By now, readers have a clear understanding that the Gulf-driven energy shock is on course to collide with a potential super El Niño weather event, creating what could be a dangerous second-order shock to food supply chains around the world.

The concern is that extreme heat and disrupted rainfall patterns could hit top agricultural growing belts, dent harvest output, and amplify existing supply stress. Even before those weather-driven impacts fully materialize, global food prices are already rising, suggesting that fertilizer and elevated diesel prices are beginning to be transmitted through the broader food supply chain.

Our Tuesday note on Thailand white rice, a regional Asian benchmark, surging 20% in May, the largest monthly increase in data going back to 2008, is another warning signal that the price action in the grain feeding half the world has entered a new upward impulse.

The troubling move in rice prices, including a 15% surge in Chicago rice futures last month, indicates that food-inflation pressures are already materializing. The concern is that these pressures could materially worsen once El Niño-driven weather disruptions begin affecting key growing regions.

UBS analysts led by Leigha Miyata published a note titled "Food Inflation & El Niño Evidence Check," confirming what we have been tracking for months: the Middle East-driven fertilizer shock is now moving through the global food supply chain just as El Niño risks rise, creating the potential for an inflation surge across Asia later this year into 2027.

Miyata noted that El Niño odds currently stand around 82% for May to June and 96% for December into early 2027, raising the risk of hotter, drier conditions across South and Southeast Asia that could pressure harvests.

Via Miyata ...

