Submitted by QTR's Fringe Finance

This week was proof that the inflation story that markets desperately want to go away refuses to cooperate. It also adds to the case that new Fed chair Kevin Warsh could have his hands tied — and may ultimately need to redefine inflation to untie them.

This week the Bureau of Labor Statistics reported another really ugly wholesale inflation print, adding to a growing pile of evidence that inflation pressures are proving far more persistent than policymakers, economists, and investors had hoped.

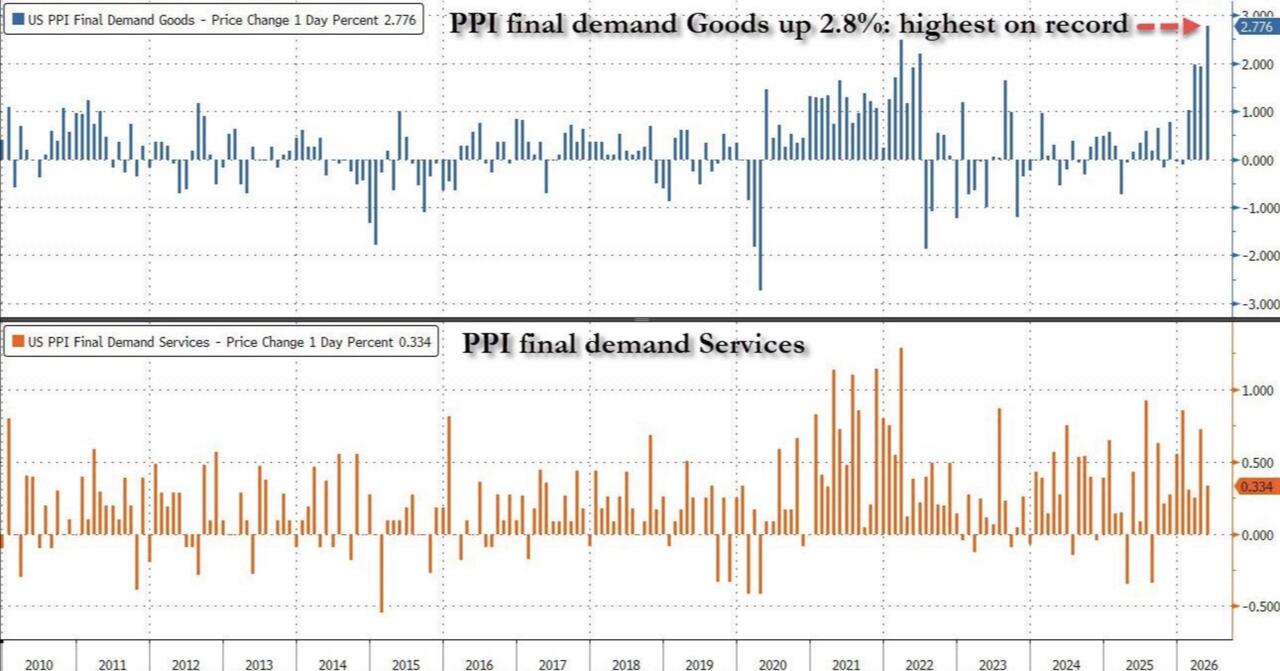

The Producer Price Index rose 1.1% in May, well above economist expectations of 0.7%. On a year-over-year basis, wholesale inflation accelerated to 6.5%, the highest reading since November 2022.

Even though core PPI, which excludes food and energy, came in slightly below expectations at 0.4% versus estimates of 0.5%, that distinction shouldn’t provide much comfort. The headline figure remains extraordinarily elevated, and businesses are still dealing with rising costs that eventually work their way through supply chains and into consumer prices. CNBC reported:

Most of the acceleration in the PPI — nearly 80% — came from a 2.8% surge in final demand goods prices, the biggest increase ever in a data series going back to December 2009. In turn, 80% of that increase came from a 10.7% jump in energy.

Zero Hedge posted the following chart on X showing the jump:

Economist Peter Schiff noted on X:

Producer prices spiked 1.1% in May, following a downwardly revised 1.1% rise in April. That's back-to-back months of 14% annualized increases. So far in 2026, the PPI is already up 4%. If this pace continues, it will rise 10% in 2026, matching the 2021 gain, the most since 1980.

PPI is often viewed as a leading indicator for future inflation because it measures costs before they reach consumers. When businesses face higher input costs, those costs rarely disappear into some magical accounting black hole. They generally get passed along. Companies can absorb some pain for a while, but eventually somebody pays the bill. Historically, that somebody is the consumer.

