Nasdaq futs rose 0.7% showing optimism heading into the release and overlooking weakness in tech during APAC trade. In premarket trading, NVDA is up 1.8% in premarket trading, as semis see a strong bid with Mag7 names almost all higher. Cyclicals ex-Energy are rallying led by Industrials with Defensives lagging and Staples down. European stocks have edged higher alongside a pullback in energy prices, which saw Brent briefly slip onto a $108/bbl handle. Today is all about NVDA but Fed Minutes this afternoon may provide color on the dissenters from the previous Fed Day. Bond yields in the US and Europe retreated from multiyear highs as traders pared back aggressive bets on interest-rate hikes this year. US yields are 1-3bp lower across the curve, the 10Y dropping to 4.64% from yesterday's high of 4.69%, as the USD sees a mild bid. Brent fell 1.8% toward $109 a barrel with the broader energy complex drops as JPM flags 6.6mm bbls of oil crossing the SoH over the last 24 hours; Precious Metals are also bid with Ags seeing weakness. Tomorrow’s macro releases include Flash PMIs and jobless data.

In premarket trading, Nvidia is outperforming fellow Magnificent Seven stocks, rising 1.8%, ahead of its much-anticipated first-quarter results report after the market closes. Fellow chip stocks are also gaining (Tesla +1%, Alphabet +0.3%, Amazon +0.2%, Meta Platforms +0.2%, Apple -0.2%, Microsoft -0.4%)

- 8x8 (EGHT) jumps 17% after the software company reported fourth-quarter results that beat expectations.

- Cava Group Inc. (CAVA) is up 7.1%. The company raised its annual sales outlook after diners flocked to its restaurants in the first quarter, defying the crunch in consumer budgets that has weighed on the industry.

- Keysight Technologies (KEYS) is up 2.3% after the measurement instruments company reported second-quarter results that beat expectations and gave a third-quarter forecast that is above the analyst consensus.

- Toll Brothers (TOL) rises 2.3% after the luxury homebuilder reported second-quarter profit that beat analysts’ estimates and raised its full-year guidance.

In other corporate news, Goldman Sachs is said to have the leading role on the cover of SpaceX’s IPO, with Morgan Stanley also listed as a lead bank. SpaceX expects to proceed with its acquisition of Cursor 30 days after the company begins trading publicly, and if the deal doesn’t go through, SpaceX would pay Cursor a $10 billion breakup fee in cash, BBG reported. Early AI tools are boosting productivity as much as 30%, said JPMorgan, while Standard Chartered’s CEO has sought to reassure staff after a backlash to his remarks on using artificial intelligence to replace “lower-value human capital.” Softbank’s $60 billion bet on OpenAI, and growing unease over Masayoshi Son’s devotion to Sam Altman is today’s The Big Take.

Futures are higher in early trading as investors digest a backdrop of surging rates volatility, heavily crowded semis exposure and euphoric - and outright manic bubble in the case of Korea - positioning, while some of the most aggressive AI momentum trades globally show signs of strain, even as stocks broadly ignore the historic rout taking place in the bond market, sending 30Y yields to 19 year highs.

A potential strike at Samsung and the words of Jensen Huang are two catalysts in the next 24 hours to keep traders on edge.

The impending strike at Samsung could add to concerns around supply being able to meet burgeoning demand for AI memory chips in the face of already surging memory prices, at a time inflation is coming for the overcrowded AI trade.

Nvidia will give a much-anticipated update on the state of the AI economy when it reports after the close. While sales are estimated to have grown 80%, investors will be more focused on what Nvidia has to say about ramping up production and fending off competitors.

Options traders are pricing an implied move of about 5.5% for Nvidia shares in either direction following the results. With the report coming at a time when the roaring rally in chipmakers is coming off the boil, well-received earnings could give the sector fresh momentum and help drive global indexes even higher into superbubble territory.

“The semiconductor rally has stalled, but really is just in a holding pattern until Nvidia reports,” said Joachim Klement, head of strategy at Panmure Liberum. “Nvidia can, for now, keep its beat-and-raise machine going, which will reignite the rally in semiconductors.”

Today we also get the minutes of the April 28–29 FOMC meeting which should show that support for removing the easing bias from the statement extended beyond the three dissenters. The minutes should reinforce the market view that the easing cycle is on an extended hold, according to Bloomberg Economics. Fed’s Paulson said she favored holding interest rates steady and conditioned lower borrowing costs on making sustained progress on inflation.

President Donald Trump threatened to resume strikes on Iran in the coming days as part of the push for a deal to end the war, after he said he had just called off a US attack. Alexandre Drabowicz, chief investment officer at Indosuez Wealth Management, said he wouldn’t be surprised if Trump’s next steps take into account where interest rates are headed, given the current yield levels. “We’re in the thick of the danger zone,” he said.

“Stagflation risk has gone up significantly,” said Justin Onuekwusi, chief investment officer at St. James’s Place. “When we’re talking about increased inflation and falling growth, in that environment, most asset classes will struggle, including bonds.”

In politics, the Republican-led US Senate signaled mounting opposition to continuing the Iran war in a procedural vote Tuesday, reflecting deepening political unease over a conflict that is taking a financial toll on Americans. Trump signed an executive order directing regulators to issue guidance on banking services to undocumented migrants, in a move that could tighten access to the financial system.

