US futures are attempting to bounce back from yesterday’s losses on Wall Street led by Tech. As of 8:00am ET, Nasdaq 100 futures lead the charge, with gains of 0.5% versus 0.1% for the S&P 500 future, although both are off session highs. SpaceX’s post-IPO surge continues, with shares adding another 3% in the pre-market while Mag 7 are mixed: NVDA is up 0.4%, while GOOGL is down 0.5%. The Stoxx 600 is up 0.2%, while the MSCI APAC Index gained 0.5% in mixed trade for regional bourses. Overnight, headlines were largely muted: US retail sales print and earnings from Jabil and CarMax come before the open, but the real action comes later, with attention focused on the Fed and Kevin Warsh's first FOMC meeting as governor. Bond markets have mirrored some of this choppiness with the exception of gilts, which have been boosted by soft UK CPI metrics. US yields are down 1bp across the curve ahead of Kevin Warsh’s debut as FOMC Chair. The dollar is mixed versus peers. The krona is a touch weaker after the Riksbank held rates as expected. Bitcoin is down 1.3%. Commodities are mostly flat to modestly lower: oil prices have been choppy as investors await the formal signing of the US-Iran peace accord on Friday and financial details of the agreement emerge. WTI crude futures are little changed around $76/bbl.

In premarket trading, SpaceX rises 1.9% to eye a fourth straight day of gains, reinforcing the company’s place among the world’s largest after it surpassed Amazon by market value. Nvidia is outperforming Magnificent 7 peers with semiconductor shares set for a rebound (Nvidia +0.2%, Amazon unchanged, Apple -0.1%, Tesla -0.2%, Meta -0.4%, Microsoft -0.4%, Alphabet -0.5%)

- Figma Inc. (FIG) is up 4.2% after Citi initiated coverage of the design software company with a recommendation of buy on expected growth from artificial intelligence demand.

- La-Z-Boy (LZB) jumps 16% after the home furniture store’s reported adjusted earnings per share for the fourth quarter beat the average analyst estimate.

- ResMed (RMD) slips 1% after Morgan Stanley downgraded the stock to equal-weight from overweight, citing lower revenue growth ahead for the maker of breathing machines.

- Rexford Industrial (REXR) is down 1.4% after JPMorgan analyst Michael Mueller cut the recommendation on the real estate investment trust to underweight from neutral, writing that it’s possible the company will see “muted” or even negative growth in 2028 in core funds from operations per share.

In other corporate news, Amazon is said to be facing a possible lawsuit from the US FTC that may lead to billions of dollars in civil penalties, over claims the e-commerce giant misled advertisers. Kuaishou Technology is in discussions with General Atlantic to lead a first round of financing for its video AI arm, Kling AI, ahead of an IPO.

