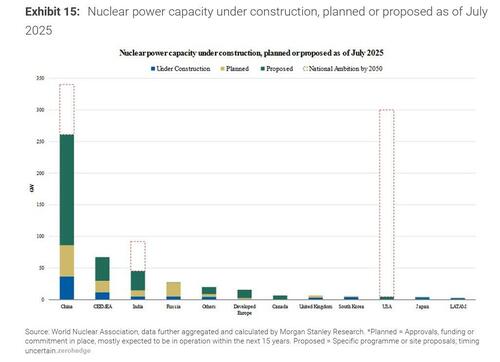

Barclays is out with a report on nuclear and how the industry is progressing from conviction to construction. The report highlights year-to-date regulatory developments, demand and execution signals and market pricing across the industry.

Last year, Barclays argued three core points regarding nuclear energy:

- A nuclear renaissance is underway driven by energy security, decarbonization, and AI power demand

- The nuclear fuel cycle is likely to be an upstream bottleneck that requires reshoring

- As the theme matures, practical hurdles will take center stage, such as speed to power, labor, permitting, and unit economics

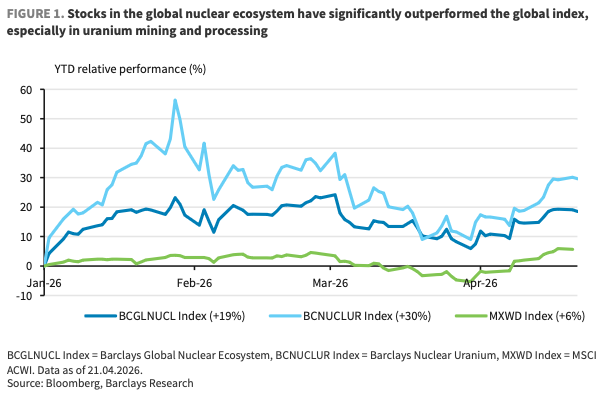

Given the run up in their broad global nuclear ecosystem index (BCGLNUCL +19%) this year, there is undoubtedly a continued interest in the nuclear theme. This also correlates with “a broad rotation from capital-light to capital-heavy (HALO) sectors”.

The market seems to be distinguishing between the themes within the nuclear renaissance, with companies in the nuclear fuel chain (BCNUCLUR +30%) providing higher returns YTD than the broader nuclear ecosystem…

The bar is being set higher by investors lately, though, with money being “less willing to fund nuclear on narrative alone, instead increasingly rewarding delivery of existing megawatts, visible permitting progress or at least a credible bridge from concept to contracted project”.

As we detailed long before most others started realizing it, Barclays also notes how the Iran war has accentuated national energy security concerns. It has not gone unnoticed how countries like France have had little to care about with the dramatic energy market price swings, while countries like Germany and other Asian nations have suffered.

The Iran war has also led to a plus for nuclear energy adoption in Europe based on the broader concept of the strategic autonomy agenda at the EU.

As it should be well understood by our readers at this point, the underwriting of nuclear development by hyperscalers has given significant confidence to the adoption of nuclear energy in the US. Massive energy deals from Meta, Microsoft, Google, and Amazon have all highlighted the significant role to be played by a power source that's actually clean and reliable.