Retail is in focus before the market opens, with Target and TJX set to report. Visits to Target stores during the first quarter were up 5.1% from the year prior, marking the chain’s first positive visit growth in more than a year, according to data from Placer.ai. The firm also notes traffic in April rose 5.5% from the previous year.

European stocks edge higher alongside a pullback in energy prices, which saw Brent briefly slip onto a $108/bbl handle. Stock market operator Euronext is among the biggest gainers, while credit checking firm Experian fell on its latest earnings. Here are the biggest movers Wednesday:

- Euronext shares gain 7.1%, most since July 2023, after the stock market operator reported what analysts say are strong 1Q earnings, driven by better revenues and costs, with the equity markets division as the main standout

- CSG shares rise as much as 12%, the most since January, after the defense company reported results analysts called strong, saying the market should be relieved after the recent selloff

- Marks & Spencer shares rise as much as 5.5% after the retailer reported a milder drop in adjusted pretax profit than anticipated during FY26, having grappled with a costly cyberattack during the year

- RS Group shares rise as much as 10%, the most since November 2024, after the distributor of electrical and industrial products announced a £100m share buyback and pointed to improving momentum across its major markets

- Playtech shares gain as much as 5.1% after the gaming software maker said it delivered an “excellent trading performance” over the first four months of the year, according to a statement ahead of its annual general meeting

- Ypsomed shares jump as much as 14%, the most since April 2025, after the Swiss maker of injection systems reported better-than-expected financial results and provided guidance that pleased investors

- Severn Trent shares rise as much as 4.9% after the UK water company reported earnings ahead of expectations in FY26 and upgraded its outlook for FY28; peer United Utilities is up 1.3%%, while smaller rival Pennon is trading 1% higher

- Experian shares drop for the first day in five, falling as much as 6%, as the credit checking company’s full-year guidance proves slightly lower than analysts expected

- Orkla falls as much as 8.9% after the Norwegian consumer goods group reported earnings which fell short of expectations. DNB Carnegie sees a “mixed” report, flagging an adjusted Ebit miss and increased margin pressure

- Rusta falls as much as 8.6%, the most since September, after SEB cut its recommendation on the Swedish retailer to hold from buy, saying the stock’s valuation discount has disappeared after a strong rally

- B&M falls as much as 3.9% as Goodbody cut its rating on the European budget retailer to hold from buy. The broker sees tepid earnings as the UK macroeconomic climate deteriorates and poor weather weighs on sales

Earlier in the session, Asian equities fell for a fourth straight session, heading for their longest losing streak in nearly two months as chip stocks dropped and bonds sold off on inflation concerns. The MSCI Asia Pacific Index declined as much as 1.3%, with Samsung and TSMC among the the biggest drags. Samsung shares slumped after its labor union said it will go on strike Thursday, a development that pushed the Korean benchmark Kospi lower. Most markets in the region were down, led by Kospi’s 3% decline. Concerns that the US-Iran war may stretch on have lifted global inflation expectations, pushing yields higher. The higher cost of capital may hinder the fast expansion of Asian stocks that have ridden artificial intelligence tailwinds to grow earnings. Stocks also fell in Japan, China, Hong Kong and Australia.

In FX, the greenback has given back some ground after dollar gains pushed EUR/USD to its lowest level since April 7. JPY remains rangebound amid the threat of intervention, with Yen fundamentals still bearish (Supplementary Budget/Energy). Demand at the overnight JGB auction was weak and saw some pressure in JGBs but no real follow-through to the FX space. USD/JPY is unchanged and testing 159.00 to the downside at the time of writing. GBP is a little weaker after soft April inflation data trimmed bets on BoE hikes. GBP/USD moved lower by c. 15pips post-data, now above pre-release levels as it attempts to regain a 1.34 handle. EUR/GBP moved higher by 10pips post-data, a move which swiftly pared amid resistance at 0.8670 and recent energy-related moves. (See 08:40 BST headline for more). EUR is also a touch weaker and seemingly moving lower in tandem with USD strength. EUR/USD -0.1%, the pair delved as low as 1.1583 before attempting to return back to a 1.16 handle, where it has traded throughout the week so far.

US Treasuries yields continue to test levels reminiscent of unnerving times. A sustained selloff in Asia and Europe on Tuesday continued through the US morning until a small relief bid emerged in the afternoon. Still, 30y yield ended the day hovering around 5.17% – the highest level since 2007. 10y yields have pushed past the 4.50% mark that has typically served as a reentry point from oversold territory and are inching closer to 4.75%. Global inflationary concerns, a Middle East crisis and a lack of conviction has led to a perfect storm of stop outs and compounding bearish momentum. The lack of thematic dip buying is likely summed up by sentiment that things look cheap but could look even cheaper. 2s5s10s – something the desk highlighted a few sessions ago – has dramatically cheapened 10bp over the past few days. Wednesday's 20y auction will be a key gauge on the market’s appetite for long-end duration at these levels. The elevated rate environment is bad news for risk assets in a world where debt-fueled capex is high, and this US administration has used tools to indirectly affect dip buying in duration before