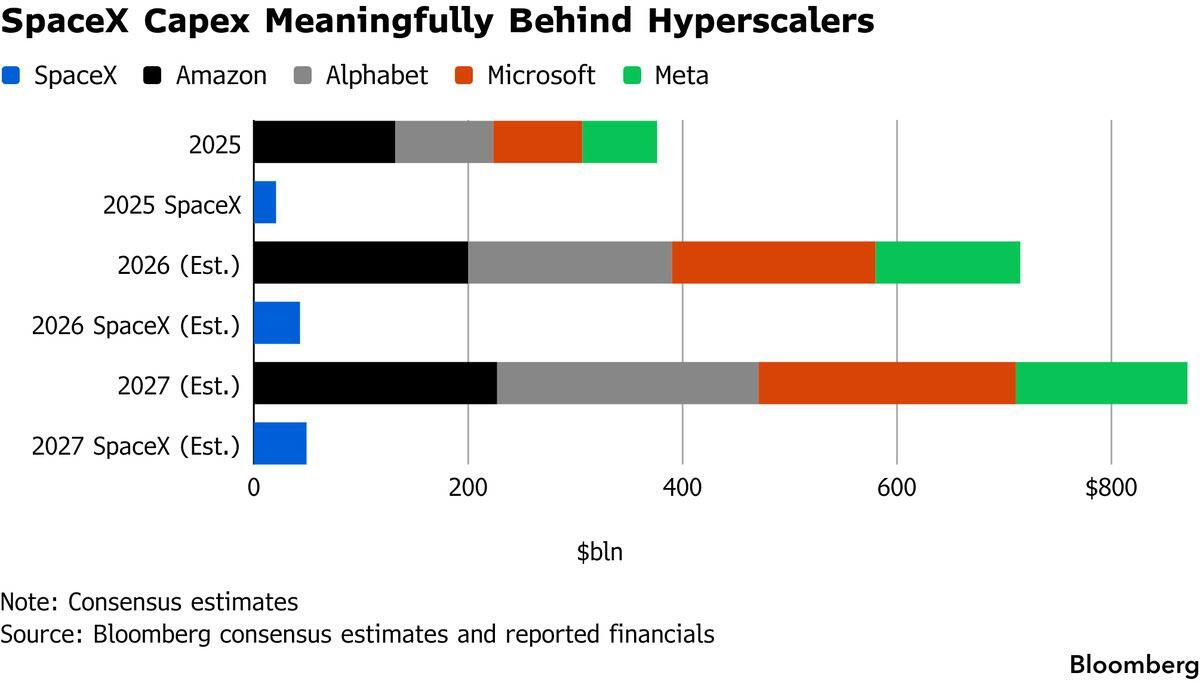

SpaceX shares are poised for a fourth straight day of gains, rising 3.1% in premarket trading. SpaceX may have made headlines for overtaking Amazon’s market cap on Tuesday, but it will take time to catch up on capex spending, or revenue as this Bloomberg chart shows.

Turning to today's main event - Kevin Warsh's first Fed decision - we noted in our FOMC preview that while rates are expected to be left where they are, investors will be looking to see which Warsh shows up for his first press conference as chair: Trump's advocate for lower rates, or the inflation hawk seen around the global financial crisis. The swaps market is not fully pricing in a 25-basis-point hike until March next year, but Warsh is expected to remove the Fed’s “easing bias” today as inflationary pressure builds.

Investors remain divided on the Fed’s next move, with forecasts ranging from rate cuts to multiple increases over the coming year. Oil has slumped on expectations a US-Iran agreement to reopen the Strait of Hormuz will boost supply and ease inflation pressures, prompting investors to reassess the outlook for global interest rates on Fed day. Ahead of the Fed decision, OIS contracts price in around 20bp of tightening by the end of the year. Option traders have been hedging a range of outcomes for Fed policy this year and in early 2027, from cuts to multiple hikes.

“We’re all poised for a hawkish, ready-to-fight inflation Warsh,” Ian Lyngen, head of US rates strategy at BMO Capital Markets, said in an interview with Bloomberg TV. “What happens if he comes out and he’s a lot more dovish?”

JonesTrading chief strategist Mike O’Rourke highlights that two of Warsh’s primary criticisms of the Fed are its expansive balance sheet and over-communication. The communication includes the Summary of Economic Projections, commonly known as the dot plot. “The forecasts are terrible,” notes O’Rourke.

Markets are also watching for changes in Fed communications under Warsh. Bloomberg Economics expects the new chair to forgo submitting his own interest-rate projection to the closely watched dot plot, a break from the practice followed by Jerome Powell, Janet Yellen and Ben Bernanke.

“Warsh faces a formidable challenge, striking a balance between President Trump’s desire for lower rates and signalling to the market that he is a credible and independent Fed chair,” said Bank J Safra Sarasin equity strategist Wolf von Rotberg. “Inflationary pressures in the US are unlikely to abate quickly. Solid growth and elevated core inflation suggest a hawkish bias, regardless of oil prices.”

On the geopolitical front, the US and Iran are preparing to formally sign a memorandum of understanding on June 19 in Switzerland. Still, governments, energy investors and shipping companies remain cautious about how quickly traffic through the Strait of Hormuz can return to normal.

Turning to politics, at the G7 meeting in France, AI is in focus with bosses of OpenAI and Anthropic in attendance. Cut-off to frontier AI models is causing concern, notes Bloomberg Opinion columnist Catherine Thorbecke, highlighting a French presidential candidate calling the move a wake up call, adding that “a nation that depends on others for its technology is a nation that can be unplugged overnight.”

Elsewhere, the IEA said world oil consumption will slump by 1.1 million barrels a day this year, worse than its previous forecast of a decline of about 420,000 a day, the biggest drop since Covid in 2020 amid “higher fuel prices and disruptions to product availability.”

