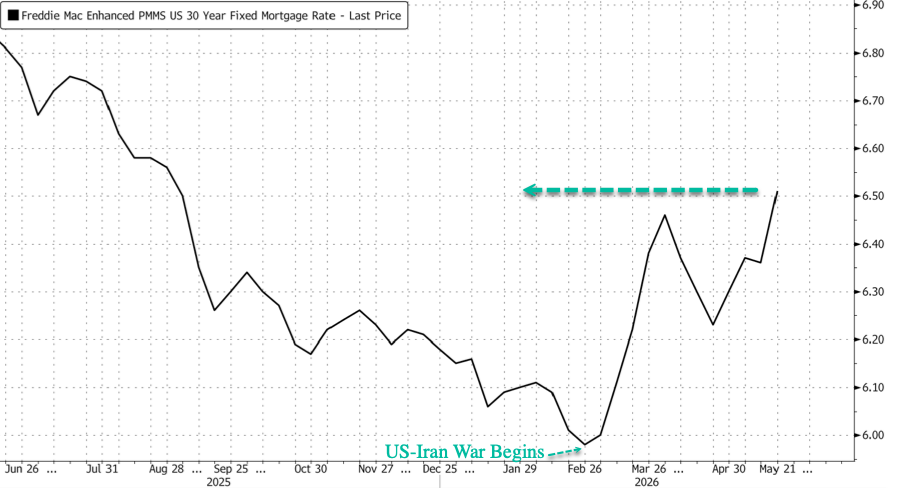

The average rate on a 30-year fixed mortgage climbed to its highest level since August, threatening to derail the spring selling season as higher Treasury yields and renewed inflation pressure push loan costs higher and freeze more prospective buyers out of the market.

Freddie Mac data released Thursday show the 30-year fixed mortgage rate for the week ending May 21 jumped to 6.51% from 6.36%, the highest rate since Aug. 28, 2025.