This morning treasuries hold gains amid a bigger curve-steepening rally in gilts after UK inflation gauge slowed more than economists estimated. US yields are 2bp-3bp lower on the day, with 5s30s curve steeper by more than 1bp; 10-year is down 2.7bp near session low 4.64%, with UK 10-year lower by more than 8bp, Germany’s by more than 3bp. UK front-end yields remain around 10bp richer on the day heading into the US session, which includes a 20-year bond auction poised to draw the highest yield since October 2023. July WTI crude oil futures, down around 2.5%, also support Treasuries. UK yields are 7bp to 10bp lower on the day with 2s10s and 5s30s curves steeper by about 1.5bp; following the UK inflation data, swaps-implied chance of a BOE rate hike in June ebbed to less than 20%, compared with about 50% at one point last week

Treasury auctions resume with $16 billion 20-year new issue at 1pm New York time. WI 20-year yield near 5.17% is ~29bp cheaper than last month’s auction; a $19 billion 10-year TIPS reopening is ahead Thursday. IG dollar issuance slate includes a couple of offerings. Twelve borrowers raised almost $15 billion on Tuesday with issuers paying, on average, 4.8bp in new issue concessions on deals that were 3.9 times covered

Economic data slate empty for the session. Fed speaker slate includes Barr (9:15am), and minutes of FOMC’s April 28-29 meeting are slated for 2pm release

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.5%

- Russell 2000 mini +0.2%

- Stoxx Europe 600 +0.2%

- DAX +0.2%

- CAC 40 +0.3%

- 10-year Treasury yield -3 basis points at 4.64%

- VIX little changed at 18.03

- Bloomberg Dollar Index little changed at 1204.72

- euro -0.1% at $1.1591

- WTI crude -1.5% at $102.59/barrel

Top overnight news

US President Trump signed a fintech Executive Order to protect the US financial system from illicit activity, while it was reported that the White House plans to release an Executive Order on cybersecurity and AI safety as soon as this week, which seeks early government access to advanced models.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks declined following the weak handover from the US, with sentiment dampened amid headwinds from a higher yield environment and the uncertain geopolitical backdrop. ASX 200 retreated with the declines led by underperformance in the mining and materials sectors, while a lack of data and firmer yields contributed to the uninspired mood. Nikkei 225 fell beneath the 60,000 level with notable pressure in machine tool and electrical equipment manufacturers, while recent comments from Japan's Finance Minister, and current FX levels were seen to stoke intervention risks. Hang Seng and Shanghai Comp conformed to the downbeat sentiment amid bond and inflation woes, with the declines in Hong Kong led by mining, solar and property stocks, while there was a lack of surprises from the PBoC announcement to maintain the benchmark Loan Prime Rates for the 12th consecutive month.