In Europe, the Stoxx 600 is up 0.2%, and holding steady near record highs as investors awaited the Federal Reserve’s rate decision, with German automaker BMW the biggest faller on the Stoxx 600 benchmark after slashing its profitability forecast, weighing on the wider auto subindex. Here are the biggest movers Wednesday:

- Straumann shares jump as much as 11%, the most since October, after the Swiss dental implant maker increased its profitability guidance for the year. Analysts were upbeat on the magnitude of the outlook boost

- Aixtron shares rise as much as 5.8% after JPMorgan analysts raised their estimates for the German semiconductor equipment supplier and set a new Street-high price target for the stock

- PZ Cussons climbs as much as 9.9%, to the highest since September 2024, after the personal care products maker said full-year adjusted operating profit should come in at, or slightly above, the upper end of the previously guided range

- BFF Bank shares rise as much as 13% in Milan trading, the most since May 12, after Italian newspaper MF reported that Banco BPM and Amco may be considering an offer for the bank, without citing sources

- Lenzing advances as much as 12%, the most since August, after Berenberg turns positive on the textile producer for the first time in almost nine years, upgrading to buy from hold to reflect an improvement in pricing

- BMW shares fall as much as 12% after the German carmaker slashed its profitability forecast and ramped up its cost-cutting program, flagging worsening demand in China and negative sentiment from the war in the Middle East.

- Orange shares slip as much as 4.1% to the lowest since March after Barclays reinstated coverage with an equal-weight rating, saying upside value from the recent SFR deal is already caputred in valuation

- Zealand Pharma falls as much as 8.1% after Berenberg cut its recommendation to hold from buy, saying unlocking upside will now take longer than previously anticipated

- Silex Microsystems falls as much as 20% after several brokers initiated coverage of the Stockholm-listed specialist microchip maker that debuted on May 7. SEB starts coverage with a sell rating, saying it’s too richly valued

- Medincell shares slump as much as 16%, the most since April 2022, after the French biopharma company reported full-year revenue that analysts said was weaker than expected

Asian stocks advanced for a fourth straight day as investors awaited the Federal Reserve’s first policy decision under new chairman Kevin Warsh. The MSCI Asia Pacific Index rose 0.5%, erasing similar losses from earlier in the session. South Korea’s Kospi led regional gains as shares of memory chipmaker SK Hynix Inc. hit a record high. The Fed decision will cap a week of major central bank meetings, after the Bank of Japan raised interest rates and the Reserve Bank of Australia left policy unchanged, both in line with forecasts. Here Are the Most Notable Movers

- Tamron shares surged 24% to a record after the camera lens maker announced an unexpected mid-term plan and a significant expansion of shareholder returns.

- Kuaishou Technology shares gain 7.3% on optimism over Chinese AI firms and news that the company is in talks with General Atlantic for the first-round financing of its video unit Kuaishou Kling.

- SK Hynix shares gain as much as 5.7% to a record after Korea Economic Daily reported the memory chipmaker is preparing a shareholder return policy worth up to 100t won this year.

- Fila SpA has sold 4.25 million shares of DOMS Industries Ltd. for 2,200 rupees each, according to terms of the deal seen by Bloomberg News.

- Chinese printed circuit board supply chain stocks extended their climb after a report that a major upstream supplier plans to raise prices. Senasic Electronics Technology shares soar as much as 100% in their Hong Kong trading debut on Wednesday.

- Merdeka Gold Resources shares rise as much as 3.2% in Jakarta trading after the Indonesian miner offered 89.7 million HDRs at up to HK$26.60 each in its Hong Kong listing.

- Kingboard Holdings shares surge 17.7% after a unit agreed to sell 155 million shares of Kingboard Laminates for HK$76 per share through a block trade agreement.

- Senasic Electronics Technology shares more than doubled in their Hong Kong trading debut on Wednesday.

In FX, the dollar is mixed versus peers. The krona is a touch weaker after the Riksbank held rates as expected.

In rates, treasuries are marginally richer across the curve, following steady price action in oil and supported by wider gains across gilts, which outperform after UK headline and core inflation figures rose less than expected in May. Treasury yields remain within 1bp of Tuesday’s closing levels, the 10-year around 4.435%, with UK counterpart outperforming by 4bp; following UK CPI data, 10-year gilt yield dropped to a two-month low 4.734% as BOE rate-hike pricing for this year eased slightly. Focal point of US session is first FOMC decision of Chairman Kevin Warsh’s tenure, expected to hold rates steady. Treasury auctions resume Thursday with $24 billion 5-year TIPS reopening; demand was strong for Tuesday’s 20-year sale

In commodities, WTI futures are up around 0.6% after rebounding from a fresh three-month low in anticipation of a US-Iran deal signing. Bitcoin is down 1.3%.

