Authored by Antonio Graceffo via The Epoch Times,

Despite sanctions and two wars, the yuan is losing ground, with much of its earlier rise tied to Russia and now reversing.

The Kremlin drafted a memo this year outlining seven areas of potential economic convergence with Washington, including a proposed return to dollar settlement for Russian energy transactions. The stated rationale in the memo is that dollar integration would stabilize Russia’s balance of payments and foreign exchange markets. Russia never actually wanted to transact business in yuan. Moscow only did so because it was cut off from the dollar system by sanctions and had no choice.

The yuan was a fallback, not a preference. Russia’s desire to return to a dollar-denominated trade regimen is an implicit admission that the yuan-based arrangement failed to deliver monetary stability. It also demonstrates Russian President Vladimir Putin’s desire to decrease Russia’s dependence on China. Putin has many ambitions for Russia’s future, but among them is not for Russia to be the No. 2 power in a Beijing-centered world order.

Heading into the U.S.–Iran conflict, many pundits believed it would bring about the demise of the dollar while accelerating the internationalization of the yuan.

Bloomberg ran a piece titled “The Iran War Is China’s Global Payments Debut,” arguing it took four years of preparation after Ukraine, and this war, to make the yuan a serious contender.

The South China Morning Post cited analysts saying disruptions from the war could accelerate a shift in oil trade and threaten the dollar’s long-held dominance.

Deutsche Bank’s FX Managing Director Mallika Sachdeva wrote in March that the Iran war could be remembered as a catalyst for “erosion in petrodollar dominance, and the beginnings of the petroyuan.”

However, none of these predictions came true.

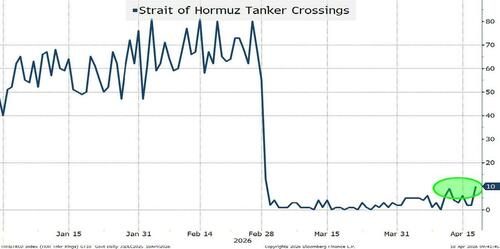

In fact, the Iranian Embassy in Zimbabwe posted that it was time to add the “petroyuan” to the global oil market, and Iran demanded that tankers be allowed passage only if trade was denominated in yuan.

But to date, the only confirmation is from Lloyd’s List that two ships paid a toll, and there is no clear evidence that the toll was paid in yuan. Lloyd’s List has also not released the names of the ships; therefore, they may very well have been Chinese-flagged vessels that paid a toll, allowing China to claim that de-dollarization was underway.

The logic behind their belief that dollar dominance would be damaged by this conflict was that the United States used sanctions and dollar-system exclusion as a primary weapon against Iran, just as it did against Russia. Every time Washington weaponizes the dollar, it gives non-Western countries an incentive to build off-ramps. Iran, China, and Russia all have a motive to route energy trade outside SWIFT and dollar settlement.

A major U.S. military and financial confrontation with Iran could have been expected to accelerate that, pushing Iranian oil sales into yuan, deepening CIPS usage, and giving China a showcase for an alternative system. However, the data shows the opposite. The dollar has lost no ground, and the yuan has made no gains. If Russia re-dollarizes, the yuan will lose much of its already small share of global trade.

The yuan’s global footprint does not support the internationalization narrative that Russia’s sanctions-driven shift was used to bolster. IMF COFER data for Q3 2025 put the yuan’s share of global foreign exchange reserves at 1.93 percent, down from 1.99 percent in the prior quarter, compared to the dollar’s 56.92 percent. The SWIFT November 2025 RMB Tracker recorded the yuan’s share of global payments at 2.94 percent, falling to 2.71 percent in February 2026.

Between 2020 and 2024, the yuan’s share of global trade settlement roughly doubled, rising from around 2 percent to a peak of 4.7 percent, according to SWIFT RMB Tracker data. That headline gain drove widespread claims that the yuan was displacing the dollar as the world’s trading currency. The reality is more complicated.

To understand how much of that gain was genuine organic growth versus a single sanctions-driven relationship, it is possible to estimate the dollar amounts involved. Global merchandise trade ran from approximately $17.6 trillion in 2020 to $24.4 trillion in 2024, meaning total yuan-settled trade grew from roughly $350 billion to $1.15 trillion, an increase of approximately $800 billion.

Over the same period, Russia–China bilateral trade grew from around $117 billion to $245 billion, with yuan settlement going from near zero before the 2022 invasion of Ukraine to roughly 60 percent of bilateral trade by 2024, a gain of approximately $145 billion in yuan-settled flows. That one corridor, therefore, accounts for an estimated 15 to 20 percent of the entire global increase in yuan trade settlement.

If Russia shifts back to the dollar, the yuan will lose part of its current 2.71 percent share of global trade settlement. In short, the yuan is not gaining internationalization, the dollar is not losing ground, and even two parallel wars, one in Ukraine and one in Iran, have not been sufficient to accelerate the yuan’s adoption as an international trade currency.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

.png?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

{kind=link}