Top Asian News

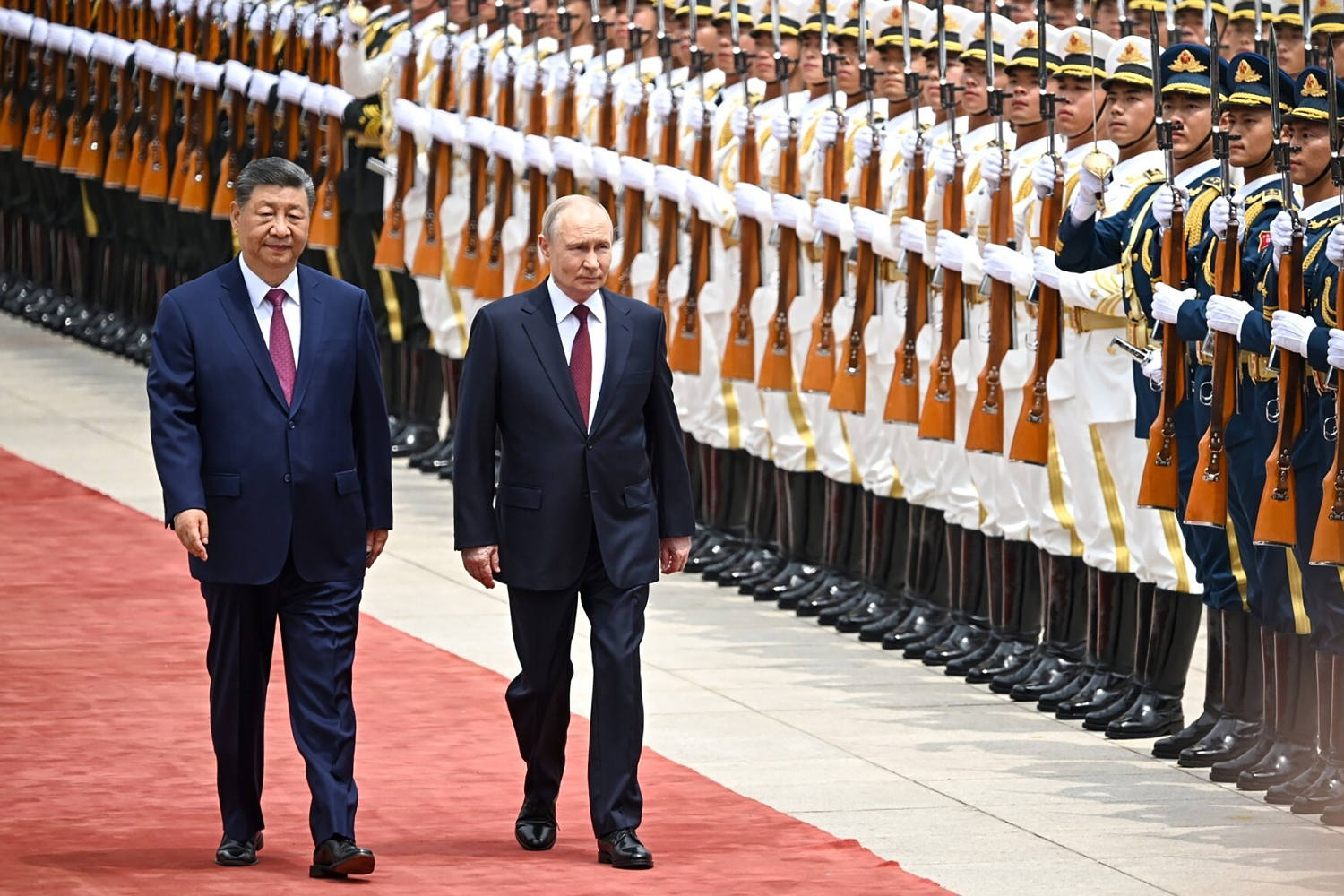

- Chinese President Xi met Russian President Putin in Beijing and said that relations have reached their current level due to deepened political mutual trust and strategic cooperation, while Putin said ties between Russia and China support broader international stability. Furthermore, China and Russia plan to deepen continuous strategic coordination, and Putin invited Chinese President Xi Jinping to travel to Russia next year, while Xi told Putin that the world faces the risk of regressing into a “law of the jungle.”

- Japanese PM Takaichi said she is not currently at a stage where she can comment on the possible size of the extra budget. She further said that plans to protect people’s lives and businesses while curbing issuance of deficit-financing bonds as much as possible.

European bourses (STOXX 600 +0.2%) were initially incrementally lower, but now display a more positive picture. On the trade front, the EU finalised the text of its US trade deal, in which the bloc would remove levies on US industrial goods in exchange for a 15% tariff ceiling on EU exports. Next steps are for the Parliament and EU countries to vote to ratify the text. The AEX (+0.4%) hovers around the U/C mark, with chip majors ASML (+3.2%) and BESI (+2.3%) supporting the index, while the FTSE 100 (-0.1%) sees little support following the cooler-than-expected UK inflation print. European sectors trade mixed. Basic Resources tops the sector pile as it manages to claw back some of Tuesday’s losses. Energy and Technology round out the top three sectors. To the downside, Media, Retail and Food, Beverages & Tobacco underperforms. UK supermarkets (Tesco -1.6%, Sainsburys -1.4%) have came under pressure after reports by the FT stated that the UK Treasury is pushing large supermarkets to introduce voluntary price caps on key groceries in return for lifting some regulations.

Top European News

- UK Inflation Rate MoM (Apr) M/M 0.7% vs. Exp. 0.9% (Prev. 0.7%, Low. 0.8%, High. 1.3%).

- UK Inflation Rate YoY (Apr) Y/Y 2.8% vs. Exp. 3% (Prev. 3.3%, Low. 2.8%, High. 3.4%); Services 3.2% (prev. 4.5%). ONS: "There was a notable fall in annual inflation led by lower electricity and gas prices. This was due to the government’s energy bill support package reducing variable and fixed tariffs, along with lower global wholesale energy prices before the conflict in the Middle East, which fed through to the reduction in the Ofgem cap."

- UK Core Inflation Rate MoM (Apr) M/M 0.7% (Prev. 0.4%).

- UK Core Inflation Rate YoY (Apr) Y/Y 2.5% vs. Exp. 2.6% (Prev. 3.1%, Low. 2.5%, High. 3.2%).

FX

- USD continues driving higher amid the continued unconstructive oil/yield environment with oil either side of USD 110/bbl and yields still elevated, albeit lower on the day. US/Iran news overnight was light, and nothing pertinent this morning, but the running commentary remains hostile. The Buck will remain attentive to Gulf developments, alongside expected hawkish FOMC minutes this evening, and NVIDIA earnings after the US close. DXY +0.1%, is now above all significant DMAs, with the 50DMA closest at 99.00.

- JPY remains rangebound amid the threat of intervention, with Yen fundamentals still bearish (Supplementary Budget/Energy). Demand at the overnight JGB auction was weak and saw some pressure in JGBs but no real follow-through to the FX space. USD/JPY is unchanged and testing 159.00 to the downside at the time of writing.

- GBP is a little weaker after soft April inflation data trimmed bets on BoE hikes. GBP/USD moved lower by c. 15pips post-data, now above pre-release levels as it attempts to regain a 1.34 handle. EUR/GBP moved higher by 10pips post-data, a move which swiftly pared amid resistance at 0.8670 and recent energy-related moves. (See 08:40 BST headline for more). EUR is also a touch weaker and seemingly moving lower in tandem with USD strength. EUR/USD -0.1%, the pair delved as low as 1.1583 before attempting to return back to a 1.16 handle, where it has traded throughout the week so far.