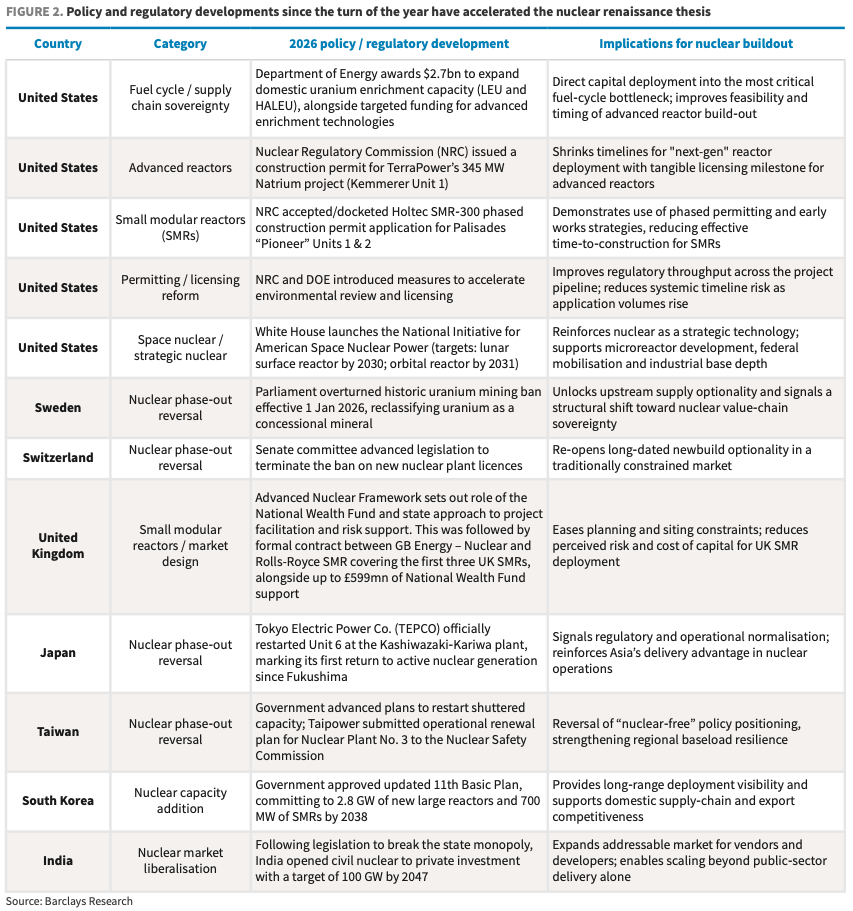

While Barclays notes there are plenty of bottlenecks that remain throughout the nuclear industry, “progress has become more visible in areas that matter most for build out”. Issues are being worked on in concrete ways throughout the fuel cycle, licensing, and component supply areas.

The report emphasizes that the clearest evidence of progress is in the fuel cycle. Progress is turning into production at US uranium mines and major projects are progressing through development in Canada.

Other award programs from the U.S Department of Energy are also boosting the front end of the fuel chain, specifically the $2.7 billion for enrichment capacity.

Significant progress has also been made on the regulation front with improvements to new licensing pathways and high speed programs for iteration and demonstration of new reactor technology.

With site-specific planning ongoing, along with early component ordering, “the industry is beginning to bridge the gap between design ambition and concrete delivery”.

Calling back to their previous point of the labor bottleneck, this challenge is starting to work its way to be the leading issue. Unlike a lot of the supply chain issues, which are mostly solved with more money, “workforce constraints remain deeply structural and are likely to take longer to ease”.

And then there is the issue of where the US gets 300,000 engineers to build all this missing power supply by 2030 https://t.co/a18crhqZ4v pic.twitter.com/tinW8SHDwM

— zerohedge (@zerohedge) October 14, 2025

At Barclay's recent NextGen Energy Conference in New York, the participants reportedly highlighted labor as a critical and growing execution constraint on both the data center construction and power generation construction areas. Data centers and reactor plants will find themselves competing for the same limited pool of electricians, engineers, and experienced construction labor.

This leads to Barclays making the closing statement that “labour is now emerging as perhaps the most important residual hurdle to the pace of the nuclear renaissance, with progress in this area likely to play a key role in determining whether improving policy support and hyperscaler demand can translate into build-out at scale”.

.jpg?branch=production&format=jpg&width=1024)

.jpg?branch=production&format=jpg&width=1024)

.png?branch=production&format=jpg&width=1024)

{kind=link}

{kind=link}

{kind=link}