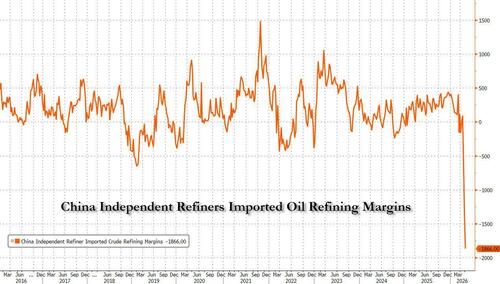

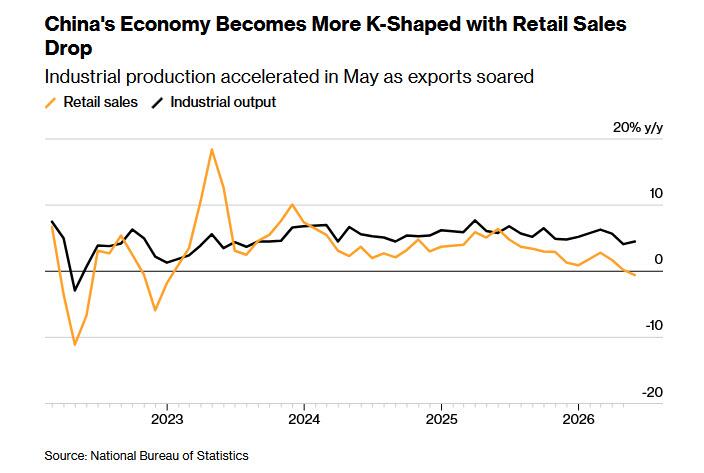

Last week we showed four China-linked charts which made it very clear that, laughable flatlined 5% GDP notwithstanding, China's economy appears to be on the verge of yet another collapse (explaining the unprecedented drop in both Chinese oil imports and refining output): between autos, real estate, banks and overall consumption, the economy - as seen by the market - was in freefall.

China is fine pic.twitter.com/PFJzVCz9Ba

— zerohedge (@zerohedge) June 26, 2026

With sentiment collapsing, and amid growing speculation that Beijing will have no choice but to unleash another firehose of fiscal and monetary stimulus, it came as little surprise overnight when China’s central bank set the interest rate on its new overnight liquidity tool at a level that was below expectations, in what some economists see as a de facto rate cut that could push down market borrowing costs.