Central Banks

- Fed's Paulson (2026 voter) said inflation remains too high and interest rate cuts may only happen after inflation is controlled, while he also commented that current policy is appropriate and it is healthy for markets to consider an extended hold or hikes. Paulson stated the US labour market is stable and consumption is slowing, but is resilient, and a rate hike may be considered if growth moves above potential or other inflation risks emerge. Furthermore, he reiterated that he did not see a need to change language at the last policy meeting, as well as noted that risks are 'super-elevated' right now to both inflation and the outlook.

- ECB's Wunsch said the bond selloff is not impacting the ECB's thinking of Iran and that the ECB will need to react at some point.

- JPMorgan expects the BoE to hike 25bps in July (prev. forecast of hike in June).

Fixed Income

- Global fixed benchmarks are firmer this morning, attempting to rebound from recent losses as energy prices pull back this morning. UK benchmarks outperform thanks to a cooler-than-expected regional inflation report, which has reduced the chance of a hike in June.

- USTs are firmer by a handful of ticks and trades towards the upper end of a 108-19+ to 108-30+ range. Focus remains on the geopolitical environment, with a recent WSJ report suggesting that Iran's position in talks with the US to end the war hasn't changed much from earlier iterations that failed to yield progress towards a deal. Earlier today, the IRGC provided some punchy rhetoric after it stated that the war would extend “beyond the region” if Iran is attacked again. Ultimately, an environment which keeps energy-related inflation woes at the front of minds, allowing yields to remain at elevated levels. On that front, the US10yr is just off recent highs, residing at 4.65%; the US-30yr (5.17%) remains towards peaks, after it surged to levels not seen since 2007, in the prior session. Ahead, FOMC Minutes and a 20yr auction.

- Bunds are firmer by around 10 ticks, and hold within a 123.86 to 124.22 range. Earlier, German PPI M/M printed a touch above the expected (1.2% vs exp. 1%); the statistics office notes that it “is primarily due to higher prices for intermediate goods”, particularly in precious metals prices. The report also highlighted the continued surge in energy prices. There was little move in German paper following this report. On the central banking front, ECB’s Wunsch said that the bond sell-off is not impacting the ECB’s thinking of Iran, adding that the Bank will need to act at some point. Elsewhere, French President Macron nominated Emmanuel Moulin to head the Bank of France. He said at the Senate today that the ECB must be ready to act to combat inflation, and stressed the importance of an independent central bank. He now appears at the National Assembly, where the outcome of the votes for his nomination will be announced this afternoon.

- Gilts outperform vs peers, and are currently higher by around 45 ticks; UK paper holds at the upper end of an 86.07 to 86.54 range. From a yield perspective, unsurprisingly the UK curve is bull steepening; the 10yr is now eyeing the 5% mark to the downside, but will likely need some positive geopolitical updates for a decisive breach below the key level. Price action today follows a cooler than expected inflation report, where headline CPI slowed to 2.8% in April, from 3.3% in March and below consensus of 3.0%. This report spurred a dovish repricing at the BoE, with markets now assigning an 8% chance of a hike in June (vs 35% pre-release); July now 50% (vs 84% pre-release).

- Germany sells EUR 3.845 vs exp. EUR 5bln 2.90% 2036 Bund: b/c 1.5x (prev. 1.24x), average yield 3.16% (prev. 2.92%), retention 23.1% (prev. 23.66%).

- Japan sells JPY 525.8bln 20-year JGBs; b/c 4.01x (prev. 4.82), average yield 3.711% (prev. 3.327%).

Commodities

- WTI and Brent July futures have been edging lower throughout the European morning thus far, with newsflow relatively mixed. Out of Iran, one official noted that the region is open to negotiations whilst an IRGC member stated that the war will extend beyond the region, if Iran is hit again. Most recently, Saudi press citing a diplomatic source suggested that Iran-Pakistan cooperation had declined/stopped over the past two weeks.

- Nonetheless, crude futures remain heavy, with WTI in a USD 102.50-104.45/bbl range while its Brent counterpart resides in a USD 109.52-111.49/bbl range at the time of writing, with some weakness seen in the European morning despite a lack of clear catalysts, although the moves did follow comments from the Iranian Deputy to the President. Dutch TTF is flat in choppy trade above the EUR 51.50/MWh mark.

- Spot gold is choppy and resides in a relatively narrow USD 4,453-4,508/oz at the time of writing, vs yesterday’s USD 4,464-4,589.58/oz parameter, with the yellow metal subdued by the firmer dollar. Spot silver, conversely, rebounds following yesterday’s 5% losses.

- Base metals are mixed with newsflow on the quieter side this morning as markets await further US-Iran updates, with its implications watched from inflationary/growth standpoints. 3M LME copper resides in a narrow USD 13,357.00-13,506.00/t range at the time of writing.

- US Private Inventory Data (bbls): Crude -9.1mln (exp. -3.4mln), Distillates -1.0mln (exp. -1.3mln), Gasoline -5.8mln (exp. -2.1mln), Cushing -1.4mln.