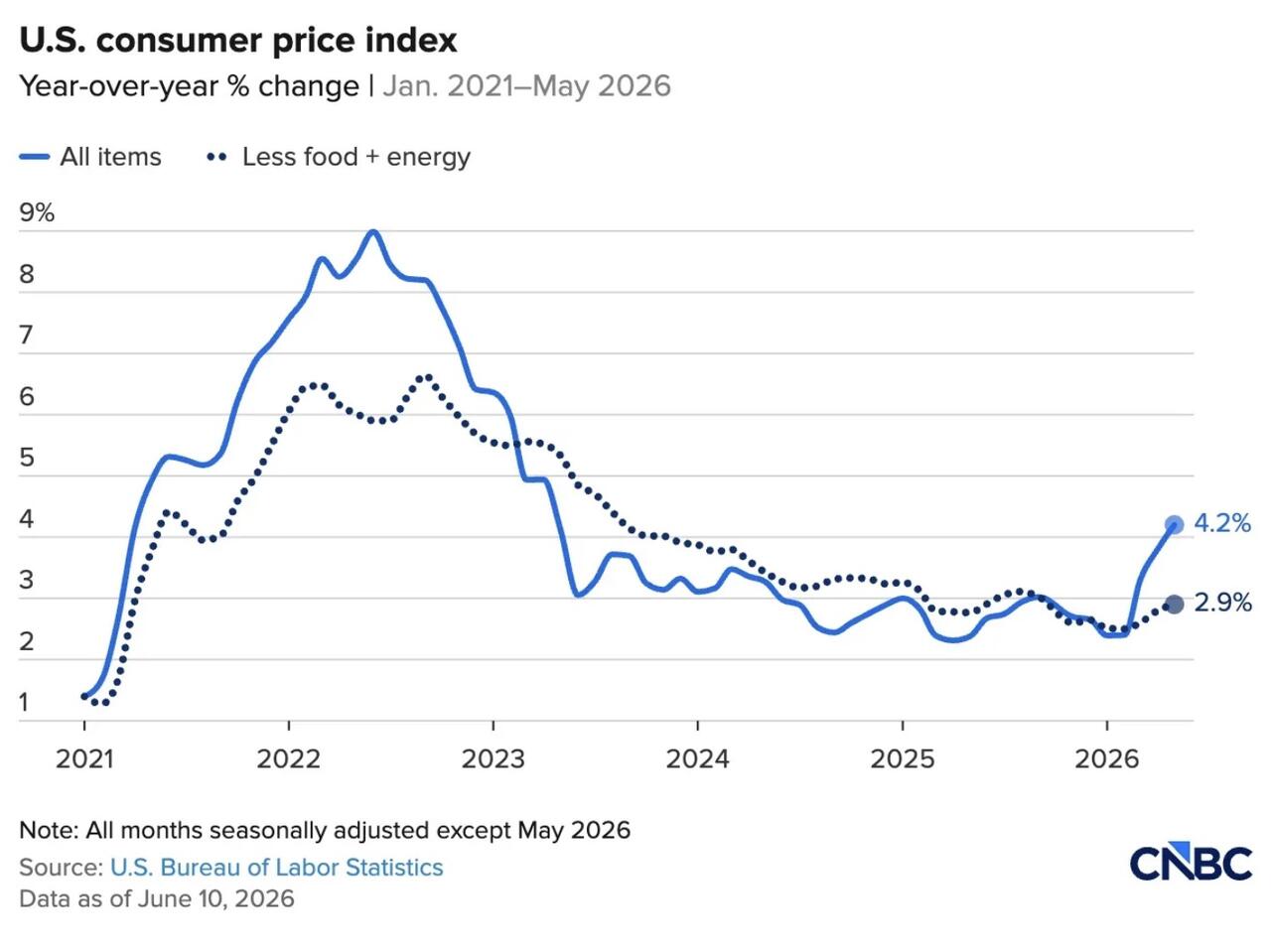

The significance of today’s report extends beyond a single monthly data point. It comes on the heels of yesterday’s CPI report, which showed inflation accelerating once again. The Consumer Price Index rose 0.5% during the month, pushing annual inflation to 4.2%. While both figures matched economist expectations, that hardly qualifies as good news.

In fact, inflation has now climbed above 4% for the first time in three years and sits at its highest level since April 2023. Personally I’m not sure how it could be made any clearer to the market that rates are going to have to hold steady or move higher than being nowhere f*cking near the Fed’s 2% “target”.

But markets seem determined to celebrate inflation reports whenever they merely meet expectations. However, there is a difference between meeting forecasts and solving inflation. The Federal Reserve’s target remains 2%. Inflation is currently running at 4.2%. That isn’t victory. It’s more than double the Fed’s target.

Taken together, yesterday’s CPI report and today’s PPI report paint a picture that should make rate-cut enthusiasts increasingly uncomfortable. Consumer inflation is accelerating. Wholesale inflation is accelerating. Energy prices are pushing higher. And the broad disinflation narrative that markets spent the better part of the last year embracing is showing signs of breaking down.

Last month, I argued that markets were underestimating how quickly the conversation could shift from rate cuts to rate hikes. At the time, that seemed like an aggressive position. Most investors were still operating under the assumption that inflation would continue drifting lower, growth would soften in an orderly fashion, and the Fed would eventually ride in with rate cuts to keep the party going.

That assumption looks considerably shakier today. And every inflation report that comes in hot further limits the Federal Reserve’s options.

At best, this data supports a case for keeping rates elevated for significantly longer than markets would like. At worst, it supports a growing argument that the next move from the Federal Reserve may not be lower rates at all…it may be higher.