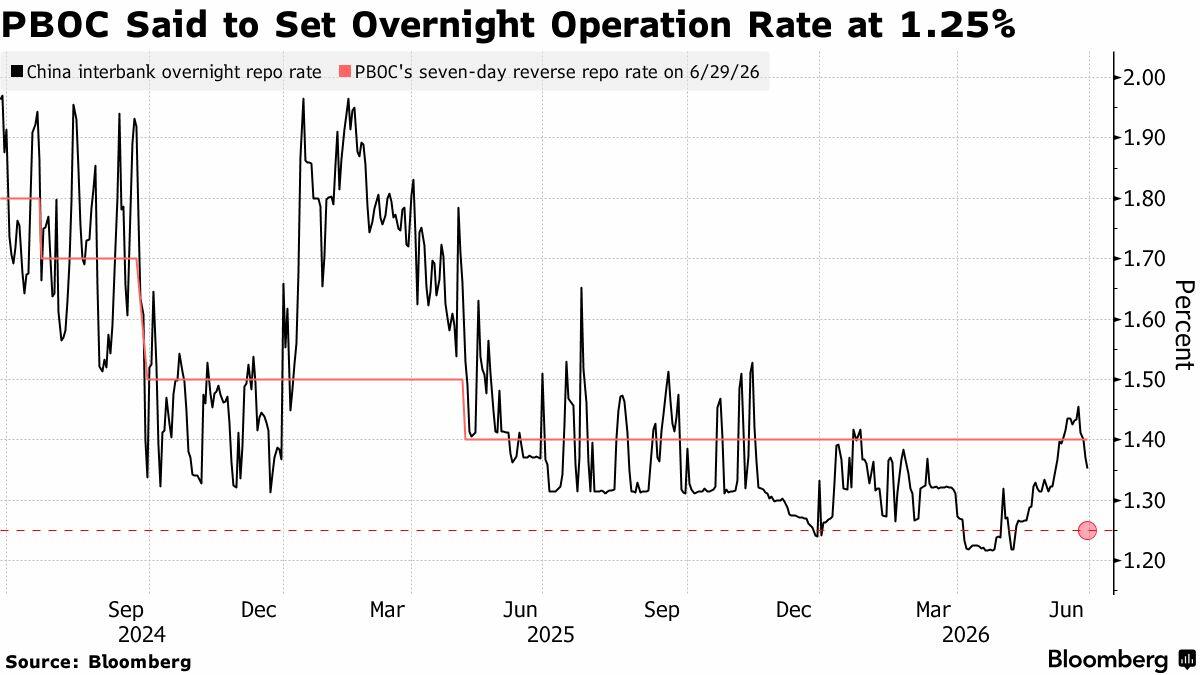

As Bloomberg reports, the People’s Bank of China said it conducted 300 billion yuan ($44 billion) of overnight reverse repo agreements in open market operations on Monday, according to a statement that didn’t disclose the rate of interest it charged on its new instrument. To avoid confusion, readers should always remember that a reverse repo in China is a repo in the US. And vice versa. The central bank uses the operation to funnel short-term funds to the market to influence borrowing costs, and it accepts eligible bonds as collateral.

The official rate of the facility - the first such overnight facility unlike the bank's traditional 7-day operations - came in at 1.25%, Reuters reported. Unlike other liquidity instruments, the PBOC did not announce the borrowing cost for the overnight reverse repos. That compared with the median forecast of 1.35% in a Bloomberg survey.

The PBOC’s benchmark remained at 1.4%, 15bps higher than the facility rate, as it provided 157.5 billion yuan of seven-day reverse repo.

The decision, which intentionally came in below well telegraphed estimates, now sets the stage for looser monetary policy including a possible cut in loan prime rates — China’s lending benchmarks — as early as next month, according to Citigroup and Standard Chartered.

"Today’s move is not an outright easing, in our view — but it likely opens the door to one,” Citigroup economists led by Xiangrong Yu said in a note. “The asymmetric move likely signals an easing bias, without a formal cut.”

That will come next.

The operation marked the first time that the PBOC deployed the tool to manage liquidity, and many traders said the move is a first step in a gradual shift toward a benchmark overnight rate. Such a transition is likely to bring China closer to the practice of its global peers such as the Federal Reserve, which relies heavily on its overnight target rate to manage the US economy.

“The People’s Bank of China appeared to signal that it wants borrowing costs to fall by setting the rate on its new overnight reverse repo 10 basis points lower than markets had expected. This backs our view that the PBOC will trim its policy rate to reduce financial burdens on businesses and households and support demand”, said Bloomberg's David Qu.

The new facility is expected to give the PBOC better control over short-end borrowing costs and allow it to smooth out any big swings in market liquidity. The cost of overnight borrowing in the interbank market has become more volatile since May, as the central bank sought to ease a glut of money in the financial system, with demand for cash typically rising at the end of each quarter.

The yield on China’s 10-year government bonds slipped one basis point to 1.71% after the announcement, extending its drop into a third session. Both the overnight and seven-day repo rates eased.

Still, despite the strong hint of easing policy, some analysts still believe the PBOC will be looking to maintain the policy status quo, for now, by keeping the seven-day benchmark steady while publicly omitting details about the new overnight rate.

“The overnight reverse repo is primarily a liquidity tool aimed at smoothing seasonal funding stress, rather than a tool to signal a particular policy stance,” said Frances Cheung, head of foreign exchange and rates strategy at Oversea-Chinese Banking Corp. “The timing of the operations today and tomorrow ahead of the half-year end — and the amount bigger than the seven-day reverse repo — both support this notion.”

Talk of a rate cut in China gained substantial traction as the Chinese economy slowed dramatically in the second quarter, with retail sales and investment falling at a pace unseen since the pandemic.

Still, most economists expect the PBOC to keep its policy rate unchanged throughout 2026, although Huang Yiping, an adviser to the central bank, said a rate cut still remains a possibility.

“The next step is to lower de facto lending rates, including a possible reduction of LPR rates” across both one- and five-year durations “to support a stabilization of credit growth,” said Becky Liu, head of Greater China macro strategy at Standard Chartered.

“We had long argued that China is firmly staying on an easing path, and will likely to take advantage of the interest rate framework reform to lower de facto rates,” she said.

Lynn Song, China economist at ING, said it’s possible the new rate may have been kept undisclosed to avoid “diluting” the significance of the seven-day benchmark.

“Given the overnight rate is still the most liquid and important rate for trading activity, it makes sense this will eventually be the level that policymakers seek to control,” Song said. “However, it probably will take some time. We probably need some track record and maturity for the overnight repo facility and how it affects market overnight rates before this shift is made.”

.jpg?branch=production)

.jpg?branch=production)

{kind=link}

{kind=link}