Today's US economic data calendar includes May retail sales (8:30am) and April business inventories and May pending home sales (10am)

Market Snapshot

Top Overnight News

- Brent held below $80 as traders bet a US-Iran deal due to be signed Friday will reopen the Strait of Hormuz, restore Iranian oil exports and give Tehran access to a $300 billion development program. BBG

- The Trump administration’s emerging nuclear deal with Iran risks securing fewer restrictions than the deal negotiated by the Obama administration — one he derided and later scrapped. BBG

- As the world awaits the full reopening of the Strait of Hormuz following the signing of an interim peace deal between Iran and the US, the United Arab Emirates is working on a highly ambitious plan to try to end its dependence on the critical chokepoint. BBG

- G7 leaders agreed to tighten sanctions on Russia’s oil and gas industry and boost military support for Ukraine. The summit’s final day turns to AI, with OpenAI and Anthropic execs attending. BBG

- Senior Trump administration officials had weighed how to structure potential government equity stakes in major AI companies before the government’s export controls on Anthropic further roiled the industry. Semafor

- US President Trump's administration considered requiring Anthropic to obtain government approval before allowing foreign nationals access to its most advanced AI models, as officials weigh new export control measures for AI tech.

- FOMC Preview: The most important change in the economic data since the last FOMC meeting is the impressive pick-up in job growth that has put the labor market on a sturdier trajectory. This has left the focus on whether the inflation situation is becoming concerning enough to warrant a rate hike. The war and the increase in oil prices will likely drive headline PCE inflation above 4% and leave core PCE inflation above 3% all year. But so far the impact on inflation looks more like the usual passthrough from large oil shocks than the pandemic’s wide-ranging shortages and price spikes. Link

- UK inflation held at 2.8% in May, unchanged from April's 13-month low and below forecasts from both economists and the Bank of England, official figures showed on Wednesday, a day before the central bank's next interest rate decision. BoE expected to keep interest rates on hold at 3.75% on Thursday. RTRS

- Sweden’s Riksbank assesses that it is well-balanced to leave the policy rate unchanged at 1.75 per cent now, but the probability that the rate will be raised later this year has increased in relation to the assessment in March. Riksbank

- Convertible bond issuance surges as companies rush to raise as much money as possible to fund their AI ambitions. WSJ

Middle East News

- An informed source told Tasnim that Bloomberg's alleged text about the US-Iran MoU is not accurate, adding that the text of the memorandum, based on the agreement of the parties, will not be published after it is signed on Friday. However, this was later corrected, stating that the text will be released after the signing on Friday.

- US Defence Secretary Hegseth and CIA Director Ratcliffe were among the “most pessimistic” about whether the Iranians would honour their commitments to make substantive concessions on their nuclear program, according to CNN.

- A US senior official was said to have dismissed as "preposterous", the reports of side deals in which Gulf states such as the UAE and Qatar could unfreeze Iranian funds they hold, according to Axios.

- The US Senate voted 48-47 to narrowly block a new bid to rein in Trump's war powers.

- Trump administration officials were reported to be discussing ideas to kick-start oil tanker traffic through the Strait of Hormuz, including offering a fee-based “VIP pass” naval escort through the waterway, according to people familiar with the discussions cited by POLITICO.

- US officials told a CNN reporter that Iran's Supreme Leader has given his tacit approval of the MOU, and that there are internal discussions over whether he could issue a statement ahead of Friday's formal signing ceremony in Switzerland. It was separately reported that US officials downplayed the Iran agreement texts and said that the text omits key back-channel commitments, according to CNN.

- Israeli artillery shelling reported in southern Lebanon, according to SNN.

- Al Jazeera correspondent reported that 10 rockets were fired towards Israeli forces in the vicinity of Kfar Tebnit town in the Nabatieh district of southern Lebanon.