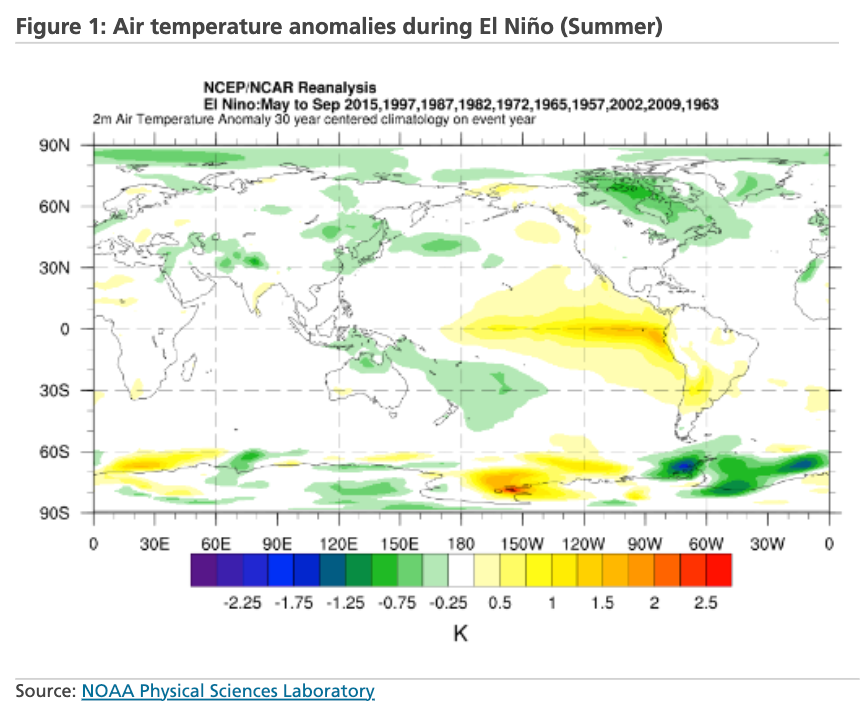

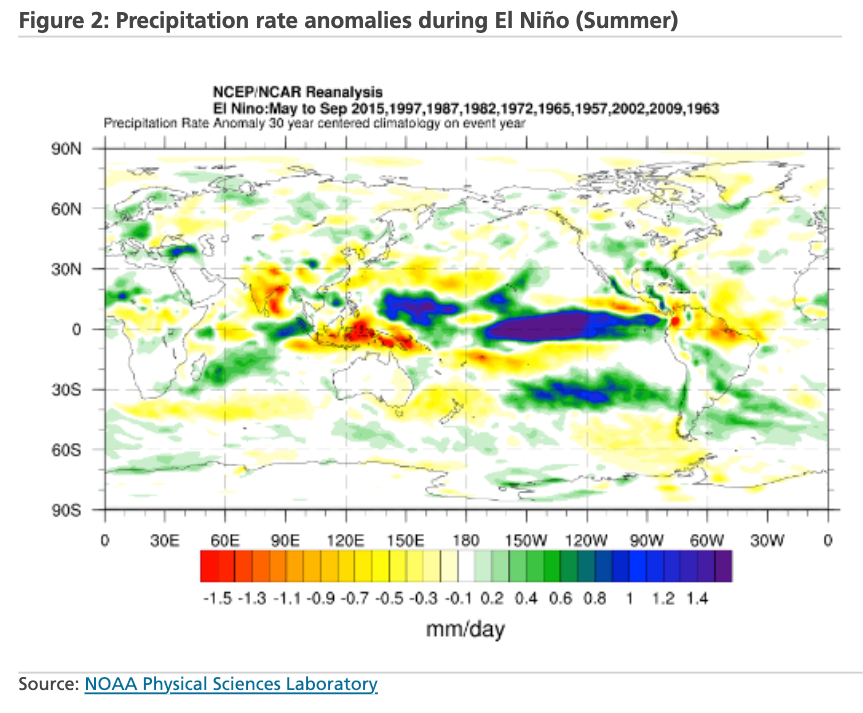

El Niño likelihood raised to 82%; expect Asia to be hotter and have less rain:

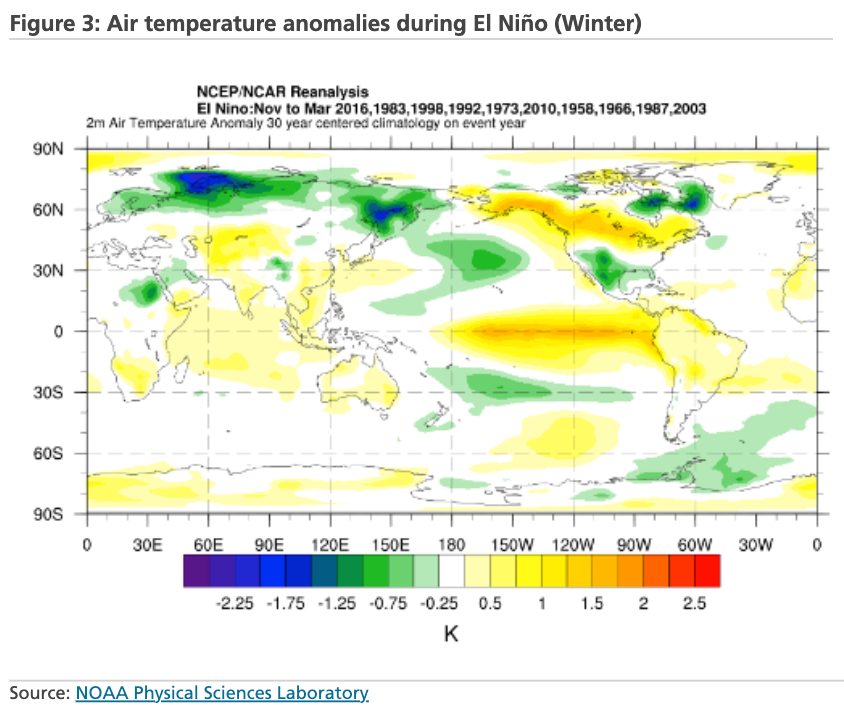

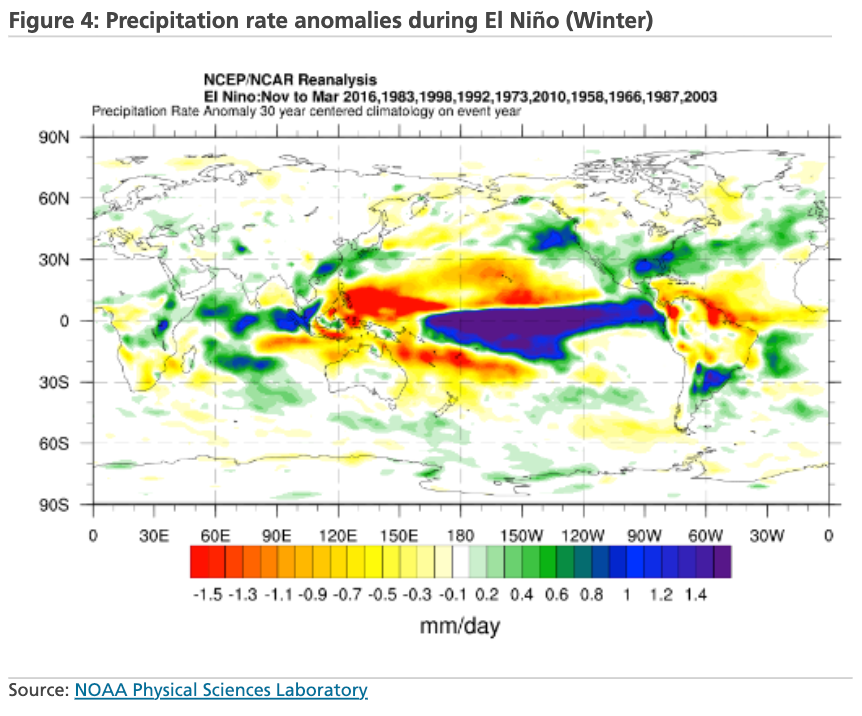

The El Niño is likely to emerge soon (82% chance in May-July 2026) and continue through Northern Hemisphere winter 2026-27 (96% chance in Dec 2026-Feb 2027, NOAA). Historical patterns show higher temperatures in Indonesia and northern Australia (Figure 1). Temperatures are normally lower in South Korea and Japan, though a "super El Niño" could reverse this, bringing intense heat and rainfall. Precipitation is lower in South and Southeast Asia, posing risks to harvests (Figure 2). Other El Niño impacts include higher power demand, lower supply, and increased disease risk (see p3).

