Unless you have lived under a rock for the last year (or month), you will know that the explosive growth of artificial intelligence is fueling a massive infrastructure buildout.

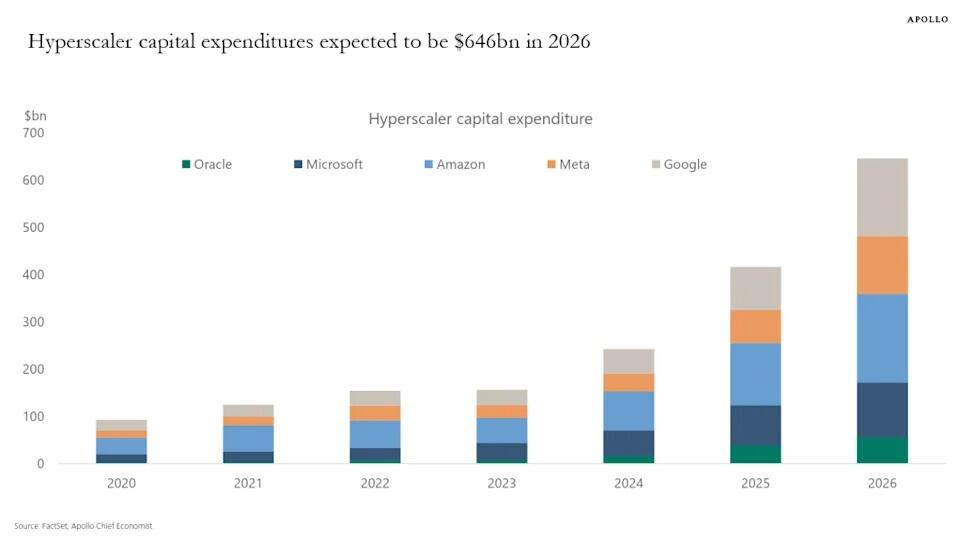

In a chart book published nearly simultaneously with Moody’s report, Apollo Global Management chief economist Torsten Slok worked to put the enormity of data center spending into perspective.

With total capital expenditure on data centers estimated at roughly $646 billion, or about 2% of U.S. GDP, Slok noted that is roughly equivalent to the GDP for Singapore, Sweden, and Argentina. Defense spending in 2025, meanwhile, was around $917 billion.

However, as Moody's warned this week, the aggressive financing structures supporting this explosive growth are creating significant systemic risks that could ripple across global credit markets and the broader economy.

The most recent example of this buildout - and its coincident debt-funding - is the $36 billion debt financing package currently being shopped by Apollo Global Management and Blackstone to enable Anthropic’s large-scale acquisition of Google’s custom TPU chips.

As Bloomberg reports, this complex, high-leverage deal - partially backed by Broadcom - underscores how private equity and specialized financiers are channeling enormous capital into AI hardware and data centers through layered debt instruments.

The move would mark one of the largest-ever private credit deals and also the biggest chip-financing debt transaction.

It aims to tap Broadcom’s credit quality to provide computing-power access to Anthropic, which just eclipsed rival OpenAI in valuation (and its ecosystem has been dramatically outperforming)...

While such deals accelerate AI capacity, they also concentrate risk.

More concerning is the scale of hidden liabilities across the industry.

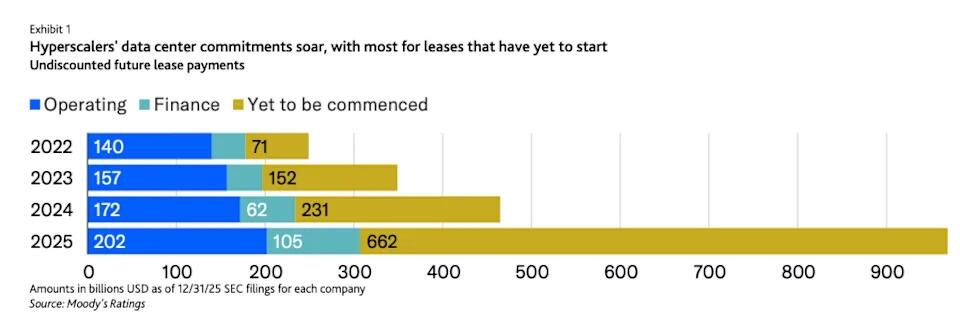

According to Moody’s Ratings, the five major U.S. hyperscalers (Amazon, Meta, Alphabet, Microsoft, and Oracle) have accumulated approximately $662 billion in future data center lease commitments that have not yet commenced.

Combined with other commitments, the total undiscounted future lease exposure reaches $969 billion.

To put the scale of this hidden obligation into perspective, Moody’s accounting analysts David Gonzales and Alastair Drake calculated that the unrecorded $662 billion is equivalent to 113% of these five hyperscalers’ most recent adjusted debt.

These obligations remain entirely off-balance-sheet under current accounting rules, despite representing binding long-term liabilities.

But as Gonzales told Fortune in a statement that it’s “not as if [these hyperscalers] have have avoided a liability through structuring,” characterizing the $662 billion at issue as “yet to be on the balance sheet,” rather than missing.

“More accurately,” he added, “they have not yet received the services to trigger this liability as of this time, but they will.”

This accounting deferral masks the true leverage in the system.

As these leases activate over the next decade, they will migrate onto balance sheets, potentially weakening credit profiles, elevating leverage ratios, and increasing refinancing pressures.

While the AI infrastructure boom promises transformative productivity gains, Moody's is basically highlighting that the current funding model - reliant on massive off-balance-sheet debt and complex private financing - builds hidden vulnerabilities into the financial system.

Regulators, investors, and policymakers should closely monitor these exposures.

Heightened Systemic Concerns

-

Contagion Risk: Heavy interdependence among hyperscalers, private credit funds, and infrastructure investors means distress at a few large players could rapidly spread through debt markets and counterparty exposures.

-

Concentration & Interconnectedness: A small group of tech giants and a limited pool of specialized financiers dominate this financing. Any material setback in AI monetization or power availability could create correlated losses across the sector.

-

Broader Market Impact: The $662 billion in off-balance-sheet exposure represents a delayed but massive claim on capital markets. In an economic downturn, forced deleveraging or asset fire sales could amplify volatility, tighten credit conditions, and affect investor confidence well beyond technology.

-

External Amplifiers: Power grid constraints, regulatory hurdles, and geopolitical supply chain risks further compound the fragility of these highly leveraged bets.

In a stressed scenario - such as slower-than-expected AI revenue growth (the end of tokenmaxxing), rising energy costs, or higher interest rates - the simultaneous activation of these liabilities could trigger widespread credit rating downgrades and liquidity strains.

Specifically, Moody’s warned that these opaque accounting practices mask the true economic risk facing the tech industry. While leasing reduces upfront capital investments, carrying such massive future commitments severely limits a company’s financial and operating flexibility, especially if AI industry conditions change rapidly.

Because these liabilities are hidden, Moody’s concluded, in its own jargony way, that it is considering new ways to look at this issue.

“The accounting liability is unlikely to reflect certain plausible future scenarios … With this in mind, we will continue to assess cash exposures and debt-like adjustments as time progresses and the dates of new leases draw nearer. We may make a nonstandard adjustment to Moody’s adjusted debt based on our expectation of likely cash outflows.”

Without greater transparency and more resilient capital structures, the race for AI supremacy risks generating systemic stress that could undermine broader economic stability.

.png?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.JPG?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.png?branch=production&format=jpg&width=1024)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}