A more detailed look at global markets courtesy of Newquawk

APAC stocks ultimately traded mixed, albeit at an improvement from the initial losses seen following the subdued lead from Wall St, where most major indices finished in the red amid renewed tech selling. ASX 200 shrugged off early weakness and edged mild gains with upside led by mining, materials and tech, although further upside in the index is capped by losses in energy and the defensive sectors. Nikkei 225 clawed back initial losses and printed a fresh all-time high after briefly topping the 70,000 level. Hang Seng and Shanghai Comp lagged amid losses in auto names and aluminium producers, while they also failed to benefit from a report that the US delayed blacklisting China's DeepSeek and over 100 Chinese firms deemed national security risks. There was also little reaction seen to the PBoC's announcement to add overnight reverse repo instruments and to increase overnight reverse repo operations, as it seeks to improve the efficiency of interest rate transmission.

Top Asian News

- PBoC Governor Pan said they will allow overseas institutions to access yuan liquidity and will add overnight reverse repo instruments at the appropriate time, while he added they will increase overnight reverse repo operations and improve the efficiency of interest rate transmission. Pan also stated that six banks are authorised to conduct offshore foreign exchange transactions in the Shanghai Free Trade Zone, and commented that it is difficult and unnecessary for China's credit growth to maintain its previous pace.

- PBoC announces an adjustment to the temporary overnight reverse repurchase and outright repurchase agreement time which is to be set between 15:00-15:30 local time (08:00-08:30BST/03:00-03:30EDT). PBoC seeks to ensure flexible and efficient use of temporary overnight reverse and outright repurchase agreements in the open market. Furthermore, PBoC said operating rates will be set at the 7-day reverse repurchase rate in the open market minus 25bps and plus 25bps, respectively, and that it will act when the money market overnight rate remains consistently below or above the respective operation rates of the tools.

- Chinese Vice Premier He Lifeng said they will step up financial supervision and will vigorously and orderly advance resolution of local government debt, while He added they will issue CNY 300bln special bonds to replenish the capital of financial institutions and that the financial sector will be opened up further.

- China's financial regulator said they will increase regulatory cooperation in emerging areas and will strengthen efforts to avert systemic financial risks. The regulator will also strictly curb unlawful financial activities and address risks in small and medium-sized financial institutions effectively and orderly, while China is to steer financial resources towards emerging and future industries.

- Senior leaders of Japan's ruling party said to have proposed cutting the consumption tax on food to 1% from April 2027 for a two-year period.

European bourses (STOXX 600 +0.3%) start Wednesday's trade mixed, with outperformance in the AEX (+0.7%) while the DAX 40 (-0.2%) lags after BMW cut guidance. Geopolitical newsflow has been light thus far as markets await for the official MoU signing on Friday.

European sectors also lack a clear bias. Technology (+1.2%) and Banks (+0.8%) top the sector pile. Autos (-2.1%) is the worst-performing sector this morning, primarily driven by updated guidance from BMW. The Co. cut its operating auto margin to 1-3% (prev. 4-6%) and said it would intensify cost-cutting, with a negative one-off in the H2'26. Analysts at Deutsche Bank and Jefferies both said the outlook cut was significantly larger than expected, which has resulted in the Co.'s shares slumping as much as 11%. This has dragged peers lower with it (Volkswagen -2.4%, Mercedes-Benz -3.0%)

Top European News

- UK Inflation Rate YoY (May) Y/Y 2.8% vs. Exp. 3% (Prev. 2.8%); Services 3.7% (exp. 3.7%, prev. 3.2%).

- UK Inflation Rate MoM (May) M/M 0.2% (Prev. 0.7%).

- UK Core Inflation Rate YoY (May) Y/Y 2.6% vs. Exp. 2.7% (Prev. 2.5%, Low. 2.6%, High. 3.0%).

- UK Core Inflation Rate MoM (May) M/M 0.3% (Prev. 0.7%).

- EU Inflation Rate YoY Final (May) Y/Y 3.2% vs. Exp. 3.2% (Prev. 3%, Low. 3.2%, High. 3.2%).

- EU Inflation Rate MoM Final (May) M/M 0.1% vs. Exp. 0.1% (Prev. 1%, Low. 0.1%, High. 0.1%).

- EU Core Inflation Rate YoY Final (May) Y/Y 2.6% vs. Exp. 2.5% (Prev. 2.2%).

- ECB Wage Tracker: 2026 Quarterly +2.604% (prev. +2.597% Y/Y); Annual +2.281% (prev. +3.193%).