- Russia's Kremlin said there is an agreement with China regarding something important on energy. Russia's Kremlin spokesperson Peskov later said the details on the Power of Siberia 2 pipeline still needs to be agreed.

- UK Treasury said Chancellor Reeves is expected to introduce broad reforms that would allow Parliament to authorise critical energy infrastructure projects.

Trade/Tariffs

- The EU has finalised the text of its US trade deal, as the bloc races to meet US President Trump's July 4th deadline. The deal would see the EU remove levies on US industrial goods in exchange for a 15% tariff ceiling on EU exports. EU's von der Leyen later said she welcomes agreement reached by the European Parliament and Council on reducing tariffs for US industrial exports to the EU, while she calls on the co-legislators to move swiftly and finalise the process on this.

- EU Trade Commissioner Sefcovic has reportedly been in contact with US Commerce Secretary Lutnick, US Treasury Secretary Bessent and USTR Greer.

- China's MOFCOM confirmed China will purchase 200 Boeing (BA) jets and said the US is expected to provide engines and parts support for the China Boeing deal. MOFCOM announced a resumption of poultry imports from certain US states and said China reinstated qualified US beef exporter registrations, while it stated the US and China are seeking to extend the Kuala Lumpur trade agreement.

Geopolitics: Iran

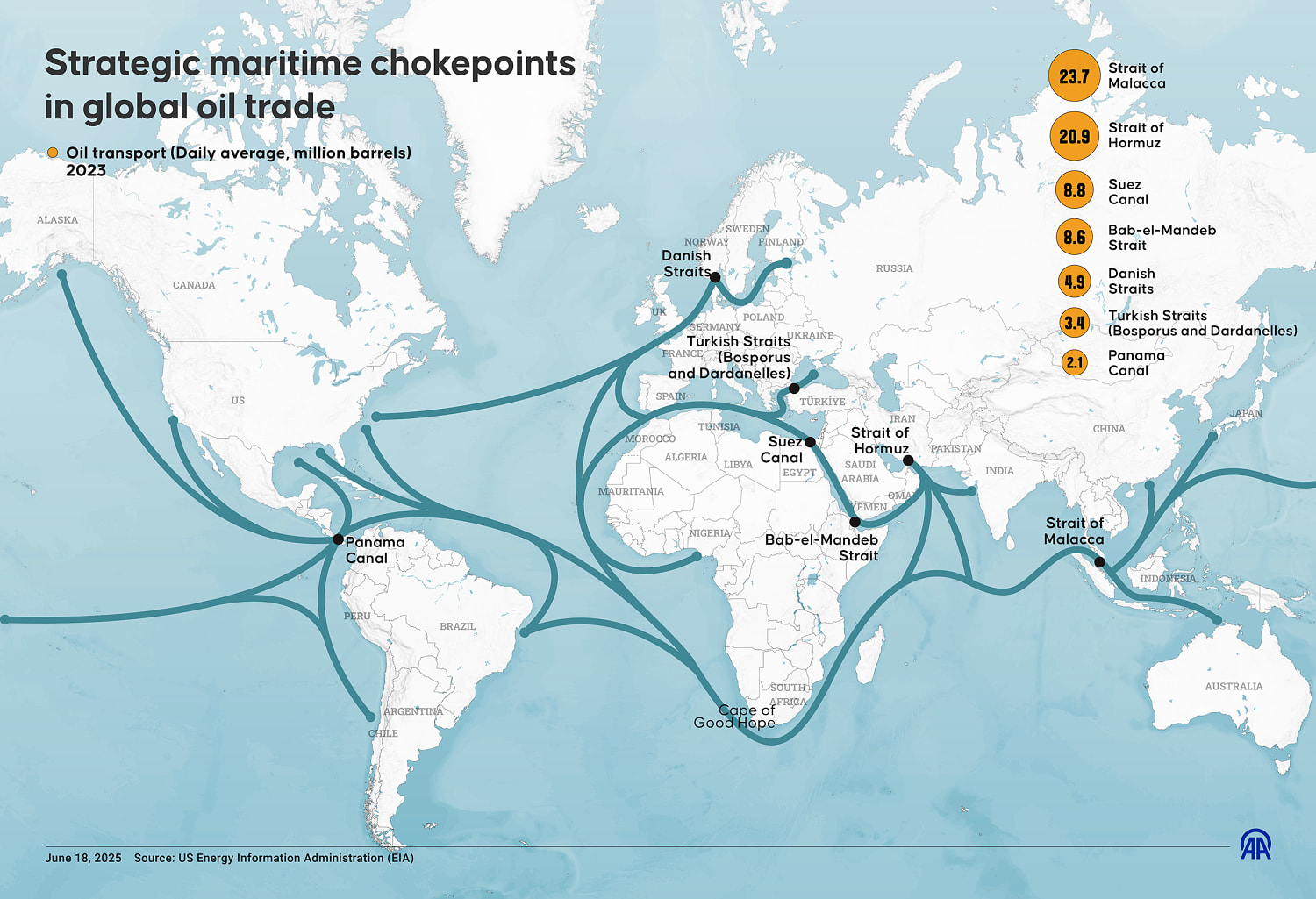

- US intelligence assessment recently showed that US forces identified at least 10 mines in the Strait of Hormuz, according to CBS citing US officials.

