The market may be in full-blown face-ripping bubble mode, and software stocks are now gripped in by a category 5 gamma squeeze hurricane, but not even that is helping the ongoing debacle that is private credit.

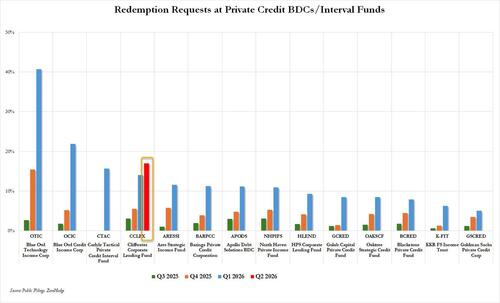

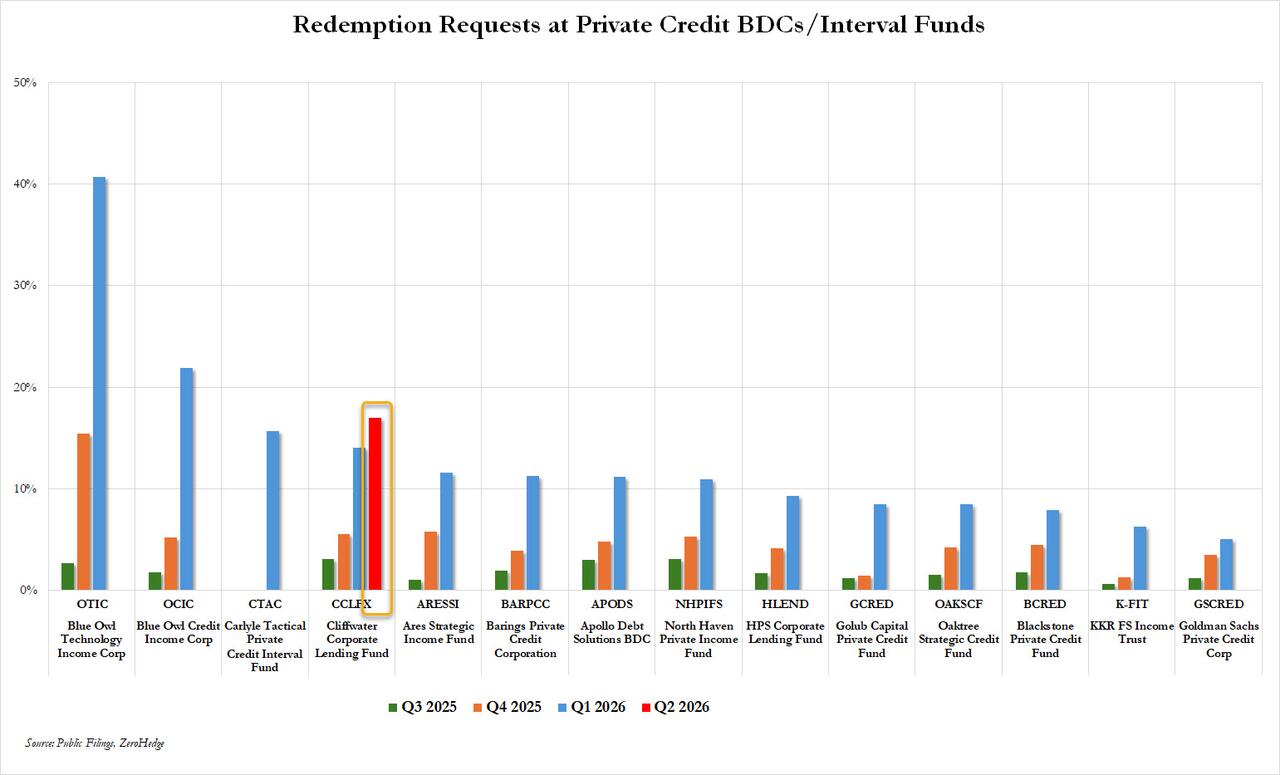

The flagship private credit fund of Cliffwater, a fund which has was slammed by redemption requests in the past quarter as the private credit crisis came to a fore, has again gated investors by capping redemptions at 5% in the second quarter after investors looked to pull more than three times that amount, or 17% of shares, Bloomberg reported, in a sign of relentless pressure on the $1.8 trillion market.

The $31 billion Cliffwater Corporate Lending Fund informed shareholders Tuesday that they’d get about one-third of their requested money back, according to a letter seen by Bloomberg. The prior quarter, investors got back around half of the roughly 14% they asked for, with the vehicle choosing to cap withdrawals at 7%.

Shortly after Cliffwater’s decision in March, S&P Global Ratings lowered its outlook on the interval fund to negative from stable, warning that the 5% redemption threshold is “an important guardrail.”

“Our repurchase program is intentionally designed to provide shareholders with periodic liquidity that aligns with the fund’s long-term investment strategy and its underlying assets,” Cliffwater CEI Stephen Nesbitt said in the letter to investors. And by periodic liquidity he meant far less liquidity than investors hoped to recovery.

The firm previously said that the fund, which has delivered a roughly 9.4% annualized net return since it was formed in 2019, has enough liquidity to meet 5% redemptions for more than a year without selling a position or an asset. After a second straight quarter of gating that may be tested very soon.

Cliffwater has become something of an unlikely giant in the private credit market by raising money at a rapid clip and deploying it across both direct loans and funds that do such lending themselves. Other non-traded business development companies are set to report the results of their second-quarter tender offers in the coming weeks. In the previous period, some like Blackstone’s BCRED went to extraordinary lengths to let investors cash out (all for nothing as the looming redemption flood will overrun even the giant fund), while other funds at Apollo Global, BlackRock and Blue Owl enforced their 5% caps.

.jpg?branch=production&format=jpg&width=1024)

.png?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.JPG?branch=production&format=jpg&width=1024)

{kind=link}