That possibility still sounds absurd to many investors because markets have spent years conditioning themselves to expect monetary accommodation whenever conditions become uncomfortable. Somewhere along the way, investors became convinced that central banking was supposed to function like a customer service call center for the S&P 500.

Stocks down? Cut rates. Economy slowing? Cut rates. Credit markets stressed? Cut rates. Investors sad about the death of their pet goldfish? Cut rates. Octogenarian billionaires complaining about flatulence that investments are giving them? Cut rates.

Unfortunately for that crowd, inflation doesn’t particularly care about market expectations, portfolio allocations, or CNBC panel discussions about why six cuts are definitely coming next year.

The Fed can tolerate slower growth. It can tolerate weaker sentiment. It can tolerate hedge fund managers with gas and anchors nearly shitting themselves on financial television. What it cannot tolerate indefinitely is inflation running more than double its target while wholesale prices reaccelerate to levels not seen in years.

And that’s where this vice grip keeps tightening. This market is already facing a half-dozen serious roadblocks and questions that all investors should know about. I wrote about them earlier this week and it’s a free read here.

Now, every hot inflation report removes another degree of freedom from policymakers. Every upside surprise forces markets to reconsider assumptions about lower rates, easier financial conditions, and endless liquidity. Every month that inflation remains elevated increases the probability that “higher for longer” eventually becomes “higher still.”

That’s bad news for an economy that has spent the better part of fifteen years becoming addicted to cheap money.

🔥 80% Off If You Subscribe Today. This coupon allows for 80% off of annual subscriptions and results in a 85% savings over paying the monthly rate for a subscription to the blog. You keep the discounted rate for as long as you wish to remain a subscriber.: Get 80% off forever

Higher rates don’t simply affect stock valuations. They tighten financial conditions across the entire economy. They pressure borrowers. They increase refinancing risk. They squeeze commercial real estate. They stress private credit. They raise funding costs. They expose leverage that only works when money is cheap. The longer rates stay elevated, the tighter that grip becomes.

Yesterday’s CPI report showed inflation running at 4.2%, the highest level in more than three years. Today’s PPI report showed wholesale inflation running at 6.5%, the highest level since late 2022.

Neither report supports the case for imminent rate cuts. Together, they strongly support the opposite conclusion. At a minimum, they reinforce the argument that rates cannot be cut anytime soon without the Fed risking what little inflation-fighting credibility it has left. At the extreme, they strengthen the case that policymakers may eventually have to consider raising rates again.

That is a conversation markets still seem remarkably unwilling to have. Instead, investors continue behaving like a rate-cut rescue package is just one meeting away. Every soft data point gets interpreted as bullish because it means cuts are coming. Every strong data point gets interpreted as bullish because growth is resilient. Somehow every possible outcome leads to the exact same conclusion: buy more stocks.

It’s a fascinating intellectual framework. Unfortunately, inflation data has a nasty habit of ruining good stories. We’re already operating in territory that would have sounded ridiculous a decade ago. Inflation remains far above target. Interest rates are sitting near multi-decade highs. Government debt continues exploding. Asset prices remain historically elevated. Consumers are increasingly stretched. Credit markets are showing signs of strain. Yet markets continue acting as though the return of free money is some sort of natural law.

The reality is that the bill for years of monetary excess — and Janet Yellen’s massive super-genius brainpower — is still arriving.

At her final news conference as Fed chair Wednesday, Yellen said the Fed’s failure to bring inflation up to the central bank’s 2 percent mandate is her single disappointment.

“We have a 2 percent symmetric inflation objective. For a number of years now, inflation has been running under 2 percent, and I consider it an important priority to make sure that inflation doesn’t chronically undershoot our 2 percent objective,” she said.

The unprecedented situation we’re in isn’t stabilizing. It’s becoming more unstable. The vice grip on the economy and financial markets is tightening one data point at a time. The screws turn a little further with every inflation report that refuses to cooperate, every producer-price surprise, every CPI release that reminds everyone that inflation never actually went away—it merely stopped accelerating for a while.

The uncomfortable truth is that policymakers spent years trying to convince everyone there was a painless exit from the biggest monetary experiment in modern history. Now they’re discovering the same thing everyone else eventually discovers and the thing that Austrian economists have been screaming from rooftops: there are no painless exits, only delayed consequences.

Now read:

--

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions.

As of May 20, 2026 I personally no longer actively trade (read my story here). My investing/saving is done by recurring contributions mostly to sector ETFs and a few select equities, trusted third parties who oversee my accounts, and advisors. Such advisors or funds, through individual equities, options, index funds, mutual funds, ETFs, or other securities, may have positions in, exposure to, or holdings of names mentioned herein that I know nothing about. Basically, via index funds, ETFs and individual equities it is possible I could own, have exposure to, or not own anything at any point. As of the same date, May 20, 2026, in an attempt to lead a healthier lifestyle, I’ve also excluded myself from fantasy sports, sports betting, online and in-person casinos and prediction markets.

And all positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

.jpg?branch=production)

{kind=link}

{kind=link}

{kind=link}

{kind=link}