- US Senate voted 50-47 to advance war powers resolution that would end US strikes on Iran unless approved by Congress.

- Iran's IRGC said that if the attack on Iran occurs again, the war will extend beyond the region, Fars News reported.

- Iranian Deputy to the President Banah said Tehran is open to negotiations within national interests, Al Mayadeen reported.

- Iranian Foreign Minister Araghchi said months after the start of the war on Iran, US Congress acknowledged the loss of dozens of aircraft worth billions, and Iran's powerful Armed Forces are confirmed as the first to strike down a touted F-35, while he added that with lessons learned and the knowledge they gained, a return to war will feature many more surprises.

- Iran-Pakistan cooperation had declined/stopped over the past two weeks, Al Arabiya and Al Hadath reported citing a senior diplomatic source. A diplomatic source says Iran and Pakistan held conflicting positions on negotiation channels and the venue for talks, and says mistrust was affecting coordination between Iran and Pakistan.

- Pakistan's Interior Minister Naqvi is on route to Tehran, according to Journalist Mallick.

- "On the verge of a decision: Trump and Netanyahu held a phone conversation last night that was described as “lengthy and dramatic,” according to journalist Segal.

- Two Chinese supertankers, carrying 4mln barrels of oil, exited the Strait of Hormuz on Wednesday, according to tracking data. It was later reported that India was preparing to send oil tankers through the Strait of Hormuz following prior reports regarding the Chinese tankers.

Ukraine

- EU governments are discussing whether former ECB President Draghi or former German Chancellor Merkel could represent the bloc in potential negotiations with Russian President Putin, according to FT.

- Russian strike killed two in Ukraine's Dnipro and Ukraine reports multiple regional drone attacks, while Russia claims interception of 273 Ukrainian drones, according to AFP.

- Ukraine's military confirms it struck a Russian oil refinery in the region of Nizhny Novgorod.

Other

- Some Trump advisers reportedly left the US-China summit thinking that a Chinese move on Taiwan was growing more likely, Axios reported. The piece suggested that Taipei is not in panic, at least on the surface

- US President Trump said Cuba is a failed nation that needs help from the US, while he believes a diplomatic deal can be made, according to Semafor.

- US indictment of former Cuban president Raúl Castro is expected to be announced today, according to two federal sources familiar with the investigation cited by NBC News.

US Event Calendar

- 7:00 am: United States May 15 MBA Mortgage Applications, prior 1.7%

- 9:15 am: United States Fed’s Barr Speaks on Consumer Financial Health

- 2:00 pm: United States FOMC Meeting Minutes

DB's Jim Reid concludes the overnight wrap

As we await earnings from Nvidia, the largest company in the world, tonight, the global bond selloff showed no sign of easing yesterday, with yields at multi-year highs around the world. Long-end Japanese yields are rallying notably this morning though after a firm 20yr auction at historically high yields. Nevertheless front end yields everywhere have climbed over the last 24 hours. There hasn't been a single catalyst, but with Brent crude holding above $110/bbl and the Strait of Hormuz still blocked, investors moved to price a growing probability of imminent rate hikes. Indeed, the chance of a Fed rate hike in 2026 moved up to 81%, despite the easing bias in their last statement. And significantly, President Trump seemed open to Kevin Warsh proceeding how he wanted to, telling the Washington Examiner that “I’m going to let him do what he wants to do”.

If you're looking for positives it seems there are three oil tankers currently navigating the Strait this morning, two Chinese and one South Korean. Assuming they get through this would mark one of the busiest days since the closure. So one to watch.

Back to bonds and this upward pressure on yields was clear around the world yesterday, but it was US Treasury yields that saw the biggest jump, with new records across the curve. Most significantly, the 30yr yield (+5.8bps) hit a post-2007 high of 5.18%, whilst the 30yr real yield (+4.0bps) hit a post-2008 high of 2.86%. For shorter maturities, the records weren’t quite so big, but the 10yr yield (+7.9bps) still rose to 4.67%, the highest since January 2025. And with investors bringing forward their rate hike expectations, the 2yr yield (+7.4bps) also hit its highest since February 2025, at 4.12%. The worrying thing would be that with this base in yields formed, where would yields go if strikes resumed on Iran? It's not inconceivable that we'd return to the bond fears seen on April 9th 2025 a week or so after Liberation Day. That ultimately created the conditions for the US to pull back from the maxamalist tariff regime but the session that morning in Asia was pretty fraught.

The latest rise in nominal and real yields kept up the downward pressure on equities as well. In fact, the S&P 500 (-0.67%) fell for a 3rd consecutive session, which is the first time that’s happened since late-March, right before the index staged one of its fastest rebounds ever. Tech stocks led the declines, with the Magnificent 7 (-1.33%) dragging the index lower. But it wasn’t just the megacaps, as the hawkish repricing also meant the small-cap Russell 2000 (-1.01%) had a decent pullback with cyclical stocks seeing a broad underperformance.