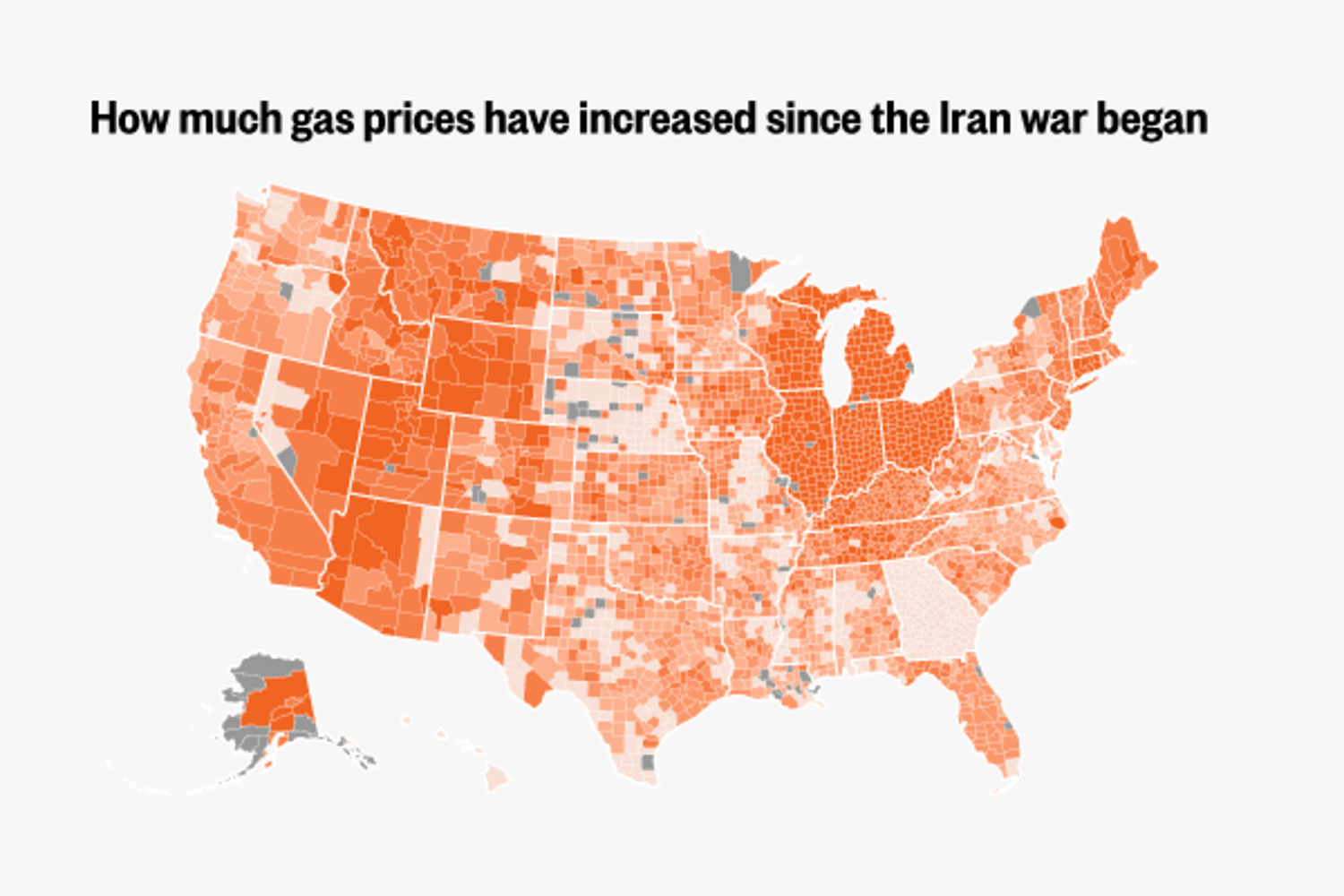

Fertilizer Prices - Urea prices correcting, now +23% since the Iran conflict started:

Though nitrogen supply remains tight, we have seen diverging trends in the last few weeks on the product level. Ammonia pricing has been stable to higher, UAN pricing has been stable, while urea pricing has seen downward corrections, $190/MT (~23%) lower than its peak level in April. Overall the UBS chemicals team see this pointing to the market having moved past peak seasonal tightness, with 2Q likely marking the high point. We believe structurally tight supply from restricted trade flows and constrained production will continue to support the pricing outlook for 2H26/2027 above the cost curve however, and note that physical market flows have yet to improve (full report).

Gov't measures have been helpful, but inflation is rising across Asia:

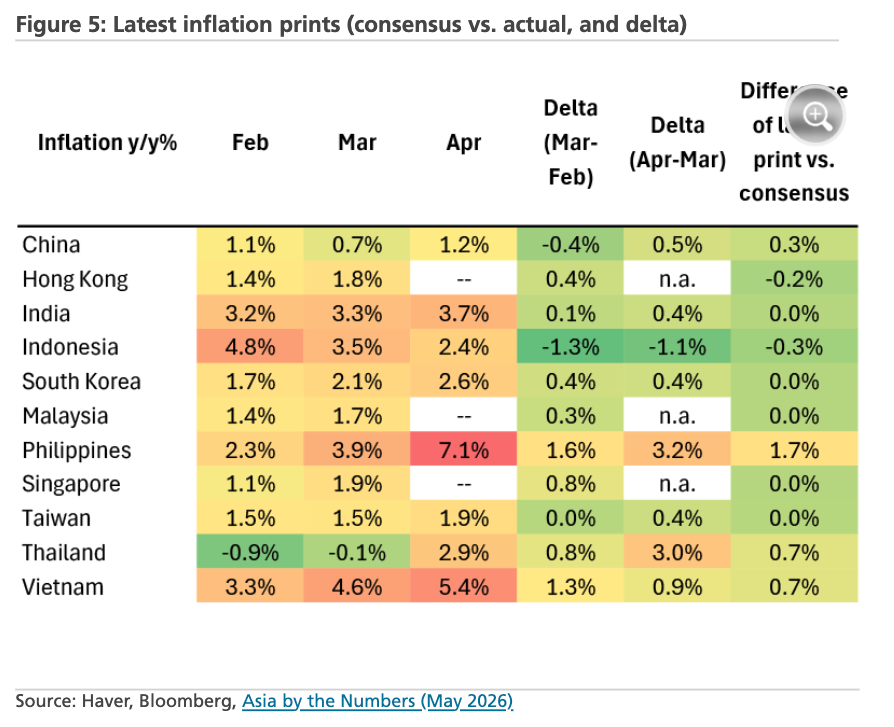

The FAO Food Price Index averaged 130.7 points in April 2026, up 1.6% from March, marking a third consecutive rise but at a slower pace. Gains in vegetable oils, meat, and cereals were partly offset by declines in sugar and dairy. The index was 2.0% higher year-on-year but remained 18.4% below its March 2022 peak. Inflation across all major Asian economies is increasing with the exception of Indonesia and Japan, and corn futures for 2026/2027 are up ~4%/5% since the Iran conflict started. UBS economists explain that inflation was likely lower in many Asian economies due to quick policy-action post Iran conflict, but that inflation will likely rise going forward (full report). In the Philippines, the level of inflation has shot up from 2.3%/3.9% in Feb/Mar to 7.1% in Apr. In Thailand, deflation in Feb/Mar has shifted to 2.9% inflation in April (Figure 5). For Japan, there are no clear signs yet of strong inflationary pressure from Middle East tensions. However, we expect national CPI for May to pick up slightly to 1.5% from 1.4% in April, suggesting April was likely the trough. Food inflation in Japan decelerated from 4.6% YoY in April to 4.1% YoY in May, though on a MoM basis, food inflation rose 0.3% (full report).

Packaging and freight costs are up; El Niño in 2026-27, fertilizer impact in 2027:

Plastic packaging prices in Japan are reported to be up 20 to 30%. This together with transport costs are expected to raise food prices, but this is not yet visible in the data for Japan. If El Niño materializes, we may see drought impact the harvests in Sep 2026- and Apr 2027- in South and Southeast Asia. Higher fertilizer costs may also affect harvests from April 2027 onwards.

UBS views on El Niño impacts

1. Agri-business: Tightening global balances and large speculative shorts mean an El Niño-driven disruption to India's monsoon could reduce sugar production by ~3–8mn tons YoY and trigger price spikes.

2. Agriculture & Inflation (India): El Niño-driven weak monsoon risks (forecast ~92% of normal rainfall) could lift food inflation, though only ~21% of CPI is directly impacted, limiting first-round effects but raising second-round risks if shocks persist.

3. Health Care (Brazil): El Niño-driven changes in mosquito patterns could increase dengue cases, with prior events (2023/24) coinciding with record infections (~6.6mn cases).

4. Thermal coal / Power demand: A potential "super El Niño" could drive extreme heat across Asia, boosting electricity demand (especially for cooling) and increasing coal demand and imports, tightening seaborne markets.

5. Hydropower / Power supply: El Niño-related rainfall shifts could reduce hydro generation in LatAm and Africa, further supporting demand for thermal coal.

6. Insurance / Reinsurance: El Niño conditions are associated with below-average hurricane activity, which could improve insurers' near-term book value but pressure pricing due to increased capital supply. In Australia, El Niño years tend to have lower catastrophe losses, though drought and bushfire risks rise.