FX

- DXY is on a modestly firmer footing after softening on Monday alongside a decline in yields and lower oil prices. Focus today is overwhelmingly on Warsh’s first FOMC meeting as chair, where the committee is widely expected to keep the federal funds rate unchanged at 3.50-3.75%. Within the meeting, attention will be on language surrounding the easing bias, and the dot plots, which ING believes a removal of the bias alongside a cut to the 2026 dot plot, would support the Buck. Alongside these points, Warsh’s communication will be closely monitored. (Full Fed preview in the Newsquawk Research suite). DXY lacks direction, trading unchanged and supported just above 99.50.

- GBP is a touch lower. In short, a cooler than expected UK CPI print, which falls beneath BoE forecasts on both a headline and core basis, services were also cooler than BoE forecast, but in line/hotter than analyst forecasts, depending on which data vendor is cited. GBP weakened post-data; Cable fell as much as 20 pips to a 1.3408 trough before paring modestly. The pair dipped below its 200DMA at 1.3418.

- Two-way action seen in SEK, which is modestly softer post-announcement despite the forecasts implying a greater chance of a 2026 hike. Pressure that is a function of the fact that the forecasts and statement are based on information up to the 11th of June, as such the fall in energy benchmarks seen in the last few sessions on the US-Iran MOU progress is not accounted for, and therefore the hawkish tilt to the policy forecast is likely to be unwound in the next meeting, if the MOU holds and the energy retreat sticks and/or extends. We may get more details from Governor Thedeen at 10:00BST, and the Minutes on the 24th of June.

Fixed Income

- Global fixed benchmarks are mixed, with USTs a couple of ticks lower whilst Bunds and Gilts gain; the latter outperforms after the UK’s inflation held steady in May. Geopolitical updates have been lacking today, with all eyes on the US-Iran deal signing on Friday. However, Iran’s Tasnim, citing a source, suggested that the text will not be published after the signing on Friday. Though, this was later corrected and it will be released.

- USTs (-2 ticks) hold within a 109-26+ to 109-30+ range. Markets are ultimately on tenterhooks ahead of the Fed policy announcement, which will see the debut of Kevin Warsh as Chair. Policy rates are expected to remain unchanged, so focus will be on whether the easing bias will be removed from the statement. Dot plots are seen to show higher inflation and a more cautious policy path, with the new Chair interestingly not expected to publish a personal dot plot. At the presser, traders will eye whether he attempts to push a dovish agenda and how he contrasts to his fellow board members. From a yield point, Warsh will be eyed for any hints to his thinking on the Fed balance sheet; should markets be guided to faster unwinding of the Fed’s balance sheet, a steeper curve could be expected.

- Bunds (+20 ticks) trade firmer this morning, continuing recent price action. Domestically, the release of the ECB Wage Tracker had little impact on German paper, where the 2026 quarterly figure rose slightly from the prior. Focus ahead turns to the EZ Final Inflation metrics for May, which are expected to remain unrevised. From a yield perspective, the German 10yr has now slipped below the 3.00% mark (current 2.93%), and now approaching levels not seen since early April.

- Gilts (+57 ticks) outperform vs peers following the region’s inflation report. In brief, a cooler-than-expected print on both a headline and core basis. A series that reduces the odds of a hawkish surprise at the June BoE. However, the as-expected/slightly-hotter (depending on the consensus provider) services figure will be a point of concern for policymakers and may well be enough to keep some dissenters in play, even given the significant energy benchmark moderation in recent days. The report will not have any impact on the policy decision at Thursday's meeting (BoE to hold), but could push the vote split a bit more dovish vs consensus; analysts saw a range between 8-1 to 6-3 before the inflation print and recent energy moderation on US-Iran progress.

- Germany sells EUR 2.107bln vs exp. EUR 2.5bln 3.40% 2047 and 1.80% 2053 Bund.

- Australia sells AUD 300mln 4.75% June 2054 bonds b/c 2.46, avg yield 5.3040%.

Commodities

- Crude futures are essentially incrementally firmer, hovering at 3-month lows, as markets await the US-Iran MoU signing in Switzerland. Details of the deal remain light; however, Reuters did shine some light on a point of the draft MoU: the rehabilitation and economic development of Iran. The report stated that a USD 300bln private fund is being designed to trigger investment into Iran. The report added that commitments have already exceeded USD 150bln across 5 regions, while the fund will not contain US government money or grants.

- Energy benchmarks are relatively contained. WTI Aug'26 oscillates in a USD 74.09-76.06 range while Brent Aug'26 rotates in a 77.75-79.57/bbl band.