Interestingly, yesterday’s rates move came despite pretty stable oil prices, which is noteworthy given how tight the correlation has been between Treasury yields and oil since the Iran conflict began. By the close, Brent crude (-0.73%) was down to $111.28/bbl, though that decline had come after Trump’s comments on Monday evening, with oil prices then creeping higher for most of yesterday’s session. Still, the stabilisation meant inflation expectations actually fell in many countries, and the rates repricing was driven by higher real rates instead. In particular, the 1yr US inflation swap (-1.9bps) fell to 3.37%, whilst the 1yr Euro inflation swap (-2.3bps) fell to 3.84%. The drift lower in Europe came even as natural gas prices recorded an eighth consecutive increase, with TTF gas rising +3.12% to EUR 51.82/MWh, its highest since early April.

In terms of the latest in the Middle East, Trump reiterated his recent threats yesterday, saying that “I hope we don’t have to do the war, but we may have to give them another big hit”. In terms of how long he’d wait, he then said “I’m saying two or three days, maybe Friday, Saturday, Sunday. Something maybe early next week — a limited period of time.” So the prospect of an escalation was still being floated. The mood also wasn’t helped by a Wall Street Journal report that mediators saw little progress in the US-Iran talks. By contrast, Vice President Vance suggested that talks had “made a lot of progress” though he also said “we're locked and loaded” to restart a military campaign against Iran if a deal did not materialise.

In the meantime, there was also a Bloomberg report that NATO was discussing the possibility of a deployment to help ships pass through the Strait of Hormuz. That came from a senior NATO official, who said it was being considered if the Strait isn’t reopened by early July. The article said the proposal had support from several NATO members, but not unanimous support.

Asian equity markets are mostly lower this morning with the KOSPI (-1.98%) the biggest underperformer after Samsung reversed its initial gains, declining by over -4% following the company's announcement that negotiations with the union have collapsed due to unresolved differences on several outstanding issues, leading to the decision to initiate a strike. Elsewhere, the Nikkei (-1.67%) and the S&P/ASX 200 (-1.36%) are also trading sharply lower with the Hang Seng (-0.55%), the CSI (-0.28%) and the Shanghai Composite (-0.66%) out-performing. S&P 500 (-0.18%) and NASDAQ 100 (-0.13%) futures are more stable but European stock futures are down nearly three quarters of a percent.

30yr JGBs have rallied around 10bps this morning after a decent 20yr auction but yields out to 10 years are slightly higher. UST yields are around a basis point lower out to 10yrs this morning.

In monetary policy action, the PBOC left benchmark lending rates unchanged for a 12th straight month as authorities balanced the need to support weak domestic demand against rising inflation risks linked to higher global energy prices. The central bank kept one-year loan prime rate (LPR) at 3.00% and the five-year LPR at 3.50%, in line with market expectations.

In Europe, bond yields also moved up to new highs yesterday. Indeed, the 10yr German yield (+4.4bps) hit to a post-2011 high of 3.19%, and the 30yr German yield (+2.8bps) also hit a post-2011 high of 3.70%. That came as investors dialled up the prospect of an ECB rate hike at the next meeting in June, with the probability up to 89% by the close. Bundesbank President Nagel also pointed in that direction, saying that “This energy supply shock is more persistent, so we are moving away from our baseline scenario”, and that the ECB may “have to do something”. But unlike the US, European equities still managed to post a modest gain, with the STOXX 600 (+0.19%) up for a second day running.

Here in the UK, gilts saw a relative outperformance after a dovish set of labour market data. Notably, the number of payrolled employees was down -100k in April (vs -10k expected), and the unemployment rate for the three months to March rose to 5.0% (vs. 4.9% expected). So that weakness meant investors dialled back the chance of rapid rate hikes from the Bank of England. Indeed, the probability of a hike by the June meeting fell to just 22%, the lowest it’s been in two months. And in turn, gilts outperformed their European counterparts, with the 10yr yield (+3.0bps) seeing a smaller increase to 5.13%.

Over in Canada, the latest CPI print also came in on the dovish side, which led investors to dial back the chance of an imminent rate hike. That showed headline CPI only rising to +2.8% in April (vs. +3.1% expected). Moreover, both of the core measures followed by the Bank of Canada actually fell, with median core down to +2.1% (vs. +2.3% expected), and trim core down to +2.0% (vs. +2.2% expected). So the probability of a rate hike by July fell to just 24%, and in turn that put downward pressure on Canada’s front-end yields. For instance, the 2yr yield (-2.1bps) fell to 3.03%, despite the global moves elsewhere.

On the data front, US pending home sales accelerated to +3.3% yoy in April (vs. +2.1% expected), their strongest annual pace since November 2024. Elsewhere, Eurozone trade data showed the block’s trade surplus falling to 9-month low in March amid higher oil prices and a rising deficit with China. Our European policy analysts discussed the EU push to increase trade defenses against China in a note yesterday (see here).

Looking at the day ahead, the main highlight will be Nvidia’s earnings after the US close. Meanwhile, data releases include the UK CPI print for April just after we go to press. Then from central banks, we’ll get the minutes from the FOMC’s April meeting, and also hear from the Fed’s Barr and the ECB’s Sleijpen.

.jpg?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

{kind=link}

{kind=link}