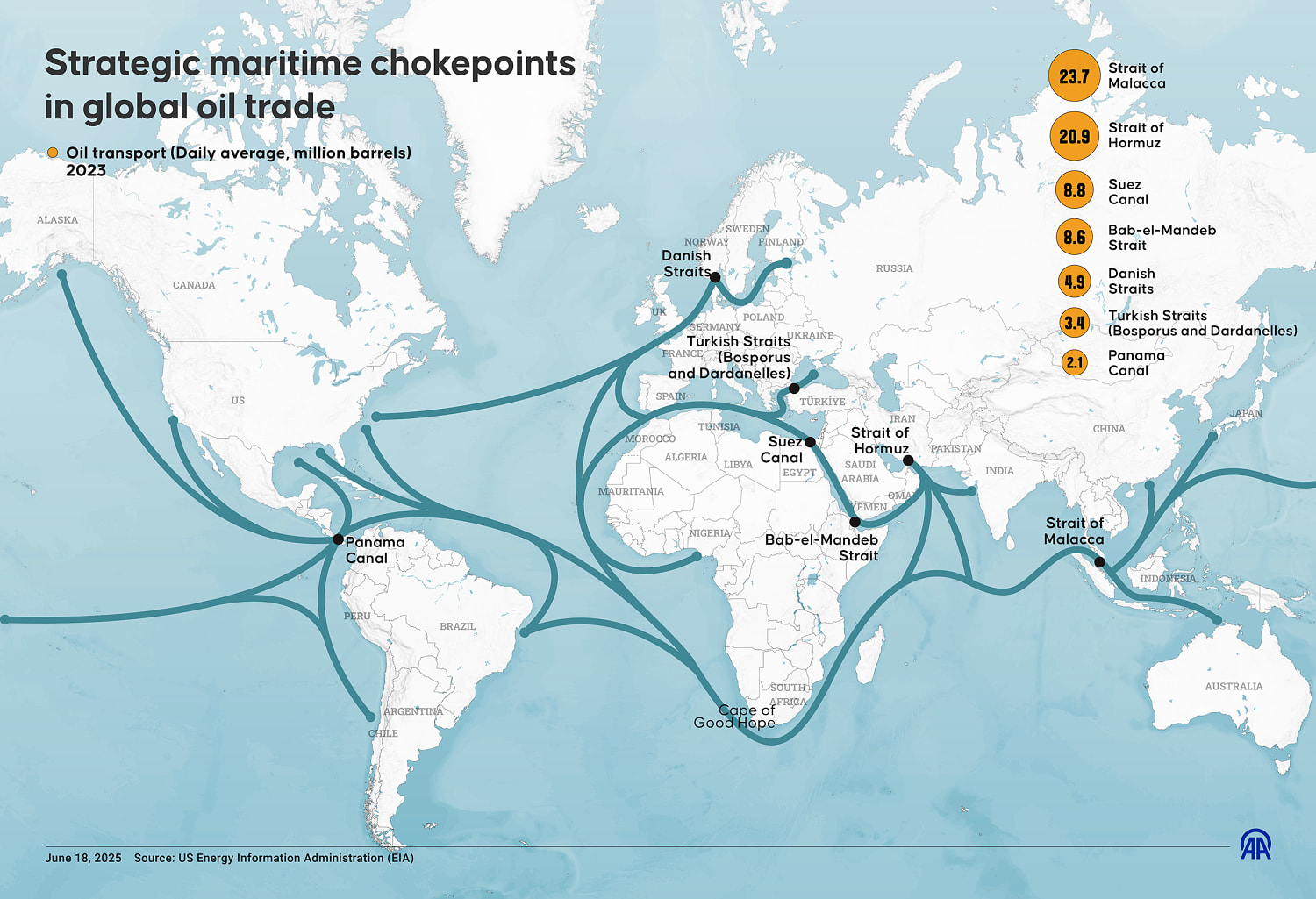

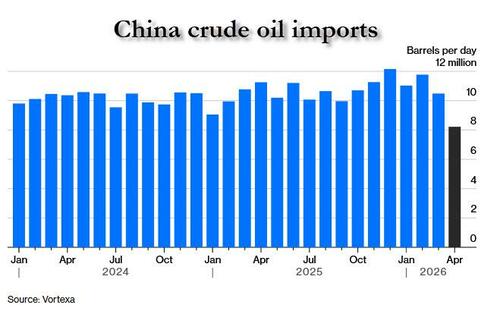

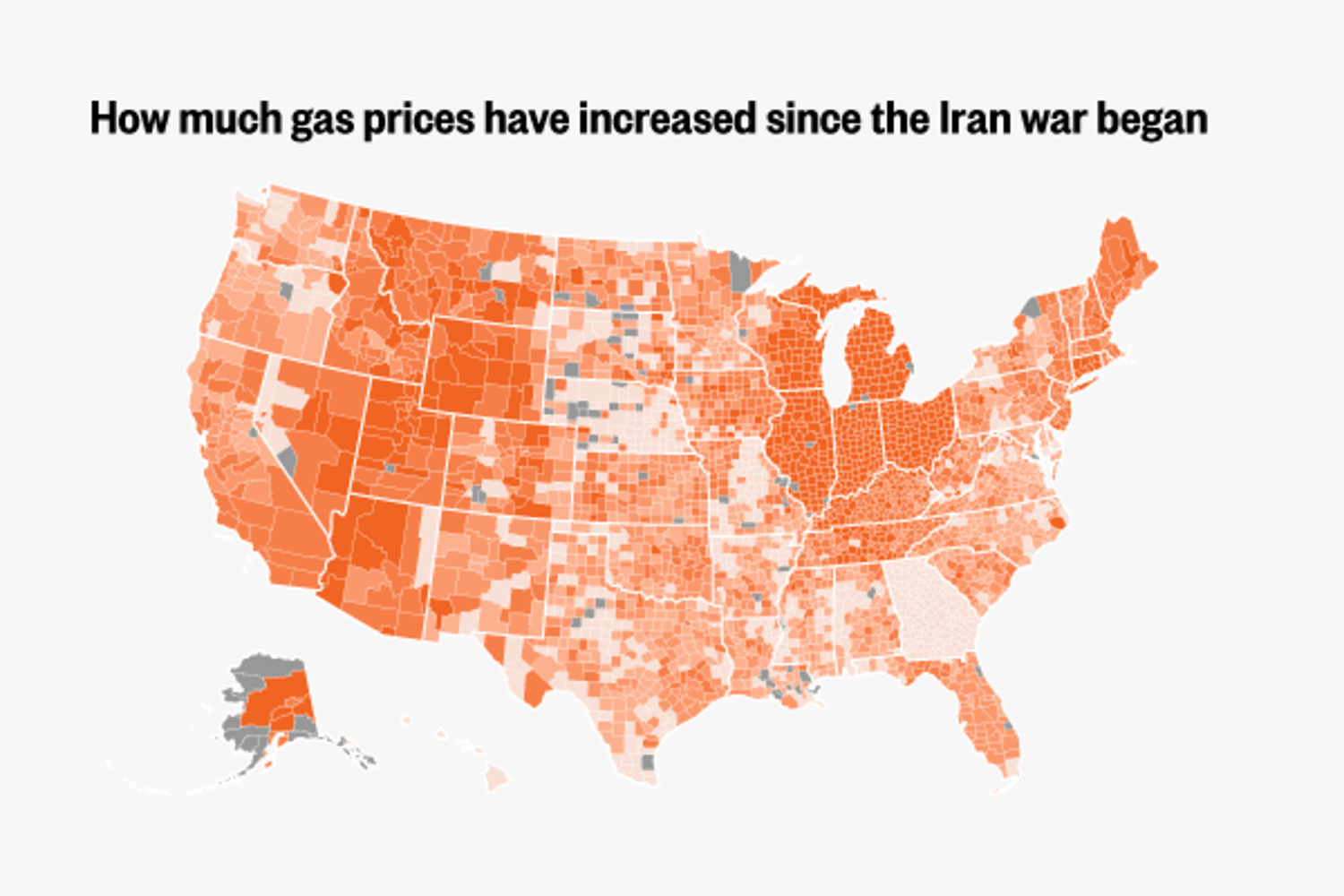

Soaring mortgage rates stem from turmoil in the Gulf region, with the U.S.-Iran war driving up oil prices, inflation, and bond yields over the last three months. Rates on 10-year Treasuries hit their highest level in one year, while 30-year yields neared 2007 highs.