- Spot gold has come off slightly ahead of the FOMC meeting, in which a hold is expected. Focus will lie in the press conference, in which Fed Chair Warsh is delivering his first post-policy conference in his new role. The yellow metal currently trades at the lower end of its narrow USD 4318-4350/oz range.

- 3M LME Copper flips either side of the USD 13.8k/t handle as market risk is subdued.

- US Private Inventory Data (bbls): Crude -8.3mln (exp. -4.5mln), Distillates -0.5mln (exp. -0.2mln), Gasoline +2.5mln (exp. -1.4mln), Cushing -1.5mln.

- IEA OMR (Jun): World oil demand falling by 1.1mln BPD in 2026 on the Iran War (prev. forecast 420k BPD fall); sees total world oil supply 920k BPD lower than demand in 2026 (prev. forecast 1.7mln BPD lower).

- TotalEnergies (TTE FP) says its Saudi Arabian refinery was hit by three drones but is still only running at 70% and "probably" will not be repaired until early 2027.

- Tanker Trackers reported that two Iranian supertankers carrying a total of 3.8mln barrels of crude oil passed through the US blockade.

- Two US Senate Democrats are calling for US Energy Secretary Wright to abandon efforts to build a West Coast SPR, CNN reported. Democrats warned that establishing it this fiscal year would flout the law and usurp congressional authority.

Trade/Tariffs

- The US delayed the blacklisting of China's DeepSeek and over 100 Chinese firms deemed national security risks, to avoid escalating tensions with Beijing, according to sources cited by Reuters.

US Event Calendar

- 7:00 am: Jun 12 MBA Mortgage Applications, prior 10.8%

- 8:30 am: May Retail Sales Advance MoM, est. 0.55%, prior 0.5%

- 8:30 am: May Retail Sales Ex Auto MoM, est. 0.6%, prior 0.7%

- 10:00 am: May Pending Home Sales MoM, est. 0.9%, prior 1.4%

- 2:00 pm: Jun 17 FOMC Rate Decision; est. 3.75%, prior 3.75%

DB's Jim Reid concludes the overnight wrap

It’s set to be a long day: I was up just before 4am to drop my daughter off for a three-day school trip to Disneyland Paris, and will be up late tonight for England’s first World Cup game while also keeping an eye on the outcome of Fed Chair Warsh’s first FOMC meeting. When I was at school, we had a one-day trip to Thorpe Park, a theme park just three miles away. I vividly remember that it cost £4 to get in. The trip to Disneyland Paris is costing me a little more than that! How things have changed.

Thankfully we can park the rollercoaster market analogies at the moment as relative calm has broken out in markets since the war in the Middle East is now seemingly over. The latest overnight was a reported 14-point US–Iran peace framework (reported by Bloomberg) outlining a broad de-escalation package centred on a permanent ceasefire, the lifting of the US naval blockade and the reopening of the Strait of Hormuz with traffic targeted to return to pre-war levels within ~30 days. Crucially, the draft includes immediate waivers for Iranian oil and petrochemical exports upon signing, alongside a broader package of financial incentives including access to frozen assets (timing unspecified) and a ~$300bn externally financed development plan. In return, Iran reiterates its commitment not to pursue nuclear weapons and to neutralise enriched material, with core nuclear constraints deferred to a 60-day second phase of negotiations. Importantly, the benefits appear conditional on compliance, and much of the detail remains fluid ahead of formal signing, underscoring that this is still a high-level MoU rather than a final settlement. The plan is for it to be signed in Switzerland on Friday.

Oil continues to edge lower overnight (Brent -0.42% to $78.61/bbl) after a big fall yesterday with Asian equities relatively quiet. Across the region, the Nikkei (+0.92%) and KOSPI (+0.83%) continue to perform well even with a setback in US tech yesterday that we'll discuss below. The ASX (+0.50%) is also higher with mainland Chinese equities broadly flat and the Hang Seng (-0.37%) slightly lower. S&P 500 (+0.25%) and Nasdaq futures (+0.54%) are bouncing back after a tougher day for US tech on Tuesday.

Ahead of those overnight moves, global markets had mostly put in another decent performance yesterday although a slump in chipmakers weighed on US equities. The main global catalyst was the US-Iran headlines, with Brent crude (-5.06%) posting a fourth consecutive decline as the two sides prepared to sign the memorandum of understanding this Friday. Indeed, Brent hit a three-month low of $78.43/bbl, which in turn has seen investors increasingly price out the chance of stagflation this year. Indeed we saw rising evidence of the US easing its blockade yesterday with Iranian tankers sailing through it with active location trackers for the first time since April.