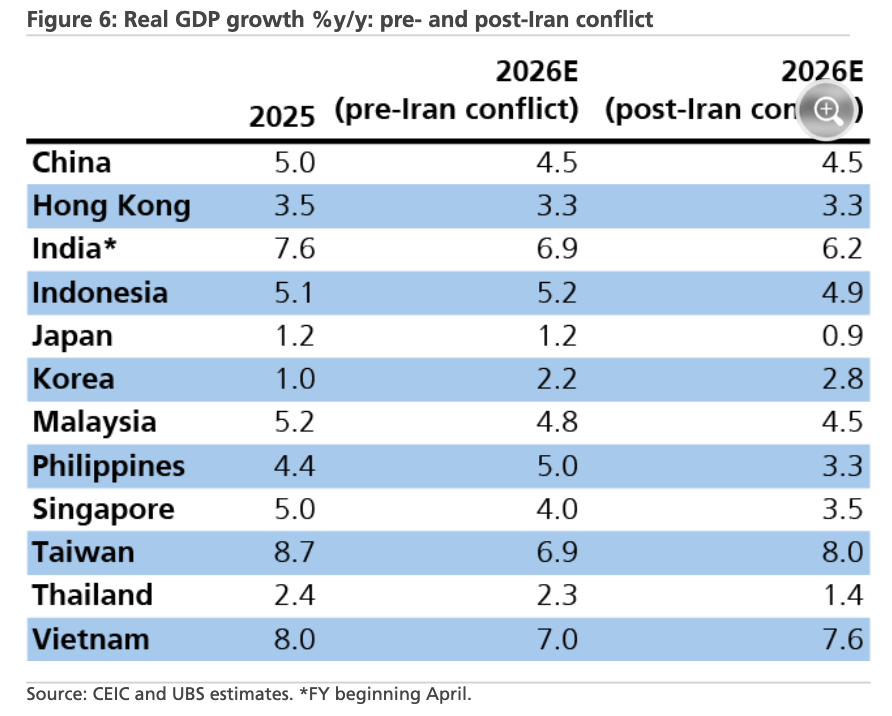

Figure 6: Real GDP growth %y/y: pre- and post-Iran conflict

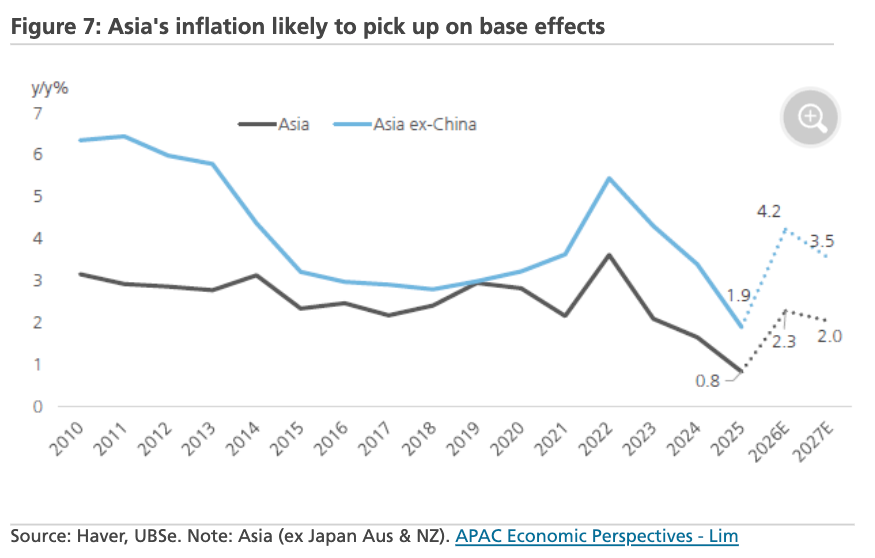

Figure 7: Asia's inflation likely to pick up on base effects

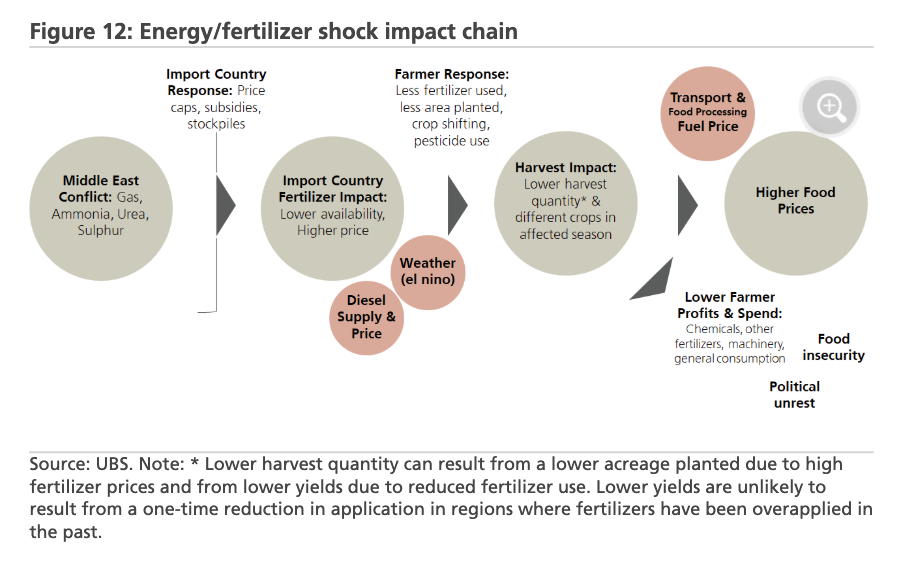

Figure 12: Energy/fertilizer shock impact chain

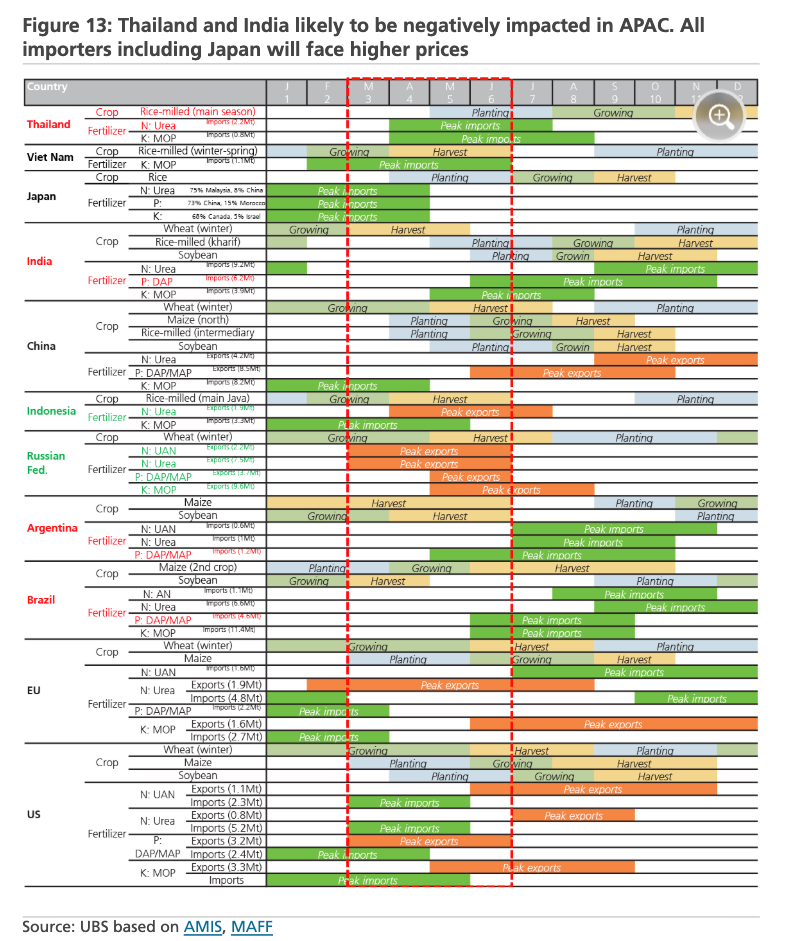

Figure 13: Thailand and India are likely to be negatively impacted in APAC. All importers, including Japan will face higher prices

Related:

-

We Are 6 Months From Global Food Shortages Because Farmers Are Facing A Quadruple Whammy Crisis

-

Everyone Talks About The Cost Of Gasoline... Soon Everyone Will Be Talking About The Cost Of Food

Last month, ZeroHedge Debates held a roundtable to ask, "How bad will the food inflation mess get?"

Professional subscribers can read the full "Food Inflation & El Niño Evidence Check" here at our new Marketdesk.ai port.

.jpg?branch=production&format=jpg&width=1024)

.png?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.JPG?branch=production&format=jpg&width=1024)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}