Mortgage rates fell to around 6% in early February, lifting hopes for a housing market rebound after three consecutive years of depressed activity. Yet hopes for a robust selling season were dashed because the conflict in the Middle East began in late February, and once the Hormuz chokepoint closed, energy prices surged, followed by rates.

"Each uptick in rates narrows the pool of buyers who can make the numbers work," Realtor.com analyst Anthony Smith told News Corp.

The impact of higher rates is significant for buyers: Before the conflict, a buyer with a $2,500 monthly budget and 20% down could afford about a $400,000 home at a 6% mortgage rate, but only about $384,000 at a 6.5% rate.

Realtor.com analyst Jake Krimmel told Bloomberg, "We've been surprised so far that we haven't seen deterioration like we did this time last year."

"May is where the rubber will meet the road because that's when things tend to really start picking up," Krimmel said.

The end result of surging rates over the last few months was flat existing-home sales in April, well below Bloomberg Consensus expectations.

The continued housing market slowdown, which feels like an eternity for those in the industry, has pressured businesses tied to housing, such as furniture manufacturers, home builders, mortgage lenders, and real estate brokerages.

Home improvement retailers such as Home Depot and Lowe's warned this week that consumers remain reluctant to splurge on big-ticket home improvement items, as elevated mortgage rates, high home prices, energy inflation, weakening sentiment, and broader macroeconomic uncertainty weigh on demand.

Lowe's CEO Marvin Ellison warned analysts earlier this week that the housing market is the "most difficult" since the financial crisis.

He continued:

I think overall this has been the most difficult housing market that I've faced in this business since the financial crisis. And as Brandon mentioned, it's almost exclusively or disproportionately on the DIY customer.

That's the majority of where our revenue comes from. And so I look at it from this perspective, you know, we've delivered four quarters of positive comps in an environment where the DIY has faced more economic pressure than I've ever seen before.

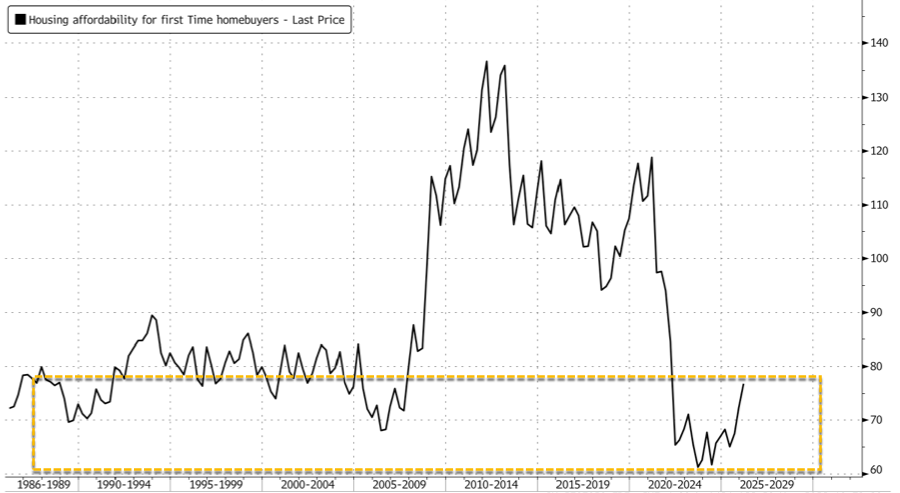

Housing affordability for first-time homebuyers remains at a four-decade low.

"Decisions made during the period of ultra-low interest rates coming out of the pandemic are still shaping behavior," said Torsten Slok, the chief economist at Apollo Global Management, citing the unwillingness of homebuyers with sub-4% rates to move. "The shift to higher rates has fundamentally changed the economics."

"If you're looking for relief on 30-year conventional mortgage rates, you're not going to get it anytime soon," said Kevin Flanagan, head of investment strategy at WisdomTree.

Nick Barta, a regional manager at Security First Financial, a Colorado-based mortgage company, told Bloomberg that the surge in rates because of the US-Iran war has had a chilling effect on the industry so far.

"All you hear about is gas prices and higher interest rates," said Barta, who has worked in the mortgage industry for nearly four decades. "It freaks people out."

President Trump has directed Fannie Mae and Freddie Mac to begin buying $200 billion in mortgage-backed securities to pressure mortgage rates lower.

"FHFA and the administration are actively evaluating a range of tools and policy options to improve affordability and expand access to homeownership for American families," Federal Housing Finance Agency Director William Pulte said.

Sarah Wolfe, a senior economist at Morgan Stanley Wealth Management, warned that higher mortgage rates continue to leave an entire generation of homebuyers stuck in rentals.

"They want the same things as the generation before them," Wolfe said, "and the bar to entry is getting higher and higher."

.jpg?branch=production&format=jpg&width=1024)

.png?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

{kind=link}

{kind=link}

{kind=link}

{kind=link}