That fall in oil prices led to a fresh boost for markets, particularly for European assets which are more exposed to the energy shock. So yesterday saw the STOXX 600 (+0.25%) and Italy’s FTSE MIB (+1.15%) hit another record high, alongside gains for the FTSE 100 (+0.61%) as well.

But for US equities there was a more divergent performance, as weakness among chip stocks dragged on both the S&P 500 (-0.57%) and the Nasdaq (-1.15%). Continued volatility for chipmakers saw the Philly semiconductor index slump by -5.71% from its record high the previous day, after rising by +15.5% after the three previous sessions. Aside from that though, there were some stronger moves, with most S&P 500 constituents higher on the day and the KBW Banks index (+1.64%) up to a new record.

Meanwhile, bonds rallied as investors became increasingly optimistic on the near-term inflation profile. The US 1yr inflation swap fell -9.5bps to 2.57%, its lowest since February 27, the day before the strikes against Iran began. And the 1yr Euro inflation swap (-10.0bps) fell to a three-month low of 2.61%, having been above 3.8% less than a month earlier. So that supported bonds on both sides of the Atlantic. In the US, the 2yr Treasury yield (-1.4bps) was down slightly to 4.05%, whilst the 10yr yield (-3.5bps) saw a bigger decline to 4.44%. European sovereigns saw similar moves, with yields on 10yr bunds (-2.5bps), OATs (-3.6bps) and BTPs (-4.1bps) all moving lower.

Nevertheless, even as oil prices have come down again, there were still warnings about the inflation shock. For instance, ECB chief economist Philip Lane warned that inflation was still in the pipeline, given “four months of elevated energy prices”. He also warned that “There’s going to be indirect effects on food, on goods, on services this year and into next year.” So even with oil prices coming down again, markets are still fully pricing in a second ECB hike before the end of the year, following on from last week’s move.

Speaking of central banks, attention today will be firmly on the Federal Reserve’s decision, which is the first with Kevin Warsh as the new Chair. They’re widely expected to keep rates on hold, but a new Chair often leads to higher volatility at first, because the market is trying to work out their communication style and reaction function. So it could still be an eventful one, even without a change in rates. In terms of what to expect, our US economists think the statement will drop the easing bias from last time, and expect the median dot will no longer signal a rate cut this year, as the last one did in March. Based on prior comments, they think Warsh is likely to avoid forward guidance and an overreliance on short-term data trends. And they also see him tacking towards the centre of the committee, so not arguing for near-term rate cuts, but not taking rate hikes off the table either. For more details, see the full preview here from our US economists.

In terms of the latest market expectations on the Fed, fed funds futures are pricing 21bps of hikes by year-end, with this pricing actually rising +1.3bps yesterday despite the broader rates rally as expectations for any dovish rhetoric from Warsh appear to have eased.

In other news, the European Parliament voted in favour of the EU trade deal with the US agreed last year, by a 440-151 margin. Although the deal was initially reached last summer, there had been several delays to the ratification process, including earlier this year when Trump was threatening to annex Greenland.

Finally, there were a few data releases yesterday, including the ZEW survey from Germany. That showed the expectations measure rising more than expected to 10.5 in June (vs. -5.5 expected), a 4-month high. However, the current situation measure fell more than expected to a 6-month low of -81.0 (vs. -78.0 expected). Then in the US, housing starts saw an unexpectedly big drop in May, falling to an annualised pace of 1.177m (vs. 1.430m expected), which was the lowest since May 2020 during the pandemic.

Overnight in Asia, Japan’s trade deficit narrowed unexpectedly to ¥378.7bn in May (vs. ¥547.6bn expected), supported by robust export growth of +17% year-on-year on strong demand from the US and China. Imports also rose (+12.5% y/y) but came in slightly below expectations. Meanwhile, April’s trade surplus was revised down to ¥299.3bn.

Looking at the day ahead, the main highlight today will be the Federal Reserve decision, along with Chair Warsh’s subsequent press conference. We’ll also hear from the ECB’s Sleijpen. Otherwise, we’ll get the UK CPI release for May, along with US retail sales and pending home sales for May.

.png?branch=production)

.jpg?branch=production)

{kind=link}

{kind=link}

{kind=link}